Donald Trump took the world by surprise in winning the U.S. presidential election. The long, acrimonious and oftentimes unconventional (to say the least) campaign season concluded with Donald Trump becoming the president-elect. Equally surprising was the Republican Party keeping control of both houses of Congress.

While the Trump triumph and ensuing policy conjecture held the spotlight, a flurry of positive economic releases globally signaled solid fundamentals. U.S. growth continued to improve from earlier in the year as an already strong Q3 GDP growth estimate was revised higher. In addition, retail sales in the UK and Germany were strong.

Risk sentiment built, particularly in the U.S. Most markets appeared to focus on the pro-growth and inflationary potential of possible Trump policies: Equities rallied, yields spiked, inflation expectations rose and the dollar strengthened. However, emerging markets were weaker as the potentially adverse consequences of protectionist trade policy weighed on the sector.

In the world

ROUNDTRIP

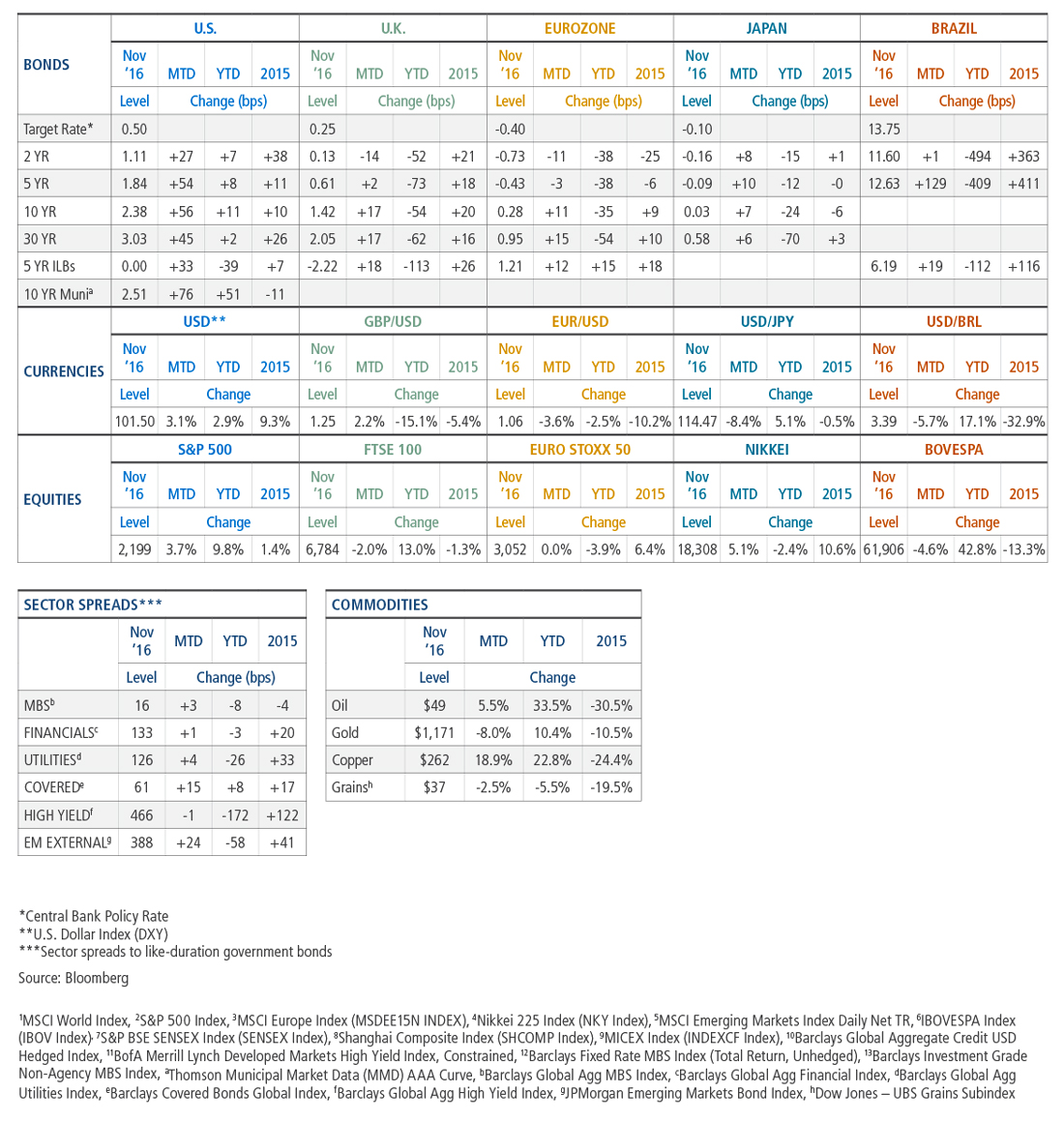

After bottoming in July, U.S. yields spiked following the U.S. election. The move higher partially reflected investors’ expectations for greater fiscal stimulus (in the form of tax cuts and infrastructure spending) and the subsequent impact on both growth and inflation. Concurrent with the rise in yields, the U.S. dollar jumped on the back of strengthening evidence of a Fed hike in mid-December. President-elect Trump’s protectionist campaign rhetoric likely also contributed to the dollar’s appreciation, especially relative to trade-sensitive emerging market currencies. Despite the sizable moves in the month, a longer-term view provides a less dramatic perspective: Yields and the dollar both ended November not far from where they started the year. In fact, the U.S. 10-year yield finished the month within 10 basis points of last year’s ending level.

After bottoming in July, U.S. yields spiked following the U.S. election. The move higher partially reflected investors’ expectations for greater fiscal stimulus (in the form of tax cuts and infrastructure spending) and the subsequent impact on both growth and inflation. Concurrent with the rise in yields, the U.S. dollar jumped on the back of strengthening evidence of a Fed hike in mid-December. President-elect Trump’s protectionist campaign rhetoric likely also contributed to the dollar’s appreciation, especially relative to trade-sensitive emerging market currencies. Despite the sizable moves in the month, a longer-term view provides a less dramatic perspective: Yields and the dollar both ended November not far from where they started the year. In fact, the U.S. 10-year yield finished the month within 10 basis points of last year’s ending level.

Donald Trump took the world by surprise on election day, defying polls, pundits and much of the political press to secure the U.S. presidency. The long, acrimonious, and oftentimes unconventional (to say the least) campaign season concluded with the president-elect’s populist message resonating across large swaths of the populace, especially in key swing states that ultimately determined the winner. Almost equally surprising was the breaking of the political stalemate as Republicans kept control of both houses of Congress. Overnight, U.S. equity futures responded to the political bombshell with a sharp 5% drop. However, expectations for a firmly expansionary fiscal shift towards pro-growth policies spurred an impressive rebound in most risk assets by the following day; developed market equities rallied, yields spiked, inflation expectations rose and the dollar strengthened. These markets appeared focused on policy proposals that have the potential to boost growth and inflation – including tax cuts, infrastructure spending and deregulation – but emerging markets weakened as the potentially adverse implications of protectionist trade policy weighed on the sector.

While the Trump triumph and ensuing policy conjecture drowned out almost everything else, a flurry of positive economic releases globally highlighted solid fundamentals. An already strong third-quarter U.S. GDP growth estimate was revised higher to 3.2%, bolstered by larger increases in household spending than previously estimated. That, combined with solid housing data and expectations for growth-enhancing and inflationary policies, drove market expectations for a Fed rate hike in December to 100%. The euro area also saw promising signs of growth, with retail sales in the UK rising at their fastest pace in 14 years. Also of note, retail sales in Germany marked their largest gains since June 2011 ahead of the all-important holiday season. On the political front, while the landscape in the U.S. was upended, Europe saw some continuity as German Chancellor Angela Merkel announced her intention to run for re-election. In France, former Prime Minister François Fillon became the leading presidential candidate for the Republicans and seemed likely to face off against Marine Le Pen of the populist National Front.

Risk appetite strengthened on balance. Risk sentiment built, particularly in the U.S., and equity markets surged in the weeks following the surprise election result. Among sectors, the reflation rotation led financials and industrials to outperform while utilities and staples lagged, in a clear departure from prior months. U.S. yields moved swiftly higher and sparked a broad sell-off in rates across most developed markets, severing the recently elevated correlation of equity and bond returns. Underpinning much of the move in yields was the expectation for higher inflation; as a result, breakeven inflation spreads widened, though the jump in oil prices on the last day of the month (on news of an OPEC agreement to cut production) also contributed. As yields rose, the U.S. dollar rallied sharply against nearly all global currencies, reaching heights not seen in over a decade (on a trade-weighted basis). A notable exception to the rally in equities was emerging markets: The protectionist trade rhetoric from the Trump campaign cast a pall over Mexico and other economies heavily reliant on the current global trade regime. Still, with reflation trades and the dollar kicking into high gear and the VIX – the measure of U.S. stock market volatility also known as the “fear” gauge – falling precipitously after the election, many investors appeared content to focus on the positive possibilities of new American leadership, despite the significant uncertainties remaining, from administration appointments to the details, timing and implementation of policies.

In the markets

TAKE IT TO THE BANK

U.S. equity markets rallied in the wake of the U.S. presidential election surprise, and all four major U.S. stock indices set record highs in November. Despite the uncertainty surrounding the incoming Trump administration, investors appeared focused on the president-elect’s promises of expansionary fiscal measures. Meaningful dispersion returned across equity sectors: A steeper yield curve and the prospect of a shift toward deregulation buoyed financials, while the threat of trade barriers weighed on technology companies dependent on global supply chains. More interest-rate-sensitive sectors such as utilities also underperformed in the month. Of note, small-cap stocks performed well on the potential for reduced competition from foreign firms and a more pro-business domestic political environment.

EQUITIES

Developed market equities1 returned 1.4% during the month amid an abrupt rotation into sectors that stand to benefit from reflation (i.e., financials, materials and industrials). U.S. equities2 rose 3.7%, and all major indices touched record highs as investors priced in expectations for pro-growth, anti-regulatory and reflationary policies under President-elect Donald Trump. European markets3 ended the month up 1.1%, and stocks were also subject to the “Trump effect” as gains in cyclical sectors were partially offset by losses in defensive sectors. Japanese equities4 rallied 5.1% on the back of a weaker yen and modestly higher yields, benefitting export-oriented firms and financial companies, respectively.

In emerging markets5, the potential for protectionist trade policies in the U.S. under the Trump administration and a stronger U.S. dollar weighed on returns. Stocks experienced their largest monthly drawdown since January, sliding 4.6%. Brazilian stocks6 fell 4.6% amid a renewed focus on political corruption in the President’s cabinet. Indian equities7 also fell 4.5% as investors feared that Prime Minister Modi’s currency crackdown could prove disruptive to the cash-dependent economy. Chinese equities8, however, gained 4.8%, pushing stocks into bull market territory as government efforts to curb surging property prices may be driving more investment toward the stock market. Finally, Russian equities9 rallied the most among emerging markets, returning 5.8% in reaction to President-elect Trump’s apparent willingness to mend relations with Moscow.

DEVELOPED MARKET DEBT

Developed market yields soared in a post-election reflation trade: Investors priced in greater potential for fiscal expansion and infrastructure spending in the U.S., along with a faster Fed hiking path. The reaction was strongest in the U.S., where the 10-year Treasury yield jumped 56 bps to 2.38%. As rates on the long end of the yield curve climbed higher, the spread of 10-year yields over two-year yields widened 28 bps. Other developed markets followed suit, with the German 10-year yield up 11 bps and the UK 10-year yield higher by 17 bps. In Japan, 10-year rates inched into positive territory during the month, but ultimately ended only 7 bps higher at the new target of about 0% after the BOJ successfully defended its new yield curve targeting policy through open market operations.

INFLATION-LINKED DEBT

Global inflation-linked bond (ILB) markets lost ground in November as rates across the globe moved sharply higher. In the U.S., breakeven inflation rates suddenly jolted higher in the wake of the surprise presidential election result. Ten-year inflation expectations in the U.S. ended the month at their highest level in more than two years as investors perceived President-elect Trump’s proposed policy measures as inflationary. An OPEC-induced rally in crude oil prices at month-end also served as a tailwind for breakeven inflation rates. The election results reverberated through other ILB markets as well; most notably, Mexican inflation expectations skyrocketed as the peso sharply depreciated, and yields spiked as the Bank of Mexico attempted to curtail the impact of the currency decline on inflation.

CREDIT

Yields in global credit markets spiked to levels not seen since the end of March as a Fed rate hike in December appeared to be a near certainty, and global investment grade credit10 returned –2.0% for the month of November. While spreads widened modestly during the month, overall they have tightened about 60 bps from the wide levels in February, due to continued strong investor demand for stable income above that of global government bonds.

As investors contended with the sharpest increase in Treasury yields since the Taper Tantrum in 2013, global high yield bonds11 experienced their first monthly loss since January. Yields rose by close to 30 bps over the month but were far outpaced by the increase in government rates, resulting in spreads that were narrower by about 10 bps.

EMERGING MARKET DEBT

EM debt assets came under considerable pressure in November following the U.S. presidential election. President-elect Trump’s campaign rhetoric raised uncertainty about the future of global trade agreements, and EM economies most reliant on the current global trade construct posted the weakest returns. Even as developed market yields moved higher, index spreads over U.S. Treasuries for EM external debt widened, EM local yields rose and EM currencies weakened considerably against the U.S. dollar. Investors pulled nearly $10 billion from the asset class, with the outflows serving as an additional headwind. Bucking the trend, oil exporters across the EM universe generally outperformed as OPEC reached a long-awaited agreement to cut production, sparking a rally in crude oil prices on the final day of the month.

MORTGAGE-BACKED SECURITIES

Rising rates and extending duration weighed on the Agency MBS sector. Agency MBS12 returned –1.72% for the month and underperformed like-duration Treasuries by 47 bps, bringing year-to-date returns relative to Treasuries to –18 bps. Lower-coupon agency MBS outperformed higher coupons, 15-year MBS underperformed 30-year MBS and Ginnie Mae MBS outperformed conventional MBS. Monthly gross issuance declined 8%, the average refinancing index dropped 15%, and October prepayments (reported in early November) fell 5%. Non-agency MBS prices were mixed given the move in rates, but spreads over Treasuries ended the month tighter; the sector continued to benefit from favorable market technicals and the gradual recovery in housing fundamentals. Non-agency CMBS13 returned –1.83% but outperformed like-duration Treasuries by 87 bps. Real estate prices rose again: The seasonally-adjusted S&P/Case-Shiller 20 City Home Price Index was up 0.4%, and the Moody’s/RCA Commercial Property Price Index was up 0.7% for the month of September (the most recent data).

MUNICIPAL BONDS

Municipals sold off sharply during November, posting their weakest monthly return since 2008. The Bloomberg Barclays Municipal Bond Index fell –3.73%, and intermediate to long maturity municipal rates were generally 70 bps to 80 bps higher over the month. The entire sell-off came after the election, as investors weighed what a Donald Trump presidency and a Republican-controlled legislature may mean for tax policy, healthcare reform and infrastructure spending. Voters also decided more than 160 state and local ballot measures: California voted to extend tax increases on top earners for an additional 12 years; New Jersey pledged to dedicate its gas-tax revenues solely to transportation funding; and Puerto Rico elected a new governor who is viewed as modestly more creditor-friendly.

CURRENCIES

The U.S. dollar surged in November. It gained against nearly all global counterparts as Treasury yields soared following the surprise election of Donald Trump. Among G10 pairs, the Japanese yen was notably weaker – down more than 8% against the U.S. dollar – as the interest rate differential between rates in the U.S. and those in Japan widened. The dollar also strengthened substantially against EM currencies on concerns over more protectionist U.S. trade policy under the new administration. The Mexican peso fell almost 9% versus the dollar for the month. China, frequently in the crosshairs of the president-elect, fixed its currency weaker as capital outflows showed little sign of abating. The British pound was the lone currency to beat the dollar on the month after the U.K. high court indicated parliamentary approval is necessary to trigger the country’s exit from the E.U.

COMMODITIES

Commodities posted positive returns in November, with gains supported by the industrial metals and energy sectors. Industrial metals were the best performing sector thanks to notably supportive Chinese manufacturing data, including the PMI at its strongest level in two years during October. In energy, oil prices faced headwinds for nearly the entire month due to uncertainty surrounding OPEC output and growing U.S. inventories. However, a decision for a coordinated production cut (or at least the appearance of one) following the 30 November OPEC meeting sparked a last-minute price rally on the last day of the month. Natural gas prices were also up, as forecasts toward month-end called for colder weather. Performance in the agriculture sector was negative overall; prices were weak for wheat amid poor exports and for corn given stock build-ups. In precious metals, higher real yields and U.S. dollar strength drove gold returns into negative territory overall for November.

In sight

THE TRUMP TRADE

Many investors seem focused on President-elect Trump’s mix of pro-growth economic policies – tax reform, infrastructure spending and deregulation. Yet, trade and immigration are areas where the president has broad powers to act unilaterally – i.e., without congressional approval. A Trump White House could unilaterally withdraw from many existing trade agreements or impose tariffs on specific industries. These risks, along with the potential for a more hawkish Federal Reserve, explain much of the recent drop in Emerging Market valuations and fund flows.

The reactions of the Federal Reserve to the implications of expansionary fiscal policy, combined with the extent (or lack) of protectionist policy will continue to drive near-term performance of the EM asset class as a whole, but there may be divergence across countries. If the Fed becomes only modestly less accommodative, EM countries with relatively strong external balances and reduced linkages to the U.S. could outperform. If trade policy turns protectionist, smaller, more open economies would likely suffer most, not least because China would suddenly become a primary target of policy, and the spillover would hurt the prospects for smaller countries. Trade protectionism combined with a strongly hawkish Fed response (induced by loose fiscal policy) could be the worst-case scenario, though significant pockets of long-term value within the EM asset class may emerge.

Appendix

© PIMCO