SUMMARY

- Weaning markets off easy monetary policy will be a delicate exercise for the ECB, and we think the bank is unlikely to remove its stimulus until inflation is solidly on track to 2%. We thus view tapering as a topic for 2017 and beyond.

- In the worst case, the ECB could wind up in monetary policy limbo: unable to exit because it wishes to keep government bond yields sustainable, but unable to go on for risk of overstepping its mandate.

- In thinking about asset allocation decisions, we must weigh both the unintended consequences of ultra-loose policy and the political dimension of high unemployment – especially if both conditions persist.

The European Central Bank’s enormous stimulus has strengthened eurozone financial markets’ resiliency, but it has also made them dependent on ongoing stimulus to maintain stability. Weaning markets off easy monetary policy will be a delicate exercise for the ECB and is a topic we think will gain prominence next year – and one that reinforces our long-term caution about investing in the eurozone.

The ECB effectively saved the euro in 2012 by acting as “lender of last resort” to its financially troubled sovereign shareholders. Fiscal policymakers assisted too, ultimately establishing the European Stability Mechanism (ESM) to support eurozone countries in financial difficulty and laying the foundations of a banking union.

The ESM added an important fiscal pillar (alongside the ECB’s monetary one) to the eurozone governance structure, which lacks its own parliament and budget. With little more than €80 billion of paid-in capital, the ESM’s fiscal resources are limited. Yet with the ECB buying vast quantities of its shareholders’ government bonds, ESM resources are needed only in Greece, which has yet to regain market access.

Further near-term easing

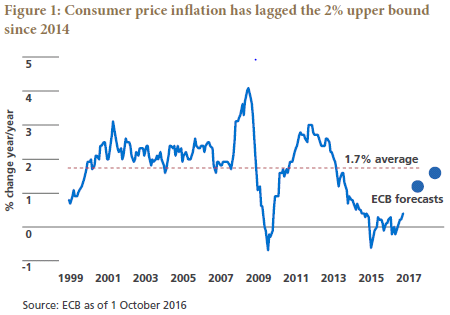

Now that the eurozone crisis has receded, the ECB has refocused on price stability. Since the bank defined price stability in 1998 as the rate of consumer inflation “below, but close to, 2%,” inflation has averaged 1.7% annually, and it has lagged the 2% upper bound since 2014. The ECB projects it to rise from 0.4% currently to 1.2% in 2017 and 1.6% by 2018 (see Figure 1). Five years of low price increases would risk entrenching inflation expectations below target – a key reason we think the ECB will ease again.

So far, the ECB has cut its main refinancing rate to zero and its deposit facility rate to -0.4%, and has committed to purchase €1.7 trillion of bonds through March 2017. This will expand its balance sheet to 17% of gross domestic product (GDP). We expect the Governing Council to announce further easing measures at its 8 December meeting, when it will also publish updated economic forecasts that we believe will show inflation on target by 2019. We think the package of measures will include an extension of quantitative easing (QE) by six to nine months at the existing purchase rate of €80 billion per month, bringing asset purchases to 20%-23% of GDP.

We believe any extension of QE will require the ECB to relax some of its current rules for purchasing government bonds, which mandate:

- Bond yields at or above the deposit facility rate (-0.4%)

- Geographical distribution of purchases in line with the ECB’s capital key

- Purchases not to exceed 33% for any one bond or issuer

Because the capital key rule requires the ECB to buy more German government bonds than those of any other member state, and because nearly two-thirds of all Bunds yield less than -0.4%, an extension of QE will make it challenging for the ECB to find sufficient Bunds to buy. In our baseline, where the ECB extends QE by six to nine months, we estimate it would need to buy between €80 billion-€130 billion in Bunds under current rules. Yet applying the three rules above, there are currently only about €130 billion of Bunds outstanding that the ECB could conceptually buy, and the majority of them have long maturities between 20 to 30 years. Life insurance companies plausibly hold the lion’s share of these bonds and are unwilling sellers; these securities help match their liabilities to policyholders and meet book accounting rules, and alternative assets are in short supply.