Roots of dissatisfaction

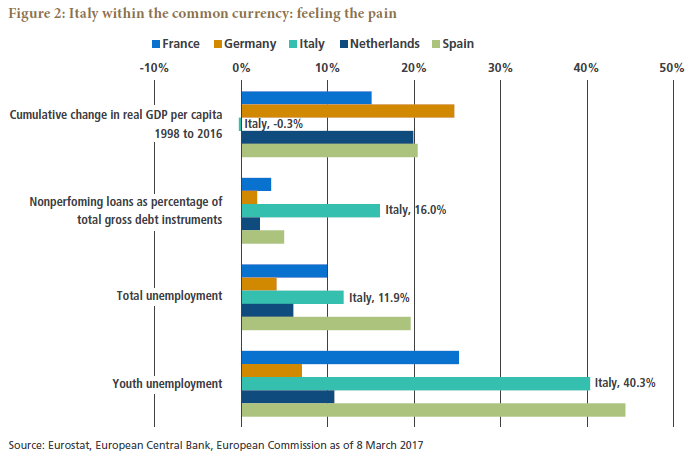

If voters’ dissatisfaction with the euro were solely about economics, Italy would stand out (see Figure 2). Between joining the euro in 1999 and 2016, Italy’s cumulative real economic growth per capita shrank by 0.3%. That is, after adjusting national income for inflation and population change, Italy’s per capita income today is smaller than it was in 1998. Adding to that, unemployment remains elevated at 11.9%, broadly unchanged from 1998, youth unemployment has risen to 40% from 29% in 1998 and bad loans make up 16% of Italian banks’ loan books.

Unsurprisingly, Italy and Cyprus are the only countries in the eurozone where more people think adopting the euro was a mistake for their country than those who think it was a good thing. In the European Commission’s latest Eurobarometer flash survey published in December 2016, 47% of respondents in Italy said having the euro was bad compared to only 41% who thought it was good (12% were undecided or did not know.) Whether Italy’s relatively poor economic performance is caused by its membership in the monetary union itself or by a lack of structural reforms is open to debate. What Italy’s poor economic performance means, however, is that politics will play a large role in determining asset prices in the run-up to the country’s general election scheduled for May 2018.

When we think about how the ECB will navigate its exit from QE, we are not only concerned about the politics in Italy and also in France, where the Front National party advocates a return to the franc. We are also concerned about how political parties in countries that have prospered in the monetary union, such as Germany and the Netherlands, oppose the euro. Central bankers place a high value on independence and inflation targets. They cannot entirely ignore their constituencies, however, and the diverse constituencies in the eurozone are becoming increasingly critical of not only the ECB’s ultra-loose monetary policy but the euro’s governance structure too. This combination poses a challenge for the ECB to exit QE. We think the political sentiment could tilt the ECB toward winding down QE before inflation convincingly reaches 2%, for example, or that it might not be able to offset tighter financial conditions in peripheral countries to the same extent it has in the past.

The case for tapering

The ECB’s monetary policy for the rest of 2017 ought to be straightforward. Rock-bottom interest rates can hardly be cut further, and the central bank has committed to buy assets until at least December this year: €80 billion in March followed by €60 billion per month from April. Based purely on the ECB’s latest inflation forecasts of 1.3% for 2017, 1.5% for 2018 and 1.7% for 2019 (these are year-over-year forecasts for the eurozone’s Harmonised Index of Consumer Prices), logic would appear to suggest the ECB should maintain its current ultra-loose monetary stance well into next year and beyond. After all, even the 2019 forecast is only just consistent with the ECB’s definition of price stability, i.e., inflation rates below, but close to, 2% over the medium term, and core inflation remains sluggish.

Monetary policy does not exist in a vacuum, however; it co-exists alongside fiscal and structural policies and it needs to consider financial stability. Monetary policy contributed substantially to Europe’s recovery from the financial crisis and even more so of late than fiscal and structural policies, which have waned. Yet the efficacy of monetary policy is declining, and the risks to financial stability from a misallocation of resources are rising the longer monetary policy continues in its current form. And despite subpar core inflation, growth in output is closing in on the eurozone economy’s potential.

An uncertain base

In our baseline outlook, no political party currently advocating a euro exit will be able to form a government in the elections to be held this year in France, Germany and the Netherlands. Even if such a party did win, supermajorities in parliamentary votes, or referendums, are typically required to make constitutional changes on matters as important as currency, making the bar for euro exit higher than just winning an election.

With no negative shock to growth or inflation in our baseline forecast for this year, we think the ECB will decide to taper QE further in September this year and wind it down altogether next year. Looking further ahead, we expect the ECB to begin normalizing interest rates toward the end of 2019 and to discontinue reinvesting bonds purchased under QE in 2020 and beyond. But we attach a flat probability distribution to our baseline, and we are very cognizant about the negative tail, for three reasons.

First, a lesson from Brexit and the United States is that voters everywhere are challenging the status quo. While these events abroad strengthened calls to create a mechanism allowing orderly exit from the euro, equally plausible are the election of pro-euro parties that call for invigorating structural reforms and cohesion, scenarios outlined in a White Paper on the future of Europe by the European Commission.

Second, our analysis suggests the rules guiding the ECB’s purchases of sovereign debt leave it with no choice but to taper purchases of government bonds further, beginning early 2018. In fact, we think it will have to cease buying central government bonds in some smaller countries altogether in the first quarter of 2018 if it is to respect the 33% issuer and issue limits. Only by relaxing these constraints and the capital key rule, or by purchasing other assets, could QE be extended beyond the second quarter of 2018, according to our estimates. Assuming the ECB respects the 33% limits and capital key, we think it will taper QE purchases to €40 billion per month in the first quarter of 2018, to €20 billion per month in the second quarter, and then finally end QE in June 2018. Periphery bond markets are vulnerable to the withdrawal of this stimulus, in our opinion, owing to their more challenging debt dynamics.

Third, QE was designed to address the risk of a symmetric deflation shock to the eurozone. Symmetry guides the ECB to purchase public sector assets under QE in line with its capital key, reflecting each member state’s economic weight in the monetary union. For asymmetric shocks affecting individual countries, the ECB intends to use what it calls outright monetary transactions (OMT). Any country applying for OMT must subject itself to a full macroeconomic adjustment programme, or a precautionary programme, under the auspices of the European Stability Mechanism (ESM), before the ECB buys its bonds. And the ECB’s bond purchases in the secondary market will be concentrated on the shorter end of the yield curve. The OMT is therefore completely different from QE.

Further complicating the QE exit

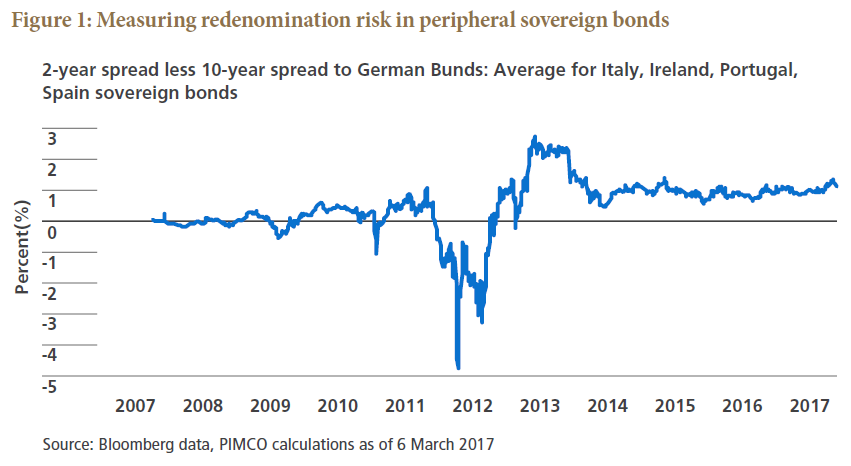

How would the ECB and individual member states react if, in the course of the exiting QE, bond yields continue to rise relative to yields on German Bunds at the same pace they have so far in 2017? We think the response would partly depend on the forces driving yields higher, but we also think QE is no panacea. Symmetry allows for “limited and temporary deviations” from the capital key only, and the 33% limits imposes a natural end to QE early next year. Elected governments value sovereignty and would surrender it only if forced to by, for example, having lost or being on the verge of losing market access. A country whose government is bent on leaving the euro is hardly likely to apply to the ESM for help, yet its actions could have significant spillover risks for others, potentially rendering them in need of ESM help. While Ireland’s, Portugal’s and Cyprus’s macroeconomic adjustment programmes produced substantial returns on government bonds (Greece haircut its government bonds), these programmes undermined the democratic legitimacy of the incumbent governments at the time. This raises a high bar for future applicants to the ESM, which is too small to fully support a country as large as Italy.

The ECB therefore faces a challenging exit from QE that renders peripheral bond markets vulnerable. Our analysis suggests the ECB has limited capacity to respond to a future symmetric shock with QE, or even to an asymmetric shock with OMT, assuming it abides by the 33% issuer limit. The ECB could respond to a symmetric shock by purchasing other assets: bank bonds, equities or interest rate swaps, for example. Such measures would likely affect the prices of these assets; however, they are unlikely to support the real economies and the sovereigns of those countries under stress.

The euro is not facing an existential threat as it did in the summer of 2012. Indeed, we think voters will not elect anti-euro parties to government at this year’s elections. However, their positions and voters’ dissatisfaction with the euro could strengthen in the future, especially if growth remains low, which is why we are concerned about Italy. Unless the ECB accepts increasing exposure to the debt of its sovereign shareholders beyond 33%, which the prohibition on monetary financing anchored in Article 123 of the European Treaty strongly discourages, it will have to phase out QE next year and even then, it would be left with little room to manoeuvre were a country to apply for the OMT. With its balance sheet full and policy rates currently still at the zero lower bound, the ECB’s ability to counteract the next recession when it eventually arrives is limited. At PIMCO, we therefore remain very cautious about our eurozone investments, particularly in the periphery.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.

©2017, PIMCO.

© PIMCO

Read more commentaries by PIMCO