As individuals reach retirement, they face a complex set of interrelated financial decisions. In addition to deciding how best to draw upon Social Security and pension benefits, they must decide:

- How to allocate personal savings to various asset classes,

- How much to invest, if at all, in an immediate or deferred annuity, and

- How much income to withdraw from savings each year.

Last year, PIMCO’s client analytics team published research that introduced an optimization model to help retirees answer these questions simultaneously. For full details of the model and assumptions, please see the April 2015 Quantitative Research article, “Investing in Retirement.” We believe the article’s insights can help providers of retirement solutions create products that will help individuals achieve retirement security.

Specifically, the paper points to two significant conclusions:

- Retirees should employ longevity protection strategies, such as a deferred annuity, designed to minimize the risk of outliving their savings. Regardless of how long a retiree actually lives, a longevity “safety net” makes it feasible to increase spending earlier in retirement and to take on more investment risk in hopes of achieving greater returns.

- Portfolio returns should influence how much a retiree withdraws to spend. All else equal, a retiree can afford to spend somewhat more when investment returns are strong, but should reduce spending when returns are weaker.

The Value of Longevity Protection

It has been well documented1that immediate annuities are generally shunned by investors because they tend to be comparatively expensive, lack liquidity and prevent retirees from passing on the investment as an inheritance. However, other types of annuities, such as deferred annuities, where payments start at some predetermined point in the future, have greater appeal. In general, they may be an effective tool to manage longevity tail risk. As M. Barton Waring and Laurence B. Siegel2 put it: “Running out of money before running out of life is a catastrophe!” An annuity provides a hedge against this risk.

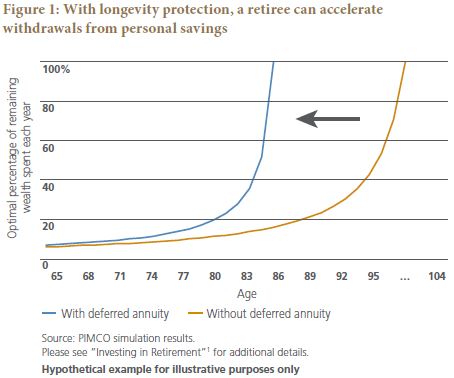

While a variety of longevity products are available, our analysis is limited to two: simple immediate and deferred annuities. Among these options, our model suggests that retirees allocate a significant portion of their savings (10% to 20%) to a deferred annuity. As Figure 1 shows, without longevity protection, a retiree must substantially delay spending to minimize the risk of running out of savings. This results in lower overall real consumption, particularly several years into retirement. With an annuity in place, however, the optimal strategy is to spend the bulk of personal savings by the time annuity payments start.

How Much to Withdraw?

The model assumes that Social Security benefits cover only 40% of pre-retirement income (the national average), so any additional consumption must be funded through a combination of annuities and invested savings. While an immediate annuity can provide a predictable income stream, our model instead recommends allocating to an investment portfolio combined with longevity protection that kicks in during old age. Retirees adopting this plan must satisfy their spending needs by withdrawing income from their investment portfolio until longevity payments begin.

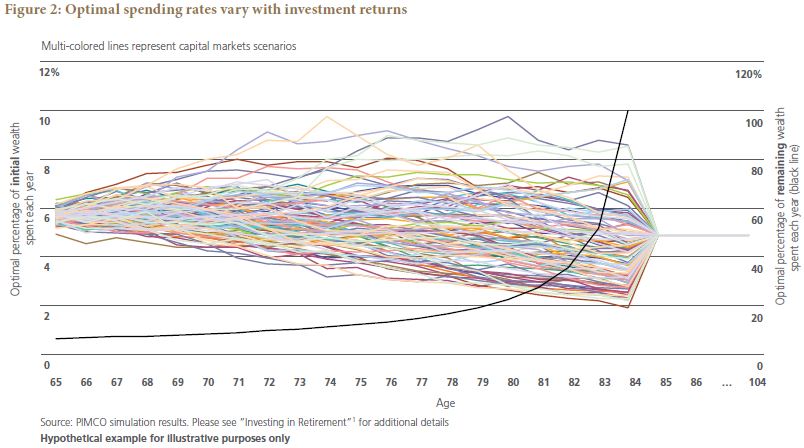

A common rule of thumb is that retirees should spend 4% of their initial wealth each year during retirement.3 However, in our model, the optimal spending rate in each year is a predetermined percentage of the remaining wealth at that time, as illustrated by the curves plotted in Figure 1. Of course, as retirement unfolds, an individual’s remaining wealth will depend on the performance of the investment portfolio: When investments perform well, the retiree can spend more; when investments perform poorly, the retiree must spend less.

As a percentage of initial wealth, then, the optimal spending rate is more complex than the 4% rule of thumb. Rather, this spending rate should adapt over time in response to the investment portfolio’s performance. Figure 2 shows the optimal spending schedule across various capital markets scenarios for a sample retiree.

Finding The Right Fit?

Looking for broad recommendations on how to invest in retirement is like looking for a shoe size that will fit everyone. Every individual’s situation is different, and solutions that focus on the “typical” retiree are unlikely to fit many individuals. For example, retirees looking for more income consistency may consider allocating a greater portion of their assets to annuity products that provide guaranteed lifetime income.

Nonetheless, we find that for a wide range of situations, the optimal solution combines financial market investments with longevity protection strategies that are designed to provide income in old age. Because markets provide not only upside potential but also downside risk, retirees must adapt their spending consistent with investment performance. Longevity protetion strategies can play an important role in budgeting and reducing the catastrophic risk of running out of money before running out of life.

1 Siegel, Laurence B. (2015): “After 70 Years of Fruitful Research, Why Is There Still a Retirement Crisis?” Financial Analysts Journal, Vol. 71, No. 1, 6-15. http://www.cfapubs.org/doi/pdf/10.2469/faj.v71.n1.1

2 Waring, Barton M. and Siegel, Laurence B. (2015): “The Only Spending Rule Article You Will Ever Need,” Financial Analysts Journal, Vol. 71, No. 1, 91-107. http://www.cfapubs.org/doi/pdf/10.2469/faj.v71.n1.2

3 Bengen, William P. (1994): “Determining Withdrawal Rates Using Historical Data,” Journal of Financial Planning, Vol. 7, No. 4 (October), 171-180. http://www.retailinvestor.org/pdf/Bengen1.pdf