SUMMARY

- Over the next 12 months, continued economic growth, coupled with supply-side normalization and a maturing business cycle, should create room for a continued price recovery for commodities.

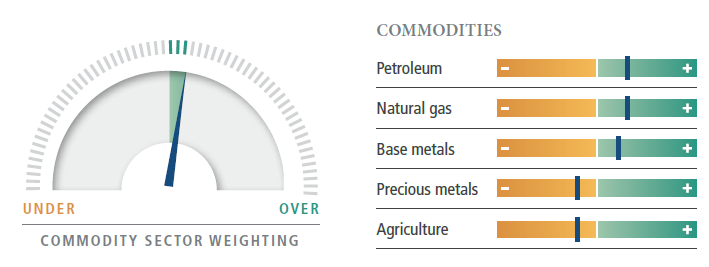

- Among specific sectors, we’re broadly constructive on both oil and natural gas due to strong demand and insufficient investment in supply, and we see scope for improvement in industrial metals prices. We’re more cautious on agriculture.

- Along with broader geopolitical risks that typically affect commodities markets, several policy uncertainties are prevalent today, including OPEC, U.S. tax policy, trade, and central bank activity.

- Commodities could potentially reclaim a diversifying role in portfolios, given growing inflation risks and shrinking correlations between commodities and other assets.

Returns in the commodities markets have improved over the past year amid stronger macroeconomic activity and supply-side tightening, and our outlook for the next 12 months has brightened.

While considerable uncertainties remain for all commodity sectors, we believe the worst market trends may be behind us. As we look ahead to the next 12 months, commodities will likely reclaim a diversifying role in portfolios, given growing inflation risks and shrinking correlations between commodities and other assets.

At this point in the business cycle, we think investors should consider positioning commodities allocations to at least match benchmark targets, if not modestly exceed them.

Supply and demand trends both look more favorable

A quick look at recent history: The “commodity supercycle” of the late 1990s through the 2008 financial crisis – a period when most commodities experienced double-digit annual real price growth – came to an end as investment in supply, partly fueled by low interest rates over the prior decade, led to rapid inventory builds and a correction in prices. The lower prices caused a sharp pullback in capital expenditures, which has translated into slower output growth for some commodities and outright contraction for others. With OPEC curtailing oil output and China restricting capacity in metals, supply-side adjustments have accelerated over the past 12 months. And while we expect capex to begin to grow again, we view this as necessary to meet future demand and not in itself a bearish indicator.

We see reason for optimism on the demand side of the equation as well. Demand growth has been strong for commodities over the past few years despite rather tepid global economic expansion. With support from low prices, oil demand has been materially above trend, and as of December 2016 had witnessed the highest two-year growth period in a decade. And given PIMCO’s cyclical forecast of acceleration in both emerging market and developed market growth as the focus on austerity recedes and infrastructure investment increases, we believe demand will likely remain strong.

These trends provide a favorable backdrop to raw materials demand. Furthermore, commodity market returns tend to be highest during the latter half of the business cycle (where we likely are now), given that prices are driven more by current economic conditions and the near-term supply/demand balance. This is in contrast with equities, which represent a discounted stream of future cash flows and thus provide more of a forward-looking barometer. Continued economic growth, coupled with supply-side normalization and a maturing business cycle, should create room for a continued price recovery.

Sector snapshots

At a high level, we’re broadly constructive on both petroleum and natural gas due to strong demand and insufficient investment in supply, and we see scope for improvement in industrial metals prices due to accelerating GDP and infrastructure growth. We’re more cautious on agriculture given ongoing high inventories and still adequate supply growth, assuming normal weather.

Oil

The oil market outlook is always a bit complicated, in part due to the impact OPEC can have on balances. For all the attention paid to changes in U.S. shale output, OPEC is capable of swinging oil balances more in a single month than U.S. shale can in a year. As a result, any oil outlook must make some material assumptions about OPEC’s intentions at the upcoming May and November meetings.

Rewinding to 2016, the oil market hit an inflection point in the summer as declining non-OPEC output and strong demand signaled a nascent market rebalancing. A fourth-quarter surge in OPEC output looked set to delay rebalancing by yet another year before last-minute negotiations between OPEC and key non-OPEC producers, mainly Russia, led to an agreement to curtail output, accelerating the drawdown of surplus inventories during 2017.

While this deal has reignited non-OPEC investment, we expect OPEC to maintain discipline through year-end 2017, allowing inventories to continue to normalize. The main risk is that OPEC fails to renew the deal and increases output just as the supplies resulting from short-cycle (primarily shale) investment in the U.S. begin to accelerate. Our baseline view is that OPEC will see an incomplete job when it meets in May and extend the deal – and as a result, we expect Brent to average in the mid-$50s in 2017 and 2018. We could revise our price view higher should production costs begin to pick up at a faster rate than producers can improve efficiency.

Natural gas

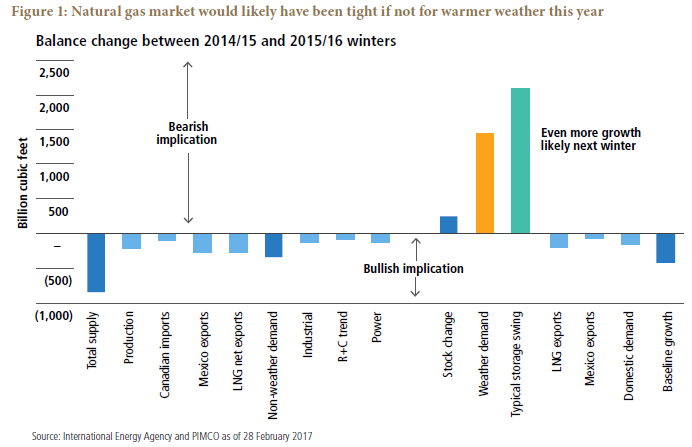

We are constructive on natural gas, particularly relative to the forward curve. As Figure 1 shows, if not for yet another winter of near-record warmth, natural gas prices would likely be much higher: Comparing this past winter to the 2014–2015 winter (the last time weather was close to average seasonal temperatures), declines in supply, expansion in exports and increases in underlying demand are driving improved balances. Remarkably, these shifts were nearly enough to absorb the lack of typical winter weather-related demand.

Looking ahead, we see strong demand for U.S. exports, particularly given the ramp-up of five liquefied natural gas (LNG) export trains between 2016 and 2017 and growing domestic demand, with several large-scale petrochemical plants coming online. This would lead to a call on domestic supply growth that producers will be unable to fulfill at current prices. Our top-down and bottom-up production forecasts show that output is unlikely to match pipeline capacity growth and that additional upstream investment will be needed to satisfy growing demand.

Industrial metals

Metals broadly are closely tied to the global growth cycle and specifically to China’s economy. Although growth in GDP and industrial activity in China have slowed from the heady pace of the previous decade, the economy is now much larger, and aggregate demand growth remains supportive from a volume perspective. In PIMCO’s view, China’s public sector credit “bubble” and its private sector capital outflows will likely remain under control this year, and we expect growth to slow to a 6%–6.5% band as policymakers prioritize financial stability over economic stimulus ahead of the 19th National Party Congress this fall. Any trade war with the U.S. will likely be engaged via words (and tweets) rather than action, and we expect the yuan to depreciate gradually against the dollar by some 4%–5%.

This backdrop is still conducive to continued demand growth. In addition, underinvestment globally and the rationing of surplus supply capacity – recent aluminum smelter closures being a prime example – have broadly supported prices. With global PMIs (purchasing managers’ indices – key indicators of economic activity) accelerating to the highest level in a decade and infrastructure spending likely to rise, the backdrop for industrial metals has improved considerably.

Precious metals

We are reasonably cautious on precious metals. Given PIMCO’s baseline view for modest global GDP acceleration and U.S. Federal Reserve rate hikes, we see scope for precious metals to trade lower this year. While gold does benefit from higher inflation given its exposure to the levels of real interest rates, which are still low by historical standards, we prefer hard commodities that have seen advancements in supply-side adjustment and stand to benefit from improving economic activity for hedging inflation risk.

Agriculture

Among the commodities sectors, we are least optimistic about agriculture. Large crops in recent years have led to a substantial inventory overhang, and inventories will likely remain high given that total acres planted have been slow to drop. It’s worth noting, however, that while we believe agriculture commodities will remain depressed, farmers in North America are just beginning to plant the new year’s crop, and its size and quality could influence our outlook.

Agriculture has the shortest pricing and inventory cycles of the commodities markets due to a supply cycle that resets every year. This means that while supply can respond annually to higher prices, just one bad crop can wipe out even large inventory overhangs. Our outlook could change materially as we enter the summer months – the key yield determination period – if poor weather hurts yields. While the outlook for the agriculture sector is benign in aggregate assuming trend yields, we see room for portfolio optimization. For example, we view the shift in acres planted toward soybeans and away from corn, given recent prices, will support corn going forward at the expense of the oilseed complex.

Investment and portfolio allocation outlook

We believe commodities allocations could play several key roles in investors’ portfolios over the coming year:

Diversification

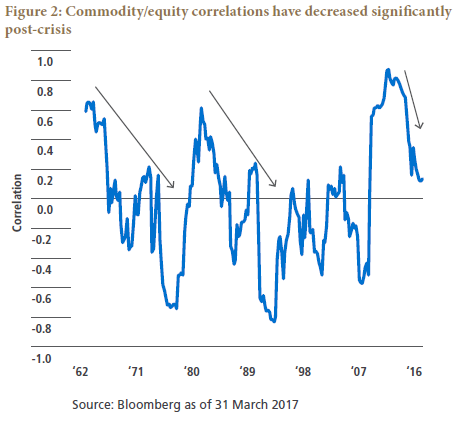

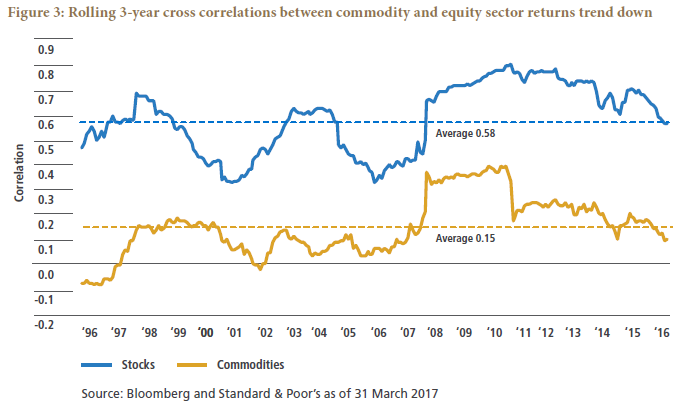

The correlation of commodities returns to other asset classes, such as equities and the U.S. dollar, as well as correlation within the commodity space, has returned to the historical norms we saw before the commodities supercycle and global financial crisis (see Figures 2 and 3).

This is an important point to factor into portfolio construction. During the financial crisis, the high correlation of commodities to equities and other asset classes was disappointing and frustrating to many investors. While commodities as a group will always retain a beta link to global GDP, the recent reductions in correlation and increasing dispersion within the commodity space are evidence that the idiosyncrasies of each commodity will likely differentiate its returns going forward. This shift points to the role commodities can play as a portfolio diversifier – and with central bank liquidity receding, we expect such diversification to become even more important.

Inflation hedging

As inflation concerns have mounted over the past few months, we have seen a corresponding rise in investor interest in commodities. Historically, commodities have demonstrated a positive beta to inflation and, more importantly from a portfolio construction standpoint, a positive beta to inflation surprises. With the focus on austerity diminishing, an increased government desire to spend on infrastructure, and improving labor conditions, we see upside risks to inflation in much of the world. This backdrop is favorable for commodities, particularly hard commodities such as base metals and petroleum.

Potential for positive ‘roll yield’

Surplus markets have dominated commodities over most of the past 10 to 15 years, resulting in low or negative roll yields on futures contracts that have hurt commodity index returns. While the roll yield implied by the 12-month forward curves in the Bloomberg Commodity Index remains negative at roughly −2%, we note that this has improved significantly from −6% a year ago. And should OPEC meet its stated goal of returning oil inventories to historical averages, it’s quite possible that the roll yield for the most impactful commodity in indices will turn positive. We even can envisage natural gas backwardation (when active futures trade at higher prices than futures contracts for the months ahead), as has occurred at times over the past year, if and when the weather supports increased demand.

In our view, active producer hedging in the longer-date futures for both natural gas and oil are depressing forward prices below the values we’d expect. While this prevents higher prices today, it generally serves to steepen the forward curve and improve roll yield. We note that what we’re anticipating is not anomalous, but rather a normalization of the commodity curves to trade much like they did before the supercycle; shale primarily gives some certainty and definition to the long-dated supply and hence the long-dated part of the forward curve. In this environment, much like the early 2000s, commodities markets tend toward backwardation when demand is strong or supplies shrink, and trade in contango (with futures prices exceeding the expected future spot price) when the opposite is true.

Discussions of roll yield often include statements to the effect that commodity equities are a superior way to get commodity-related exposure. However, our research shows that after accounting for the equity beta in commodity equities, they have not outperformed commodity futures historically. (To learn more, see “Commodity Investing: A New Take on Equities Versus Futures.”)

Policy risks complicate the commodity outlook

“Stable But Not Secure” has been a secular theme informing PIMCO’s investment process for nearly a year now, with a focus on uncertainties. Beyond the “normal” geopolitical risks typically present in these markets (and which tend to be supportive for commodity prices), we see a few key policy-related risks today:

OPEC policy

We view OPEC policy as the biggest area of risk to the oil markets. We don’t dispute that U.S. shale supply and shifts in shale inflation will have a material impact on where the long-term futures curve is anchored, and on balances 12 to 24 months forward. However, OPEC production decisions can rapidly swing balances in the short term. While debate swirls around whether the U.S. will grow by 600,000 barrels per day (b/d) or 1 million b/d in all of 2017 (and whether this is repeatable in 2018), OPEC could move output by 1 million b/d by June if it decided to do so.

U.S. tax policy

The potential imposition of a border adjustment tax (BAT) in the U.S. could have significant implications for commodities (although we assign a low probability to its passage given the lack of political support). The most direct impact on commodities of the BAT – which would tax imports and offer tax credits for exports as part of an overall tax policy overhaul – would be to increase the price of U.S. deliverable and traded commodities compared with the same commodities abroad by roughly the magnitude of the marginal tax rate (20%).

While this could benefit key components of the commodities indices, such as WTI crude, RBOB (gasoline), diesel fuel and Henry Hub natural gas, we think overall it would lower the price of non-U.S.-based commodities, such as Brent crude, through a few primary mechanisms: 1) a stronger U.S. dollar that will depress global production costs, 2) a test of OPEC’s ability and willingness to coordinate production when its market share is being ceded to U.S. producers, who see higher prices and improved return on investment, and 3) slower growth in emerging markets, which is particularly relevant to commodities given their size and commodity-intensive growth.

Trade conflicts

While statements from the new U.S. administration have at times been contradictory, policymakers have generally expressed a fairly negative view toward global trade. Changes to the latest G-20 communiqué highlight just how far trade has moved up the agenda in Washington. Given the global nature of tradable commodities and the importance of petroleum in global transport, growing trade frictions would be disruptive to both regional markets and final product demand.

A hawkish mistake by central banks

One macro concern is that major banks overly tighten credit (typically via increased policy rates), thereby limiting or reversing some of the recent economic momentum. While on the surface the impact would probably be short-term bearish for commodities through the demand channel, over the longer term rising rates could paradoxically sow seeds for improved balances by increasing the cost of capital and reducing investment.

Key takeaways

Overall we see a broadly positive outlook for commodities in the next year. Supply-side adjustments, a reasonably positive outlook for global economic activity and firm commodity demand all point to improving fundamentals. With inflation risk rising and the return of commodities as a diversifier for portfolios, we think portfolio allocations that are in line with benchmark allocations or modestly overweight may make sense for most investors.

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. Derivatives and commodity-linked derivatives may involve certain costs and risks, such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Commodity-linked derivative instruments may involve additional costs and risks such as changes in commodity index volatility or factors affecting a particular industry or commodity, such as drought, floods, weather, livestock disease, embargoes, tariffs and international economic, political and regulatory developments. Investing in derivatives could lose more than the amount invested.

There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.

©2017, PIMCO.

© PIMCO

Read more commentaries by PIMCO