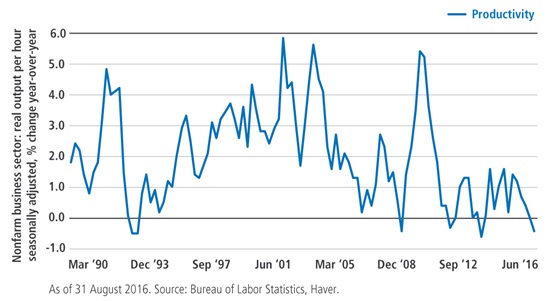

Fundamentals pointed to more of the same underwhelming growth picture. In keeping with the trend in recent months, risk sentiment remained robust despite a tepid fundamental backdrop that was largely unchanged. Economic indicators in the U.S. continued to paint a muddled outlook with impressive labor market gains, robust personal spending and confidence figures offset by a slight downward revision to Q2 GDP. In a reversal from July, U.K. sentiment rebounded considerably, while “hard” economic data, such as unemployment, retail sales and GDP, also impressed. The Bank of England (BOE) launched its stimulus package as promised, including its first interest rate cut in seven years. As the U.K. economy shrugged off Brexit worries for the time being, Europe’s concerns grew. Sentiment among German businesses took a steep dive, and eurozone PMI fell nearly one point, though at 52.0 it remained in expansionary territory. In stark contrast to last August, when a surprise currency devaluation spurred a dramatic market sell-off, China news was notably light. Despite weakening Chinese industrial production, softening retail sales and slowing credit growth, markets managed to maintain an almost eerie calm.

Markets continued to rally in the absence of left tail economic surprises. Many of the market trends evident in July continued into August as risk assets gained. Healthy risk appetite was apparent and credit spreads ‒ high yield, in particular ‒ tightened on the month. Equities were only modestly higher, but the three major U.S. indexes set all-time records early in the month. Implied volatility, as measured by the VIX Index, remained well below long-term averages; August’s daily average was the lowest in the past two years. Even U.S. 10-year Treasury yields remained remarkably range-bound, though the yield curve flattened and the dollar moved higher as Fed Chair Yellen’s Jackson Hole address was perceived to be hawkish. The current economic and financial market configuration is far from the marvel of Willy Wonka’s Chocolate Factory, but it does make one wonder: With unprecedented levels of central bank support around the world unable to stop the global economy from becoming increasingly fragile, the U.S. mired in lackluster growth in the eighth year of an expansion, and yet sovereign yields at all-time lows and equities at all-time highs, is it real, or is it pure imagination?

World Records

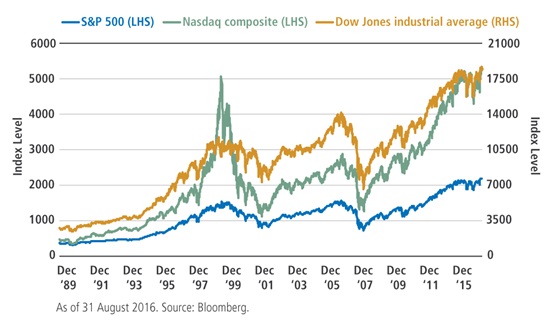

While Usain Bolt and Katie Ledecky were breaking records at the Rio Olympics, the three major U.S. equity indexes (Dow Jones, Nasdaq and S&P 500) simultaneously set all-time highs in mid-August, an alignment that has not happened since 1999. Momentum from July – with a continued building in investor risk appetite – carried the markets to their new highs. Equities have remained buoyant amid low interest rates and a generally resilient economy, marking a sharp turnaround from earlier in the year when recession fears gripped markets. Despite the new records, equity markets closed the month on a more subdued note as Fed Chair Yellen’s address at the Jackson Hole symposium pushed expectations higher for the next Fed rate hike, possibly as early as September.

EQUITIES

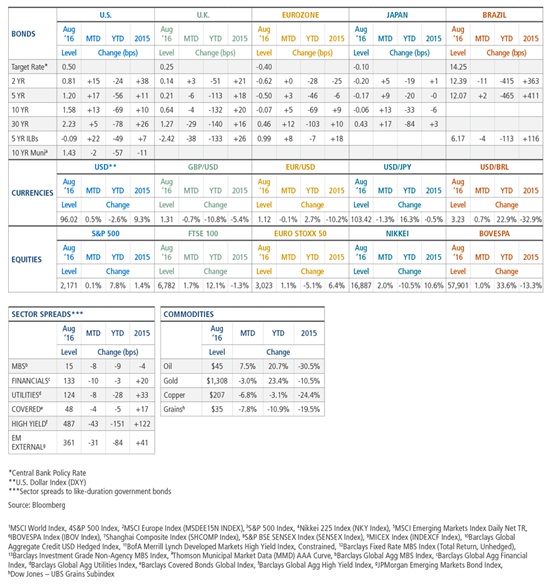

Developed market equities1 returned 0.1% during the month, trading range-bound amid muted volumes as investors awaited central bankers’ next policy moves. In Europe,2 stocks rose 0.7%, while U.S. equities3 ended the month flat, returning 0.1%. Japanese equities4 outperformed most developed markets, returning 2.0% on a slightly weaker yen and dovish rhetoric from the BOJ at Jackson Hole.

In emerging markets,5 equities rose 2.5% as stabilizing macro fundamentals, combined with low to negative yields in developed markets, continued to drive flows into risk assets. Brazilian stocks6 extended their gains, returning 1.0% amid the anticipation and realization of former President Dilma Rousseff’s impeachment, paving the way for fiscal reform. Chinese equities7 advanced 3.7% following the approval of a second trading link from Hong Kong to mainland markets and loosening of foreign investment limits. Indian equities8 also ended the month positive, returning 1.5%, while Russian equities9 advanced 1.4% on a rebound in oil prices.

DEVELOPED MARKET DEBT

Against the benign global backdrop, developed market yields generally drifted higher over the month. Observers closely followed policymakers’ comments at Jackson Hole, and market expectations for at least one U.S. rate hike in 2016 rose to nearly 60% after Janet Yellen communicated that improving economic data strengthened the case for a rate hike as soon as September. Two-year Treasury yields, which are more sensitive to Fed rate hike expectations, rose nearly 20 basis points (bps), and the curve flattened. Japanese yields spiked early in the month on disappointment with the Bank of Japan’s (BOJ’s) stimulus package announced last month, while yields in Europe continued to trend higher in the absence of major left tail economic surprises. U.K. yields proved the exception, as 30-year rates rallied nearly 30 bps after the Bank of England (BOE) cut its base rate by 25 bps and launched a bond-buying program.

INFLATION-LINKED DEBT

Global inflation-linked bond (ILB) markets posted gains for the month,

led by the U.K. after the Bank of England introduced additional easing measures early in the month. In the U.S., real rates on Treasury Inflation Protected Securities (TIPS) followed nominal yields higher on the back of better economic data, including a strong July payrolls report. Following recent flattening, the U.S. breakeven inflation curve steepened despite higher oil prices as headline Consumer Price Index (CPI) came in below expectations. U.K. index-linked gilts saw strong outperformance versus their nominal counterparts in August, with breakevens supported by an upside surprise to the Retail Price Index (RPI), stronger demand from domestic accounts, and a modest decline in the pound. Among European ILBs, peripheral countries outpaced core issuers in a continuation of the post-Brexit recovery, with additional support coming from a modest upside surprise to August’s preliminary Italian Harmonised Index of Consumer Prices (HICP) figures.

CREDIT

Global investment grade credit spreads10 continued to rally in August, tightening another 9 bps alongside continued global monetary policy support and a recovery in commodity prices following a brief sell-off in July. Year-to-date total returns for global investment grade credit stand at 8.3%, as low yields globally continue to be a key driver of demand for credit and should remain favorable for spreads.

Global high yield bond yields11 reached a 16-month low in August amid easing global macro concerns, an improving backdrop for commodities and accommodative central banks. With spreads down about 55 bps for the month (and 160 bps for the year), global high yield bonds have posted their seventh consecutive month of positive returns, up 2.2% in August and 13.2% year-to-date.

EMERGING MARKET DEBT

EM debt posted modestly positive returns in August, as risk assets continued to perform well despite renewed expectations of a Fed rate hike later this year. Spreads over Treasuries for external debt narrowed, EM local yields were flat, and currencies generally strengthened modestly against the U.S. dollar. Developed market yields remained anchored near all-time lows, lending support to EM assets, and stronger energy prices and idiosyncratic political events also drove performance in select markets. In South Africa, a weak showing by the ruling party in local elections drove down yields and strengthened the rand. Elsewhere, Brazilian yields fell and the real appreciated following the formal removal of President Rousseff from office.

MORTGAGE-BACKED SECURITIES

Agency MBS12 outperformed like-duration Treasuries by 32 bps, bringing year-to-date excess returns to +11 bps. Ginnie Mae MBS outperformed conventional MBS, 30-year MBS outperformed 15-year MBS, and higher coupons outperformed lower coupons within 30-year conventional mortgages. July prepayments, reported in early August, declined by 7%, and the average refinancing index for August also declined 9%. Non-agency MBS prices increased and spreads tightened amid continued favorable market technicals and stable residential real estate fundamentals. Non-agency commercial MBS13 (CMBS) was also strong, outperforming like-duration Treasuries by 63 bps. CMBS technicals have been favorable given the slower pace of new issuance year-to-date and continued investor interest in high quality spread assets.

MUNICIPAL BONDS

Municipals were up modestly during the quiet trading month, as they outperformed Treasuries across the curve: Long-dated muni yields were anchored, while the front end drifted slightly higher as the market weighed the possibility of a September rate hike. The trend of strong demand absorbing steady supply continued. Refunding was behind much of the $44 billion in August supply, as issuers – most notably, the State of California – took advantage of low interest rates to refinance outstanding debt. Puerto Rico’s federally led restructuring efforts took a first step forward as President Obama appointed seven members to the island’s new financial oversight board. This bipartisan group will work with the governor to draft a fiscal plan that should form the basis of negotiations with creditors.

CURRENCIES

The dollar strengthened modestly against most developed market currencies in August as the market-implied probability of a rate hike at the next Fed meeting steadily increased. The British pound weakened after the Bank of England delivered a strong easing package alongside a cut in the policy rate, while the Japanese yen declined following the government’s introduction of a new fiscal stimulus package early in the month, fueling speculation over future policy coordination. Among emerging markets, idiosyncratic political issues drove currency strength in South Africa, where the ruling party was roundly defeated in local elections, and in Brazil, where President Rousseff was formally impeached and removed from office.

COMMODITIES

Performance was mixed among commodities sectors, with energy posting gains but agriculture and metals selling off. Crude oil prices were supported in part by generally positive International Energy Agency (IEA) data, including improving balances, as well as favorable technicals (short covering). Headlines on refinery cuts provided additional support to petroleum products, which generally outperformed the already notable gains in crude. Natural gas was down as production recovered more than many had expected. Agriculture was also negative as wheat, corn and soybeans all sank meaningfully following a bearish USDA report on new crop yields that surpassed all expectations. Precious metals were down, owing largely to technicals in the absence of any noteworthy shifts in fundamentals. Base metal prices also came under pressure due, in part, to a rise in London Metal Exchange (LME) inventories and news that Chinese local governments were evaluating options to cool rising home prices.