In the world

The month of May featured elections in France, Iran and South Korea, but renewed political controversy in the U.S. and Brazil garnered headlines. France kicked off May’s presidential races as Emmanuel Macron secured a larger-than-expected final round victory over Marine Le Pen. Next, South Koreans chose a different path with Democratic Party candidate Moon Jae-in, months after former President Park Geun-hye was impeached and removed from office. Iranians, meanwhile, re-elected President Hassan Rouhani. Still, much of the news cycle focused on the freshly charged political environment in Washington after President Trump dismissed FBI director James Comey, who was leading the investigation into Russia’s involvement in the U.S. election and potential collusion with Trump’s campaign. The growing scandal led to the U.S. Department of Justice appointing former FBI director Robert Mueller as special counsel to oversee the Russia inquiry. But the U.S. was not alone in the scandal spotlight: Brazil was thrown back into political chaos after President Temer was allegedly recorded engaging in a bribery cover-up scheme. The accusations came less than a year after the impeachment of former leader Dilma Rousseff and put Temer’s bold economic reform agenda in doubt. Ringling Brothers may have folded its tents for the last time, but lovers of political circus had much to watch.

A rebound in U.S. economic data strengthened the Fed’s case for a rate hike in June while European growth surprised to the upside. A healthy employment report bolstered the Fed’s comments last month that the weakness seen in the first quarter was likely transitory. The economy added 211,000 jobs in April and the unemployment rate fell to 4.4%, alleviating some fears over the anemic 79,000 increase in jobs in the previous month. Retail sales also rebounded, rising 0.4% and outpacing the prior 0.1% gain, as strength in the labor market and a 2.5% increase in hourly wages supported consumption. Against this backdrop, the Fed’s meeting minutes revealed that another rate hike could be appropriate soon (likely June), and outlined a plan to reduce the balance sheet by slowly and predictably ending reinvestments of maturing securities. Across the Atlantic, data indicated that the eurozone’s recovery may be gaining momentum: The economy grew at an annualized pace of 1.8% in the first quarter. Meanwhile, Moody’s Investors Service downgraded China’s sovereign debt for the first time since 1989, citing rising liabilities and slowing growth.

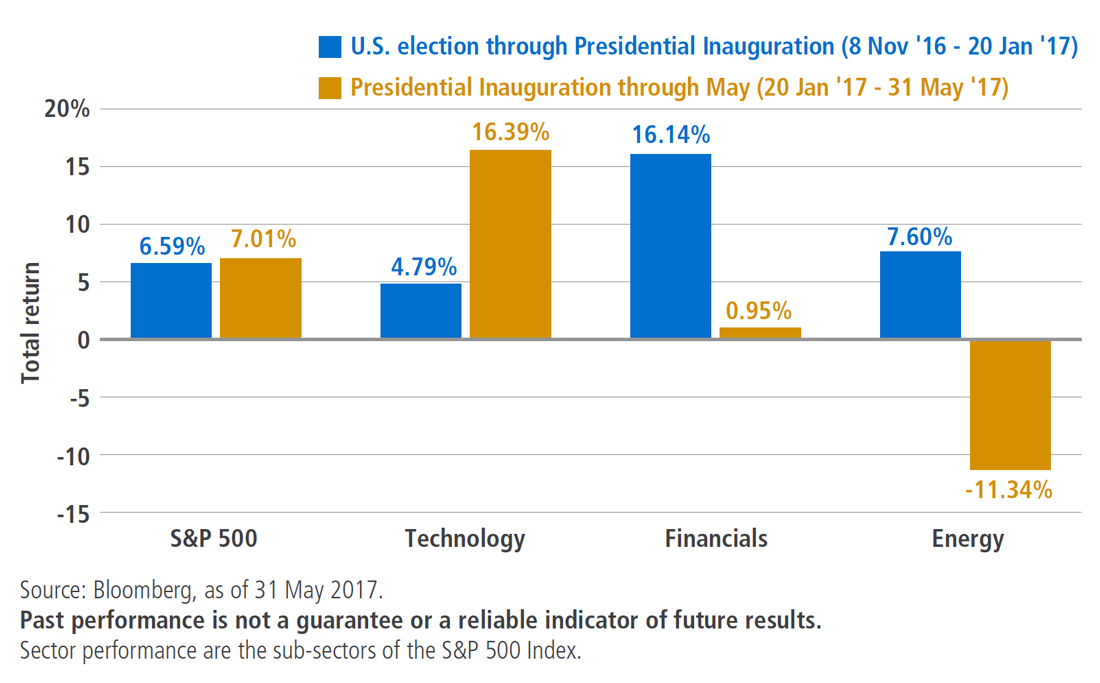

While the political turmoil contributed to a brief period of elevated market volatility, most risk assets recovered to end the month higher. Investor unease over geopolitical events was apparent in May, particularly the controversies surrounding the administrations in the U.S. and Brazil. Still, the seemingly inexorable trend higher in risk markets prevailed as equities globally gained and credit spreads tightened. The VIX – a widely cited volatility measure – also reflected the short-lived nature of the downturn in markets during the month as it reached both its highest intraday level in 2017 and its lowest level since 1993. Also of note, the drivers of the recent equity market gains have changed from those that initially pushed equity markets higher following the U.S. election; while the “reflation trade” immediately following President Trump’s election focused on financial and energy companies, those sectors have struggled more recently. The gains in May – consistent with the emerging trend in 2017 – were driven by technology companies with strong earnings growth, as well as more rate-sensitive sectors like utilities as interest rates have fallen. In fact, the U.S. 10-year Treasury yield is now 24 bps lower than at year-end 2016.

Tech is back

After surging in the weeks following the U.S. election, U.S. equity sectors – such as financials and energy – that stood to benefit from stronger growth, higher inflation and a steeper yield curve (dubbed the “reflation trade”) have faded. Yet, even as optimism waned for rapid progress on deregulation, tax reform and infrastructure spending, the S&P 500 continued to grind higher in May. What drove the gains? A handful of mega-cap technology stocks. Highlighting the lack of breadth in the rally, just six tech stocks have accounted for 35% of S&P 500 gains year-to-date, yet those stocks represent only 12% of the index’s total market capitalization. The rotation into high-growth tech firms has been supported by double-digit earnings growth in Q1 and the sector’s lower sensitivity to falling oil prices, a flattening yield curve and diminishing expectations for sizable and imminent fiscal stimulus.

In the markets

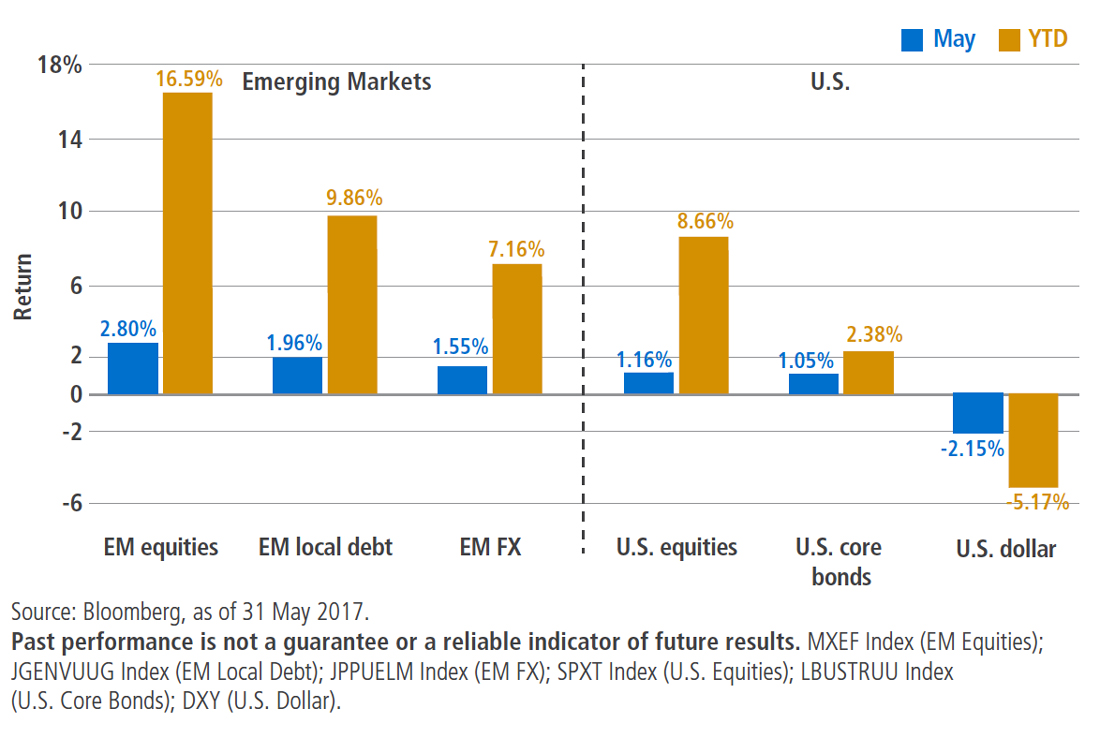

EM streak continuesEmerging market (EM) equities, bonds and currencies delivered strong performance in May, adding to their stellar start to the year. The MSCI EM Equity Index returned 16.6% through the end of May, nearly double the return of the S&P 500 over the same period, while EM local debt and currencies delivered returns in the high single-digits. With developed market (DM) rates trending lower and concerns over protectionism waning, investors have re-focused on improving EM fundamentals, and investment flows have followed. Despite a fresh political scandal in Brazil, investors remain drawn to attractive yields in the sector as inflation abates and countries such as Russia and Brazil emerge from recession.

EQUITIES

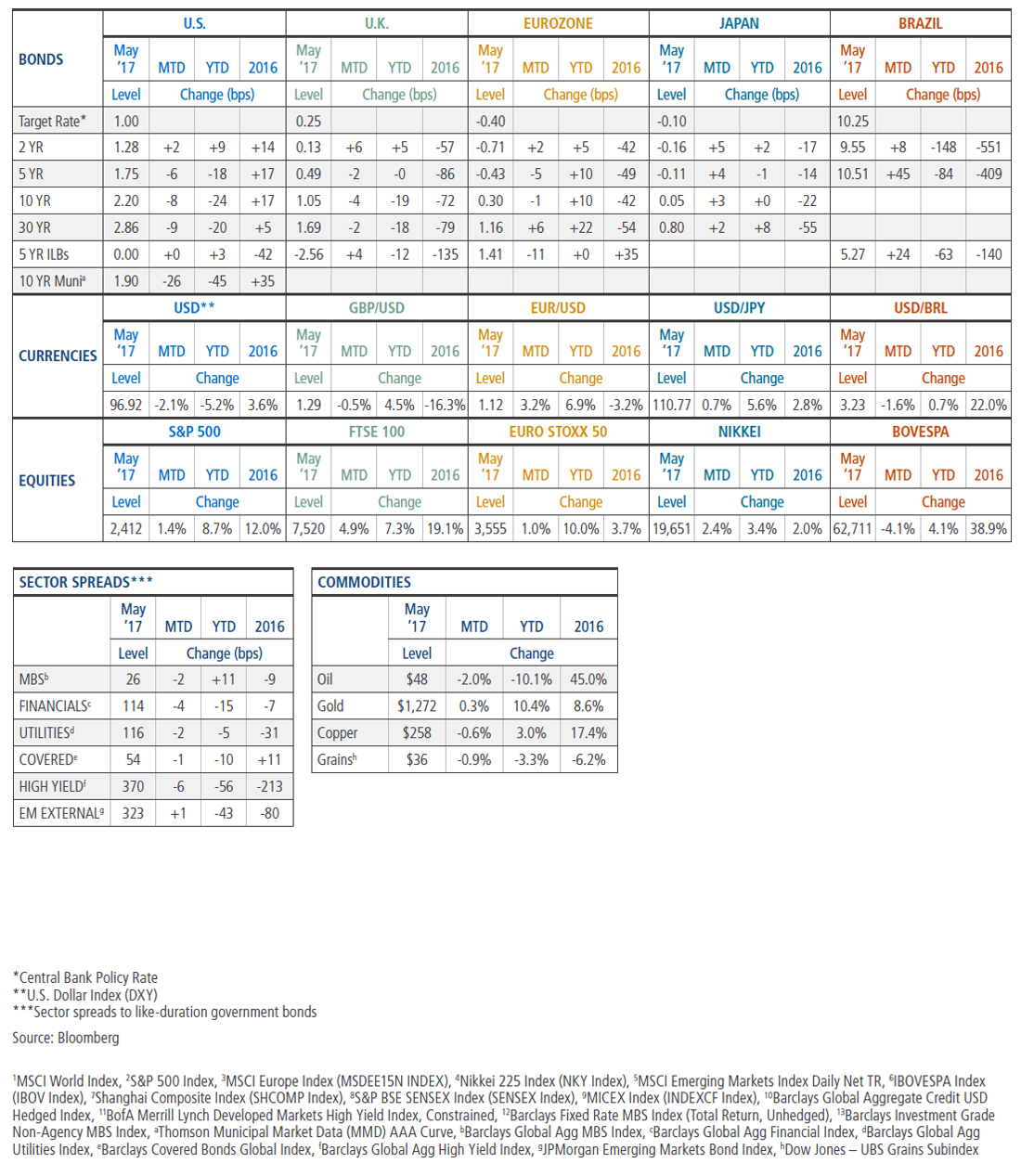

Developed market stocks1 returned 2.1% in May as corporate earnings growth supported optimism and investors shrugged off political controversy in the U.S. After their largest one-day decline in over eight months, U.S. equities2 rebounded sharply to end the month 1.4% higher. Generally positive economic data buoyed stocks in Europe3 to a 1.5% return. Japanese equities4 rose 2.4% after the government reported better-than-expected GDP growth for the first quarter of 2017.

Despite volatility in some emerging economies5, equities benefitted from relatively stable global market conditions and a strong technical backdrop, returning 3.0%. Brazilian stocks6fell 4.1% amid President Michel Temer’s alleged involvement in a corruption scandal, which could threaten future reforms. In China7, stocks fell 1.1% as tight liquidity conditions weighed on returns. Indian equities8 rose 4.1%, touching record highs, while Russian stocks9 ended the month down 5.6% on lower crude oil prices.

DEVELOPED MARKET DEBT

Most developed market rates continued to decline as political uncertainty rose. In the U.S., the front end of the yield curve rose slightly thanks to firm economic data and indications that the Federal Reserve is comfortable with hiking the policy rate soon. Two-year Treasury yields rose two basis points (bps), while longer-term Treasuries continued to rally, with 10-year yields falling 8 bps to 2.20%. Similarly, in the UK and Europe, rates rallied and yield curves flattened but for very different reasons: strained Brexit negotiations, terror attacks and unease over the UK general election on 8 June; recent polls showed UK Prime Minister Theresa May’s Conservative party holding a slimmer majority than expected. Japan proved the exception during the month: Rates rose across the yield curve. The economy expanded at a better-than-expected 2.2% (annualized) in the first quarter, supported by continued strength in exports, healthy domestic demand and an unexpected rise in capital expenditures.

INFLATION-LINKED DEBT

Although global inflation-linked bond (ILB) returns were mixed across countries, they broadly underperformed comparable nominal sovereign bonds in May on generally weaker inflation readings and a dip in crude oil prices. U.S. Treasury Inflation Protected Securities (TIPS) posted outsized underperformance for the month; broad-based weakness in April’s Consumer Price Index (CPI) release and tepid wage growth outweighed a relatively strong 10-year TIPS auction. U.K. index-linked gilts similarly underperformed conventional gilts on inflation news: The Bank of England revised lower its longer-term expectations for inflation, and inflation readings for April indicated moderating prices for services. Within emerging markets, Brazilian inflation expectations skyrocketed and the real plunged in the wake of corruption allegations against President Temer.

CREDIT

Global investment grade credit10 returned +0.9% in May, with corporate spreads tightening 3 bps. Credit markets began the month on a strong note following a market-friendly outcome in the second round of the French elections, although political turmoil in the U.S. and Brazil roiled markets later in May. Investor demand for stable income remained strong overall, highlighted by continued strong flows into high-grade retail funds and ETFs.

Global high yield bond11 prices moved higher during May; the favorable backdrops for rates and stocks as well as a light new-issue calendar outweighed oil price volatility and yields at multi-year lows. Spreads compressed 7 bps over the period and yields dropped 8 bps for a return of 0.9% in May and 4.8% year-to-date.

EMERGING MARKET DEBT

Emerging markets (EM) debt continued its streak of strong performance, posting positive returns in May, thanks to continued global risk appetite and investment flows into the asset class. Modest yield spread widening in external debt was more than offset by a decline in underlying U.S. Treasury yields, while index yields on local currency debt fell and EM currencies continued to rally against the U.S. dollar. Czech, Romanian and Polish local debt were notable outperformers as the Eastern European economies posted stronger-than-anticipated first-quarter GDP growth. Elsewhere, Brazilian debt came under pressure after local media reported the existence of evidence implicating President Temer in bribery and cover-up efforts associated with the “Car Wash” scandal; the news reports spurred speculation that Temer may be removed from office, jeopardizing his proposed fiscal reforms.

MORTGAGE-BACKED SECURITIES

Agency MBS12 returned 0.62% and outperformed like-duration Treasuries by 14 bps. The May Federal Reserve meeting minutes confirmed that the Fed expects to begin balance-sheet tapering later this year, but in a “gradual and predictable” manner, which helped MBS outperform. Overall, conventional MBS outperformed Ginnie Mae MBS, 30-year MBS outperformed 15-year MBS, and higher-coupon conventional MBS outperformed lower-coupon conventional MBS. Net issuance remained robust, and prepayment speeds decreased 7%. Non-agency MBS prices rose moderately, and spreads relative to swap rates tightened. Non-agency commercial MBS13 returned 0.92% and outperformed like-duration Treasuries by 33 bps.

MUNICIPAL BONDS

The municipal market posted positive returns in May, with the Bloomberg Barclays Municipal Bond Index returning 1.59%, and as the muni yield curve flattened, munis outperformed Treasuries across all tenors. Fund flows to the sector remained positive, averaging $450 million per week, while supply grew to $38.2 billion for the month. In early May, Puerto Rico’s federally appointed oversight board filed Title III proceedings, a bankruptcy-like provision under the new law created by Congress specifically for the commonwealth to restructure its debt (PROMESA). The filing followed the expiration of a stay on litigation and a breakdown of negotiations with creditors. In other credit news, Illinois leaders missed a 31 May deadline, steering the state toward its third year without a budget and further downgrades from the rating agencies.

CURRENCIES

Geopolitics largely influenced currency moves in May. Sterling remained volatile as the Conservatives’ lead in the polls seemed to slip somewhat, with some even predicting a hung Parliament. The Brazilian real fell by as much as 9% following allegations of corruption and bribery against the president. However, the currency retraced most of the loss by month-end, and the risks to the broader EM complex were fairly well contained. Most EM currencies appreciated against the U.S. dollar during the month; the Polish zloty, in particular, outperformed on the back of accelerating growth. In Europe, speculation about the pace and path of tightening by the European Central Bank strengthened the euro.

COMMODITIES

Overall, commodities posted negative returns, with only a few positive outliers. In energy, unfavorable weather and climbing U.S. supplies caused a notable sell-off in natural gas. Crude oil prices were down on skepticism that OPEC would succeed in rebalancing market supply due to increasing drilling in the U.S. and rising output from Libya. Gasoline, however, posted gains. In agriculture, sugar and soybeans were large detractors: Sugar came under pressure on the news of Brazil’s political scandal, while slightly higher soybean stocks weighed on an already bearish market. In contrast, corn gained, supported by slightly lower stocks and the expectation of lower year-over-year production. In precious metals, gold posted marginal gains thanks to a weaker dollar and some safe-haven buying. Oversupply concerns, primarily in nickel, dragged industrial metals prices lower.

Outlook

PIMCO expects the nearly eight-year-old global economic expansion will strengthen and broaden over the coming year, driving global GDP growth to 2.75%–3.25% from 2.6% in 2016 and boosting CPI inflation to 2.25%–2.75%. Our outlook reflects several positive factors: generally supportive fiscal policies (or expectations of them) in most developed market economies, easier financial conditions since the start of the year, more positive animal spirits as indicated by consumer and business confidence data, and a rebound in global trade.

In the U.S., we see growth above-trend at 2%‒2.5% in 2017 as business investment recovers, particularly in the energy sector, and consumer spending is supported by a further decline in unemployment, higher consumer confidence and expectations of personal income tax cuts in 2018. We forecast core inflation to hover sideways this year at 2.0%–2.5%, but expect that the Fed will feel encouraged by above-trend growth and continue on its path to policy normalization in 2017.

For the eurozone, we expect growth will be in a range of 1.5%‒2.0% in 2017, revised higher from our forecast in December to reflect the stronger momentum into this year. While political uncertainty remains elevated ahead of elections in Germany and potentially Italy, both fiscal policy and monetary policy are expansionary, and the recovery in global trade growth supports exports and investment. We anticipate core inflation at just below 1%, making little headway toward the European Central Bank’s (ECB) “below but close to 2%” objective. We also expect the ECB to continue buying bonds at a pace of €60 billion per month through December 2017, before tapering and eventually ending its purchases from early next year.

In the U.K., we expect growth to stay in the range of 1.75%–2.25% (above market consensus) despite Brexit, reflecting robust momentum, higher government spending and a positive contribution from net trade on the back of the 15% drop in the pound in 2016. We forecast CPI inflation to exceed the Bank of England’s 2% target but expect that the Bank will keep policy rates unchanged this year.

Japan’s fiscal stimulus and a weaker yen should propel GDP growth to 0.75%‒1.25% in 2017 while inflation remains significantly below the 2% target. The Bank of Japan is likely to keep targeting the overnight rate at –0.1% and the 10-year bond yield at 0% and thus continue its standing invitation to the government to engage in additional fiscal expansion, which we expect to happen later this year.

China’s public sector credit bubble and private sector capital outflows will likely remain under control, and we expect growth to slow to a 6%‒6.5% band in 2017 as policymakers prioritize financial stability over economic stimulus ahead of the 19th National Party Congress in the fourth quarter. Any trade war with the U.S. will likely involve words rather than action, and we expect the yuan to depreciate gradually by 4%–5% against the U.S. dollar.

In emerging markets, we expect moderate growth will return to Brazil and Russia as their deep recessions end. With inflation dropping, both countries’ central banks could cut rates multiple times. Mexico’s Banxico is expected to tighten policy further, following the Fed’s lead, and growth should slow to 1.25%‒1.75% as a result.

In sight

A souring mood(y) on China

China’s downgrade to A1 from Aa3 by Moody’s Investors Service on May 24 was not too surprising since both Moody’s and Standard & Poor’s had warned in March 2016 that they were reviewing China’s ratings. The market impact of the downgrade is also limited: China has not issued sovereign external debt for more than a decade, and local currency bonds are not included in the widely tracked global indexes yet, so there was no index-related selling.

However, the downgrade is far from a non-event: It will likely alert political leadership to the economy’s current trajectory and give reformers at the People’s Bank of China (PBOC), the Ministry of Finance and the financial regulatory agencies ammunition to further rein in debt. Chinese policymakers may now feel a sense of urgency to intensify regulation of the huge shadow banking system, maintain a hawkish monetary policy stance and somehow restore fiscal discipline. Although positive from a structural standpoint, such a policy shift could put more pressure on Chinese growth, financial markets and commodities prices in the coming year.

Appendix

© PIMCO

Read more commentaries by PIMCO