Normalization of the European Central Bank’s (ECB) monetary policy never was a question of “if” but one of sequencing, timing and calibration. Financial markets reacted to ECB President Mario Draghi’s speech in Sintra this past week in a way suggesting the ECB might change all three of those policy normalization parameters. A firmer euro, higher sovereign bond yields and lower stock prices reflect changing expectations for a more forceful, faster withdrawal of stimulus and possibly a reordering of the sequence.

We interpret Draghi’s speech as consistent with the ECB’s evolving changes to forward guidance as it adapts policy to the improving outlook for growth and inflation against the backdrop of the approaching technical limits to its asset purchase programme. We do not interpret Draghi’s speech as a hawkish change in policy.

Many market observers focused on the one sentence in Draghi’s Sintra speech on 27 June 2017 that unsurprisingly suggested the ECB will taper government bond purchases:

“As the economy continues to recover, a constant policy stance will become more accommodative, and the central bank can accompany the recovery by adjusting the parameters of its policy instruments – not in order to tighten the policy stance, but to keep it broadly unchanged.”

Yet they appeared to attach little value to his comments that the “monetary policy stance needs to be persistent”, i.e., the stance will remain accommodative, because “inflation dynamics are not yet durable and self-sustaining”. Or that the ECB will need to act with “prudence” in gradually adjusting its policy parameters, i.e., the normalization process will occur in baby steps.

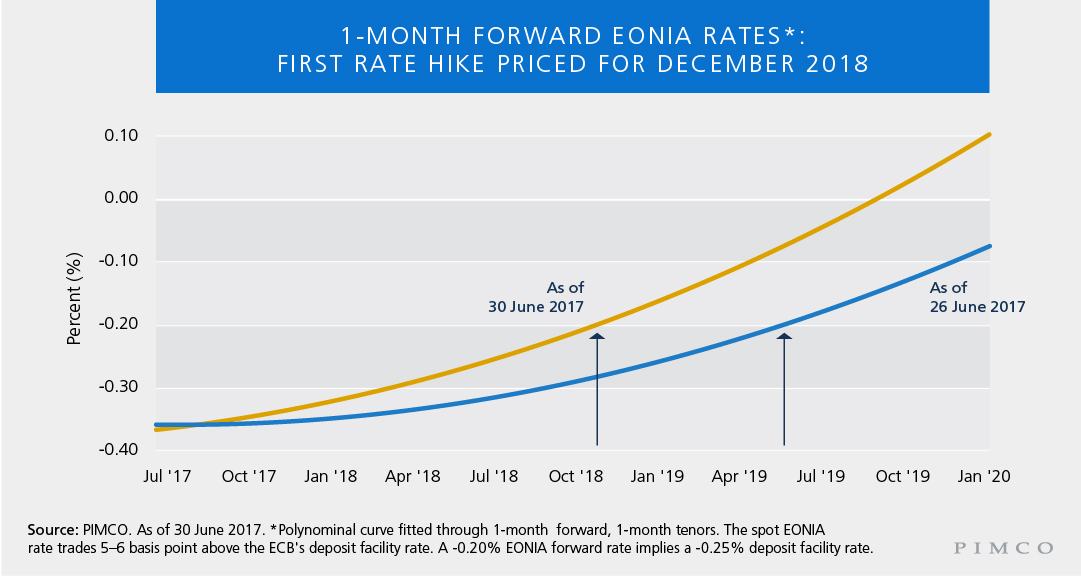

ECB normalization outlook

When it does occur, we think the first deposit facility rate hike will be of only 15 basis points, taking it from −0.40% to −0.25% and restoring symmetry in the ECB’s standing facilities (the marginal lending facility rate is 0.25%, the main refinancing rate 0%). Markets now price that rate hike to occur around December 2018, having priced it to occur around June 2019 prior to Draghi’s Sintra speech. The ECB says its standing facility rates will “remain at their present levels for an extended period of time, and well past the horizon of the net asset purchases.” Assuming “well past” equals six months, current prices therefore imply the market expects the ECB to wind down its quantitative easing (QE) programme by the end of June 2018. We consider that within the bounds of possibilities, but on the aggressive side.

In our baseline outlook, here is what we expect from the ECB:

- Indicate in September and provide details in October that it will taper QE effective January 2018.

- Wind down QE during the second half of 2018, earliest by end June, latest by end December.

- Raise the deposit facility rate in the first half of 2019.

- Discontinue reinvesting the proceeds of bonds purchased under QE in 2020.

While we think markets are enthusiastic in their expectations for policy normalization, we should not forget recent market movements. The long period of easy global monetary policy compressed term (and credit) risk premia. QE contributed to decoupling Bund yields from their anchor of nominal economic growth. Backed by firm improvements in eurozone economic data, recent market moves could go further. Lest we forget, however, real economic output in the eurozone is barely above the level recorded a decade ago (source: Eurostat as of 30 June 2017), and the risk that China’s credit bubble destabilizes world growth is not insignificant. New Normal bond yields are therefore likely to prevail.

Andrew Bosomworth is PIMCO’s head of portfolio management in Germany and a regular contributor to the PIMCO Blog.

© PIMCO

© PIMCO

Read more commentaries by PIMCO