Market Outlook

Investors cautious after rocky 2015, but recession appears remote

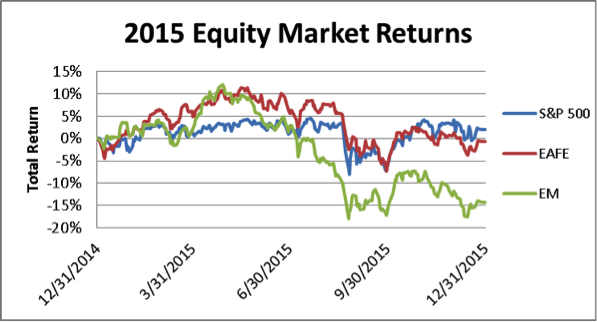

Investors stomached a white-knuckle ride through much of 2015 as the financial markets searched for direction. Although global equity indices bounced off their September lows during the fourth quarter, returns for the full year proved disappointing. The S&P 500 Index reported a total return of 1.4% in 2015, but returns would have been negative without the benefit of dividends. Performance in overseas markets proved even more challenging, as the international developed market index (MSCI EAFE) reported a full-year loss of 0.8% and the emerging market index (MSCI EM) declined 14.9% during 2015.

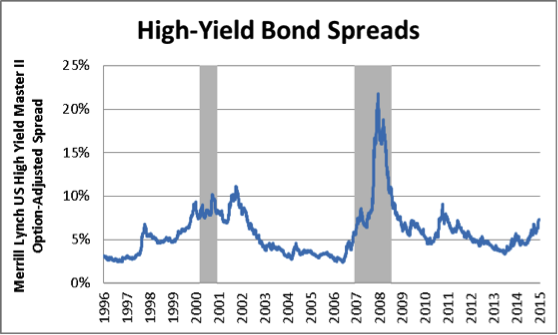

With the bull market approaching its seven-year anniversary, investor sentiment has become increasingly cautious. In the high-yield bond market, investors have begun demanding more return to take on risk. Spreads (the yield difference between junk bonds and comparable U.S. Treasuries) in December widened to their highest levels since 2011, spurring anxiety among some equity market observers, since rising high-yield spreads preceded both the 2000 and 2008 stock market downturns.

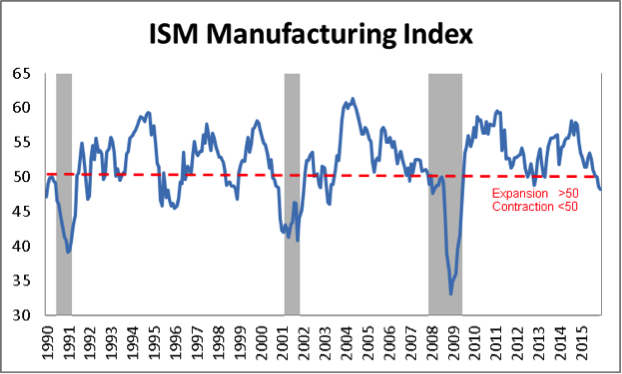

We don’t believe prevailing high-yield bond spreads suggest an imminent bear market for stocks. We do think investor vigilance is merited, however, as equities are not trading at their bargain valuations from a few years ago and the global economic backdrop has been sending mixed signals. While the U.S. economy as a whole continues to exhibit strength with sustained improvement in the labor market and relatively consistent (albeit modest) annualized GDP growth of 2.5%, there are pockets of weakness in domestic activity. For instance, the Institute for Supply Management (ISM) Index, which measures manufacturing activity, moved into contraction territory (below 50) for the first time in three years during November and ended the year at its lowest reading since 2009.

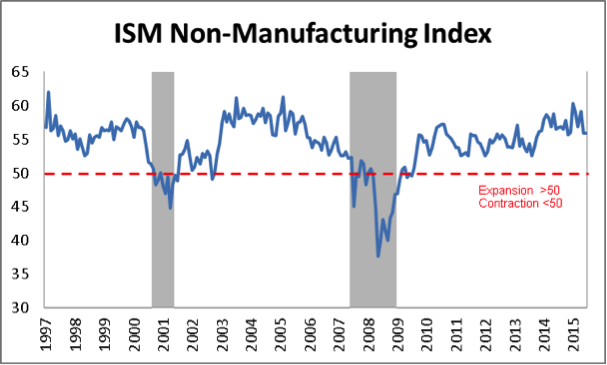

Given that most recessions have followed a manufacturing sector downturn, the ISM Manufacturing Index is a closely observed leading economic indicator. That said, index contraction sometimes occurs in the middle of economic cycles and does not always result in recession. U.S. manufacturing activity is clearly under pressure because of declining activity in energy and natural resources, as well as the strong dollar’s negative effect on exports. It is crucial to note that the manufacturing sector is less important that it has been in past cycles, however, now representing just 12% of the U.S. economy. More importantly, the services side of the economy, which accounts for the majority of U.S. economic activity, remains healthy, as the ISM Non-Manufacturing Index is still expanding solidly.

Though we are not overly concerned about the recent slump in the U.S. manufacturing sector, we believe the underlying factors behind that slowdown, particularly the decline in commodity prices, warrant close monitoring. The collapse in commodity prices has negatively affected corporate profits, capital spending, emerging markets and, most recently, the credit markets. Thus, the trajectory of commodity prices from here will likely be a critical influence on equity market returns in 2016. It is important to recognize that today’s depressed commodity prices are largely a function of oversupply, not a lack of demand. Global oil consumption, for example, increased by an estimated 1.4 million barrels per day in 2015 and is expected to increase by another 1.4 million barrels per day in 2016, according to International Energy Agency (IEA) forecasts. With the price of oil (and many other commodities) below the marginal cost of production, we expect a dramatic deceleration in the growth of global commodity production during 2016. This slowdown will ultimately bring supply and demand back into balance and should boost commodity prices to more rational levels over the coming quarters. In aggregate, we believe a return to commodity price equilibrium will benefit the global economy and the financial markets in 2016.

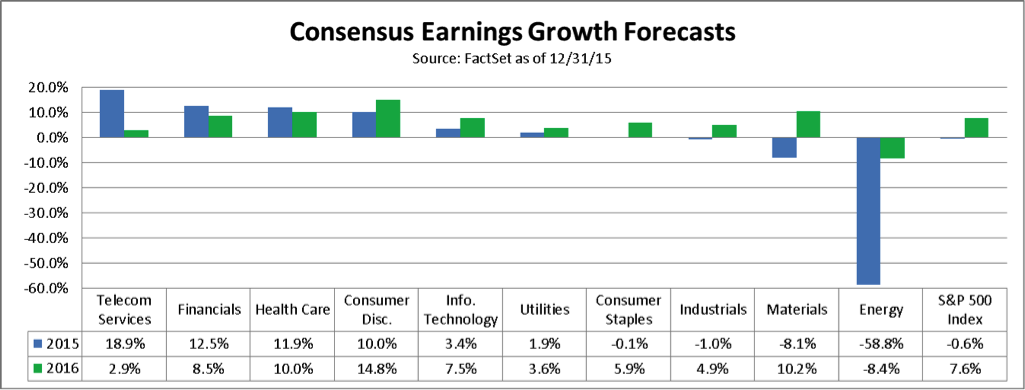

Domestic corporate earnings growth was relatively stagnant in 2015, primarily because of profit erosion in the energy sector (-58%) and a significant drag from the strengthening U.S. dollar. Absent a global or domestic recession (both of which we view as unlikely), we believe U.S. corporate earnings in 2016 will return to the long-term trend of mid- to high-single-digit growth.

The S&P 500 ended 2015 at a P/E of 17.3 times, which is slightly higher than the historical average trailing P/E of 16.4 times. We think a slight valuation premium is warranted in a low interest-rate environment, but we do not believe P/E multiples will expand from current levels. Thus, just as we predicted in 2015, we expect equity returns in 2016 to track corporate earnings growth closely.

Like 2015, we would not be surprised to see increased bouts of market volatility in 2016. An aging business cycle, tighter (though still accommodative) Fed monetary policy, variability in the commodity markets, and escalating geopolitical risks could all contribute to heightened investor anxiety in the coming year. That said, we still believe solid fundamentals are in place for the market to overcome these concerns. While acknowledging that we are now firmly in the second half of this economic cycle, the unusually slow recovery following such a deep recession means this expansion could continue well beyond the typical recovery period of approximately 5 years. That potential, together with a likely rebound in corporate profit growth, creates a strong opportunity for stocks to outperform other asset classes in 2016 and beyond.

Investment Overview

Core Portfolio

We initiated a new position in Brookfield Asset Management (BAM) during the fourth quarter.

Brookfield Asset Management is an alternative asset manager focused on “real asset” investments. The company owns and operates publicly listed partnerships and private equity funds that invest in real estate, renewable energy and infrastructure. The company’s global investment and operating platform provides strategic flexibility to invest across numerous asset classes and geographies, including certain markets not accessible by other large investors. Brookfield generates cash flow from both the fees it charges for managing its funds and from the funds’ investment performance. The assets purchased by BAM’s funds are the backbone of the global economy, and they should continue to grow in value as the global economy expands. Despite some inevitable downturns, most of those assets should also be able to endure (and sometimes even advance) during periods of global economic disruption and consolidation. We believe Brookfield’s expertise in managing real asset investments offers a compelling way to capitalize on numerous secular trends: an increasing reallocation of capital into real assets, protection from potential (or inevitable) inflation as a result of loose global monetary policy, sustained growth in emerging market economies, and substantial demand and need for infrastructure investments.

During the quarter, we exited our holding in Kroger (KR).

Kroger is one of the world’s largest food retailers, with an expansive footprint in the United States. While many of the company’s grocery store peers have struggled in recent years, Kroger reported exceptional earnings growth over the last five years because of its management’s superior execution of its Customer First strategy. Although the company continues to report solid results with industry-leading same-store sales growth, this has been fully incorporated into Kroger’s current valuation. Shares are trading at a historic peak multiple, both on an absolute level and relative to its peer group. With what we view as limited upside opportunity from this valuation, coupled with the downside risk from unremitting competitive threats and potential deflationary pressures, we decided to exit our position in Kroger and reallocate the proceeds into more attractive investment opportunities.

Equity Income

MLPs poised for comeback in 2016

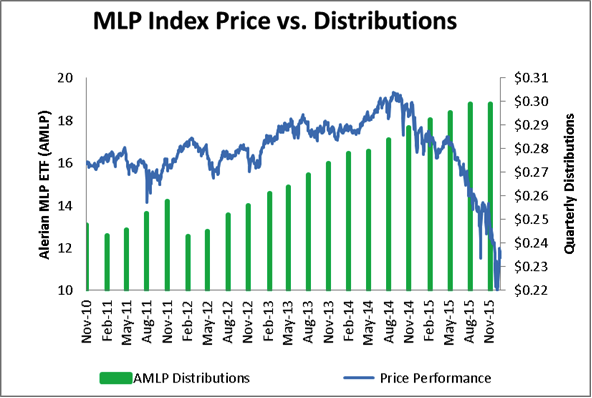

Income-producing equities, such as Master Limited Partnerships (MLPs), Business Development Companies (BDCs) and Mortgage Real Estate Investment Trusts (mREITs) reported mixed results during the fourth quarter, but each category finished down for the full year. As was the case during the third quarter, MLPs declined in value the most among these asset classes during fourth quarter—further extending their substantial full-year loss.

The prospect of rising interest rates and falling energy prices continued to weigh on MLPs, but escalating fears of widespread distribution cuts have proved particularly damaging to the sector’s performance recently. Although MLP distribution growth in 2016 may prove less robust than initially forecasted, we still believe most of the sector will sustain (or increase) distributions for the year, since industry fundamentals remain relatively healthy. While the outlook for MLPs is not without risks, we believe attractive valuations, solid long-term fundamentals and abating headwinds from 2015 tax-loss harvesting will attract investors back to the sector in the first half of 2016 and boost beaten-up MLP stock prices.

Fixed Income

Yields rise as Fed raises short-term interest rates

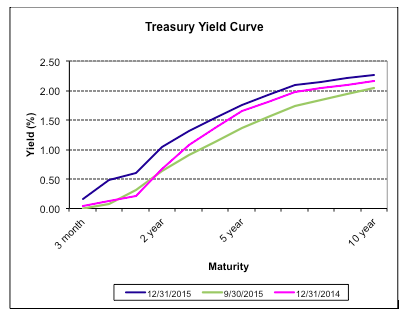

The yield curve shifted higher in the fourth quarter as the Federal Reserve raised short-term interest rates. The yield on the 10-Year US Treasury increased about 10 basis points from the end of 2014.

Municipal bonds remain relatively attractive compared with taxable bonds, as their generally improving credit quality and limited new issuance provide a favorable backdrop for the sector.

Alternatives

Hedge fund performance lackluster, but new opportunities loom

Hedge Funds posted slight losses in 2015, though dispersion between strategies and managers was much greater than it has been in many years. Market-neutral trading strategies and managers who were short commodities posted better results than fundamental managers with more market exposure. While an uptick in market volatility helped trading strategies, 2015 still turned out to be a difficult year. Widening credit spreads; growth outperforming value, since most hedge funds have a value orientation; and the market’s punishment of companies that didn’t meet expectations all contributed to lackluster performance. Last year’s volatility has resulted in some compelling valuations, however, and should create investment opportunities going forward.

A strong lending environment continues to support Real Estate prices, though much discussion remains around how potentially rising interest rates may affect real estate prices. A gradual rate increase could have a nominal effect on real estate prices, since landlords can raise rents accordingly. If the economy slows, however, real estate prices may stagnate, even if the pace of rate hikes remains slow. As a result, while discussions have centered on rate moves, economic growth may have more of an effect on real estate prices than interest rates.

Private Equity appears to be in the early stages of a transition. After many years of steadily rising prices for venture capital-backed companies, a number of later-stage growth companies have been forced to raise capital at lower valuations than previous fundraising rounds. As a result, investors are becoming more discerning in deploying capital. Additionally, investors are repositioning portfolios into areas such as distressed strategies and smaller buyouts. Since private equity typically does best after volatility in the public equity markets, 2016 could be the beginning of a very rewarding period for the strategy.