(Inf)election Point

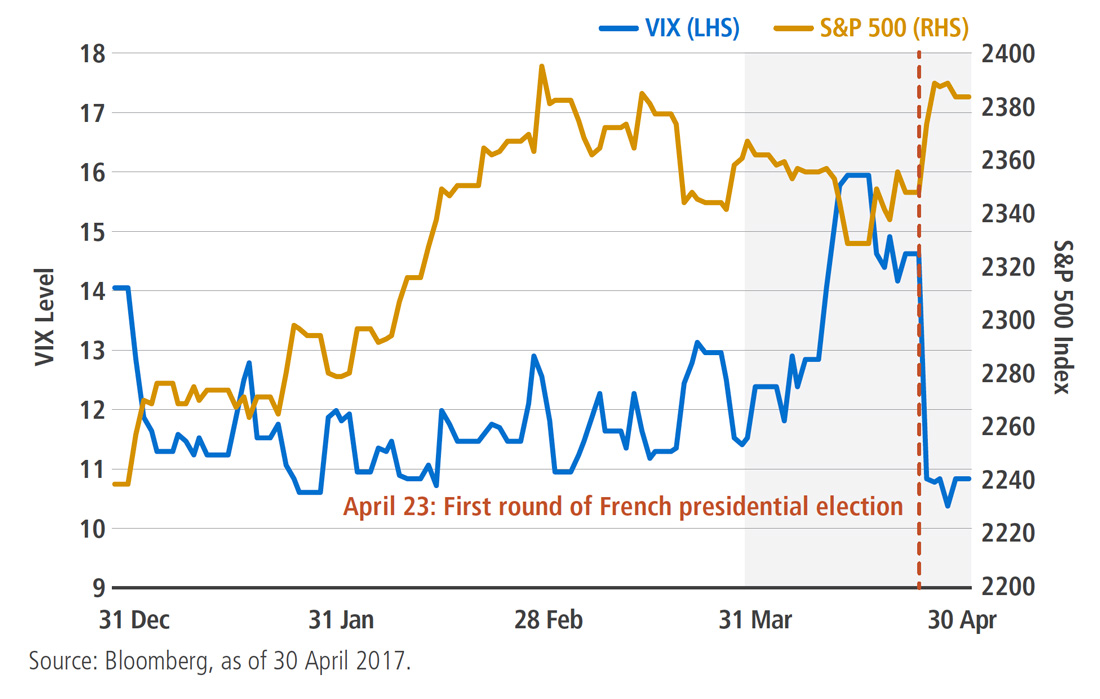

The first round results of France’s presidential election sparked a global relief rally after centrist candidate Emmanuel Macron came in first, ahead of far-right leader Marine Le Pen. Even U.S. markets felt the impact of the election results. Prior to the vote, investors were cautious, and market jitters (represented by the VIX) reached the highest level of the year. But concerns quickly dissipated in the aftermath: The VIX fell to almost 10-year lows and equities rallied on the expectation that pro-Europe Macron would win in the final round. Polls accurately predicted the outcome, a vote of confidence for political opinion polling after last year’s poor predictions in both the Brexit referendum and the U.S. presidential election.

EQUITIES

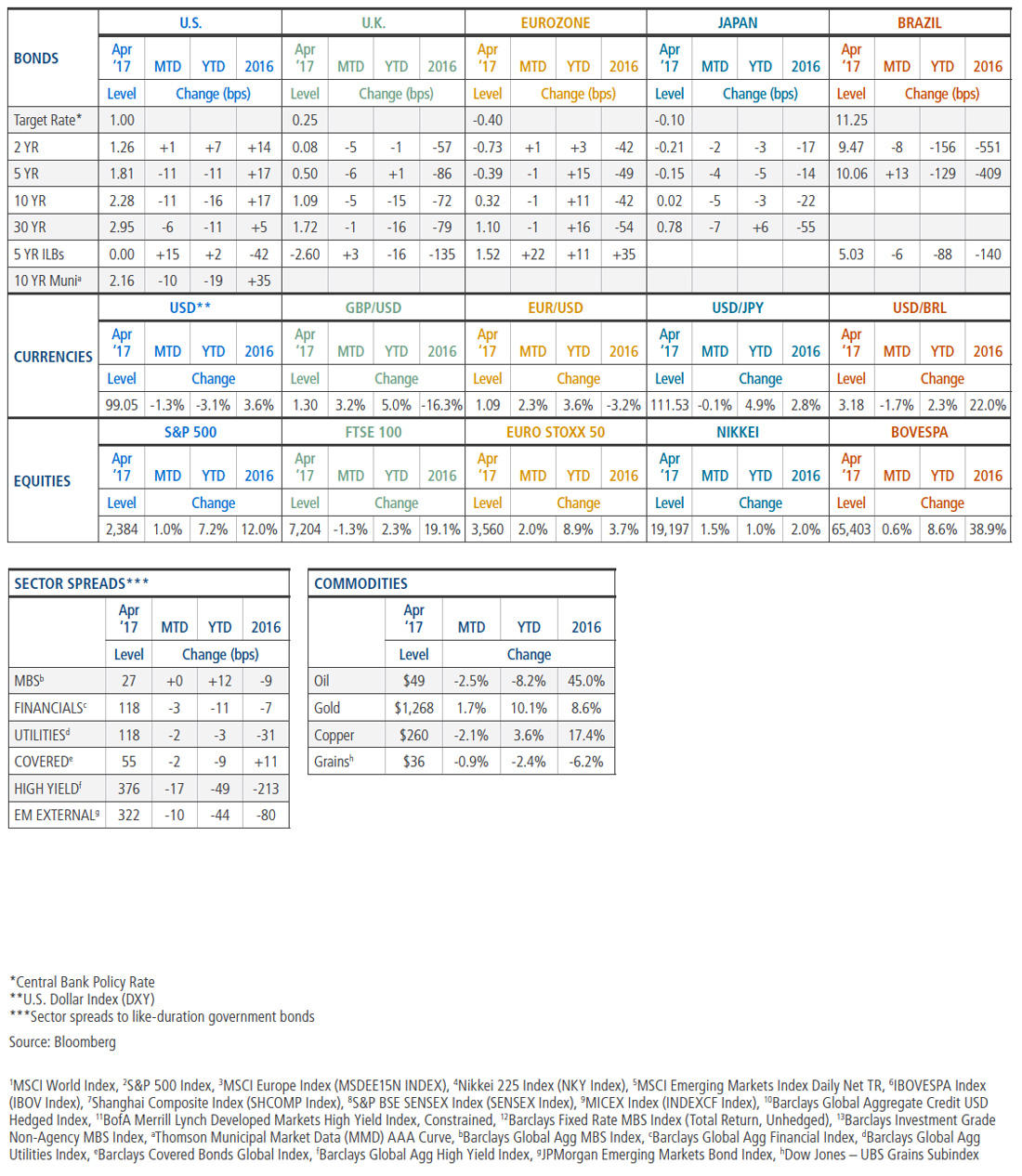

Developed market stocks1 returned 1.5% during the month as investors welcomed news that centrist candidate Emmanuel Macron garnered first place and 24% of the vote in the first round of the French presidential election. U.S. equities2 ended the month higher, returning 1.0% amid better-than-expected first-quarter corporate earnings. Stocks in Europe3 returned 1.7%, with nearly all gains realized after the French election. Japanese equities4 rose 1.5%, sending the Asia-Pacific region into positive territory for the year.

In emerging markets5, stocks benefitted from relatively stable global market conditions and a strong technical backdrop to return 2.2%. Brazilian stocks6 rose 0.6% despite weakness in commodity markets. In China7, stocks fell –2.1% as regulators are expected to ramp up efforts to reduce leverage and fraud in the financial system. Indian equities8 rose 1.0%, touching record highs, while Russian stocks9ended the month up 1.1%.

DEVELOPED MARKET DEBT

Most developed market yields fell in April as investors sought to reduce risk amid the French election, softer U.S. growth data and rising international tensions. The U.S. 10-year Treasury yield fell below 2.20% for the first time since November in the run-up to the French election. As centrist Emmanuel Macron edged out far-right candidate Marine Le Pen for the top spot, Treasury yields retraced a portion of their move but still ended the month 11 basis points (bps) lower. German 10-year bund yields experienced a similar phenomenon, falling 17 bps to a low of 0.16% before recovering to end the month flat, while French spreads against bunds compressed to levels not seen since January.

INFLATION-LINKED DEBT

Global inflation-linked bonds broadly gained, outpacing their nominal counterparts. In the U.S., breakeven inflation (BEI) rates dipped sharply to begin the month as employment and CPI reports both came in notably weak. They came under further pressure from slumping oil prices before rebounding slightly into month-end in response to stronger risk appetite after the French election and increased demand due to index rebalancing. The U.K. breakeven inflation curve steepened over the month: Short-term inflation expectations moved lower on weaker-than-expected retail price inflation and a stronger pound, while long-dated inflation-linked bonds continued to see strong pension demand given light issuance. European ILBs broadly outpaced nominal government bonds, with inflation expectations moving higher in line with inflation readings.

CREDIT

Global investment grade credit10 returned +0.9% in April, and spreads tightened 2 bps. Credit markets reacted strongly to the results of the first round of the French presidential election, reversing what had been until then a lackluster month for returns. Investor demand for stable income remained strong during the month, highlighted by continued strong investment flows into high-grade retail funds and ETFs.

Global high yield bond11 yields declined through the month, approaching the multi-year low set in early March – a positive response to the French election outcome, as well as to strong corporate earnings and optimism related to President Donald Trump’s tax plan proposal. With yields 26 bps lower at 5.1%, spreads tightened 15 bps to end April at 372 bps.

EMERGING MARKET DEBT

Stable external conditions focused investors’ attention on improving fundamentals, and emerging market debt posted another month of positive returns in April. Spreads on external debt tightened and index yields on local currency debt fell as investment flows into the asset class continued apace. EM currencies continued to appreciate against the U.S. dollar, showing resilience to volatility in crude oil prices, which rallied during the first half of the month before retreating in the latter half. The Turkish lira rallied following the passage of a referendum that allows President Erdogan to consolidate power and thus reduces political uncertainty, and frees up the central bank to pursue monetary tightening. In Asia, the South Korean won depreciated amid heightened concern over a potential conflict with North Korea.

MORTGAGE-BACKED SECURITIES

Agency MBS12 returned 0.65% and outperformed like-duration Treasuries by 2 bps. The March Federal Reserve meeting minutes were released and revealed that the Fed expects to begin reducing its balance sheet in late 2017 but plans to reduce exposure to both MBS and U.S. Treasuries, which was modestly bullish for MBS performance. Overall, conventional MBS outperformed Ginnie Mae MBS, 30-year MBS marginally outperformed 15-year MBS, and higher coupon conventional MBS outperformed lower coupon conventional MBS. Both gross issuance and Fed reinvestments were in line with March levels, while prepayment speeds increased 23%. Non-agency MBS prices rose moderately, although spreads relative to swap rates were unchanged. Non-agency commercial MBS13 returned 0.83% and outperformed like-duration Treasuries by 3 bps.

MUNICIPAL BONDS

Below-average new issue supply and positive flows into municipal bond mutual funds supported the market in April, and the Bloomberg Barclays Municipal Bond Index returned 0.73%. Intermediate munis outperformed as the yield curve flattened. The White House unveiled a tax reform plan that lacked details, which was a relief to muni investors: It became clearer that the likelihood of sweeping policy changes remains low, and any changes will probably take longer than previously expected. At the end of the month, creditors rejected Puerto Rico’s first official debt restructuring offer, moving the island closer to filing bankruptcy.

CURRENCIES

Politics was in the driver’s seat for most currency markets in April. The euro rose against the U.S. dollar and was the top performer in the G10 on the French presidential election result. Solid European inflation data provided an additional boost to the euro at month-end. Thanks to the appreciation in the euro and President Trump’s continued denunciation of dollar strength, the greenback weakened on the month. U.K. Prime Minister Theresa May surprised markets by announcing a snap election in June, which strengthened the British pound; the early election is expected to provide her some leverage in the upcoming Brexit negotiations. EM currencies continued to outperform – notably, the Turkish lira, which gained as the central bank demonstrated a renewed commitment to orthodox monetary policy and lifted the liquidity lending rate by 0.5%.

COMMODITIES

Commodities dipped lower over the month of April, with losses broad-based across major sectors. Within energy, oil prices rallied to begin the month before losing ground on uncertainty around future OPEC production. In contrast, natural gas posted incremental gains thanks to supportive weather forecasts and a dip in inventory. Within agriculture, returns were mixed, with coffee and sugar prices plunging; notably, live cattle outperformed due to stronger demand for beef. Base metals were broadly lower, and gold prices gained as the U.S. dollar weakened.

Outlook

PIMCO expects the nearly eight-year-old global economic expansion will strengthen and broaden over the coming year, driving global GDP growth to 2.75%–3.25% from 2.6% in 2016 and boosting CPI inflation to 2.25%–2.75%. Our outlook reflects several positive factors: generally supportive fiscal policies (or expectations of them) in most developed market economies, easier financial conditions since the start of the year, more positive animal spirits as indicated by consumer and business confidence data, and a rebound in global trade.

In the U.S., we see growth above-trend at 2%‒2.5% in 2017 as business investment recovers, particularly in the energy sector, and consumer spending is supported by a further decline in unemployment, higher consumer confidence and expectations of personal income tax cuts in 2018. We forecast core inflation to hover sideways this year at 2.0%–2.5%, but expect that the Fed will feel encouraged by above-trend growth to raise interest rates two more times during 2017.

For the eurozone, we now expect growth will rise to a range of 1.5%‒2.0% in 2017, revised higher from our forecast in December to reflect the stronger momentum into this year. While political uncertainty remains elevated ahead of crucial elections in France, Germany and potentially Italy, both fiscal policy and monetary policy are expansionary, and the recovery in global trade growth supports exports and investment. We anticipate core inflation at just below 1%, making little headway toward the European Central Bank’s (ECB) “below but close to 2%” objective. We also expect the ECB to continue buying bonds at a pace of €60 billion per month through December 2017, before tapering and eventually ending its purchases from early next year.

In the U.K., we expect growth to stay in the range of 1.75%–2.25%(above market consensus) despite Brexit, reflecting robust momentum, higher government spending and a positive contribution from net trade on the back of the 15% drop in the pound in 2016. We forecast CPI inflation to exceed the Bank of England’s 2% target but expect that the Bank will keep policy rates unchanged this year.

Japan’s fiscal stimulus and a weaker yen should propel GDP growth to 0.75%‒1.25% in 2017 while inflation remains significantly below the 2% target. The Bank of Japan is likely to keep targeting the overnight rate at –0.1% and the 10-year bond yield at 0% and thus continue its standing invitation to the government to engage in additional fiscal expansion, which we expect to happen later this year.

China’s public sector credit bubble and private sector capital outflows will likely remain under control, and we expect growth to slow to a 6%‒6.5% band in 2017 as policymakers prioritize financial stability over economic stimulus ahead of the 19th National Party Congress in the fourth quarter. Any trade war with the U.S. will likely involve words rather than action, and we expect the yuan to depreciate gradually by 4%–5% against the U.S. dollar.

In emerging markets, we expect moderate growth will return to Brazil and Russia as their deep recessions end. With inflation dropping, both countries’ central banks could cut rates multiple times. Mexico’s Banxico is expected to tighten policy further, following the Fed’s lead, and growth should slow to 1.25%‒1.75% as a result.

In sight

High uncertainty yet low volatility

U.S. stock market volatility has cratered to near decade lows despite a high degree of uncertainty regarding the U.S. policy outlook. How can this be? Earlier this year, two key factors were likely drivers: the rally in equities (rallies are typically accompanied by drops in volatility) and a decline in stock correlations (as some stocks rallied a lot more than others, overall index volatility was curbed).

But the story appears to have changed a bit since the end of February—the rally has been largely on hold, and realized correlations have actually been on the rise. Those two key factors damping volatility through February don’t seem as relevant, and yet the collapse in equity volatility has persisted. The most likely explanation is that investors have taken a wait-and-see approach to changes in fiscal policy. At some point though, meaningful changes to the tax code could materialize, and in the near term, companies will either meet or fall short of relatively lofty earnings expectations. So U.S. stock volatility has collapsed, but there is reason to believe it may rise again – and perhaps by a lot.

Appendix

Past performance is not a guarantee or a reliable indicator of future results. All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk and liquidity risk. The value of most bonds and bond strategies is impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in foreign denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax; a strategy concentrating in a single or limited number of states is subject to greater risk of adverse economic conditions and regulatory changes. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation- Protected Securities (TIPS) are ILBs issued by the U.S. government. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax. Corporate debt securities are subject to the risk of the issuer’s inability to meet principal and interest payments on the obligation and may also be subject to price volatility due to factors such as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Commodities contain heightened risk, including market, political, regulatory and natural conditions, and may not be suitable for all investors. It is not possible to invest directly in an unmanaged index.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. ©2017, PIMCO.

©2017, PIMCO.

© PIMCO

Read more commentaries by PIMCO