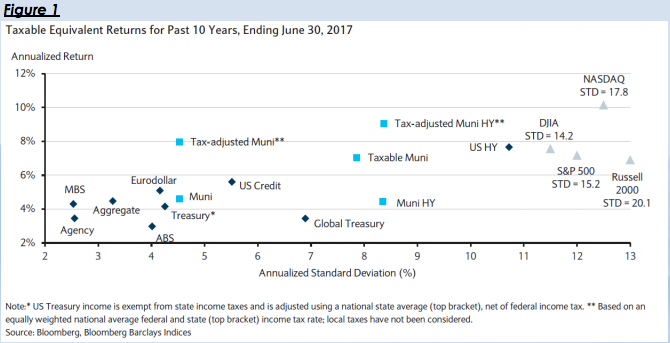

The dramatic recovery in fixed income markets, which began in Q1, persisted throughout the second quarter. Investors increasingly sought safe haven investments in light of geo-political uncertainty and perceived overvaluation in equity markets more broadly. Thirty year U.S. Treasury (UST) bond yields declined by over 17 basis points while one year UST bond yields rose by over 20 basis points. The municipal bond market, once again, outperformed as the Treasury yield curve flattened. Much to the surprise of many investors, on a tax and risk-adjusted basis, municipal bonds have delivered the strongest performance of any asset class over the past ten years, see Figure 1. As measured by the standard deviation (SD) of returns over time, risk was greatest, not surprisingly, in the equity markets. As seen in the S&P 500, 15.2% SD, equities have delivered lower annualized returns with almost 400% more risk/volatility when compared to municipal bonds according to Bloomberg/Barclays research. The risks are greater still in the Russell 2000 Index, 20.1% SD, and NASDAQ Index, 17.8% SD. The Bloomberg/Barclays Municipal Index, by comparison, has a SD of just over 4%. This is an important data point to be mindful of when considering one’s risk tolerance and optimal asset allocation.

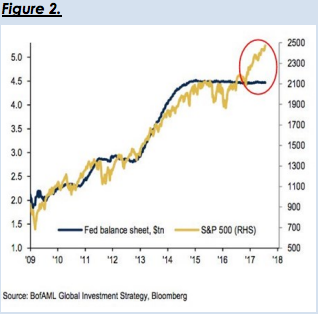

Since the election we have seen the resulting euphoria and hope begin to subside as inflated fixed income yields, resulting from panicked investors fearing dramatically higher economic growth rates, dissipated. The enormity of the political challenges facing the new administration have become more evident with each passing day. A deceleration in inflationary pressures and below trend economic growth provided further evidence to support the view that inflation and economic growth is likely to remain subdued for the foreseeable future. Additional headwinds are sure to be felt as the Federal Reserve seeks to further tighten financial conditions by increasing shortterm interest rates in the face of anemic economic growth. We raised concerns regarding economic stagnation and overvaluation in risk markets in our Q1 2017 commentary. Since that time, a number of other notable investment management firms have voiced similar concerns. These firms include PIMCO, DoubleLine Funds, T. Rowe Price, and Oak Tree Capital. Each of these firms has publicly announced their strongly held view that the US equity market is significantly overvalued and investors should, therefore, consider reducing their exposure accordingly. Figure 2 below, provides a unique illustration of the degree to which the US equity market has dramatically diverged from its highly correlated relationship with the Fed’s balance sheet, according to BOAML/ Bloomberg Analytics. We firmly believe the Fed is intent on reducing the size of its balance sheet in the near-term. Given the high historically positive correlation of equity market valuations and expansionary monetary policy, we believe the associated downside risk in equity prices is material.

Municipal bonds have recovered solidly over the past six months as higher demand for tax-free income resulted in a substantial inflows of new investors into the asset class. Solid demand, together with a limited new issue supply calendar, resulted in municipal bonds, yet again, delivering some of the strongest returns among fixed income investments. Each of our firm’s strategies have delivered strong returns for our clients, both for the quarter and year-to -date. Our emphasis on lower investment grade credits, together with our tactical overweight position in longer-term bonds, contributed meaningfully to performance as the long-end of the municipal bond market outperformed. Lower rated yield spreads narrowed further relative to highgrade bonds, as we found attractive investment opportunities in primary and secondary markets. We have been fortunate to avoid those areas of the market that are experiencing the most distress and offer limited upside for the respective risk. In our view, we continue to avoid bonds backed by the State of IL, Chicago GO’s, Chicago Board of Ed, Puerto Rico in all its forms, as well as Tobacco Settlement bonds. As a reminder, we have no exposure to bonds that have no rating or are nonrated given their extremely low to no liquidity. Investors with limited exposure to longer-term muni bonds and in need of higher tax-free income should consider adding to positions in longer-duration lower rated, yet still stable, municipal bonds, in our view. The relatively steep slope of the municipal yield curve is likely to flatten further as the sun sets on the current US economic expansion. While taxable credit market spreads continue to be meaningfully compressed, municipal bonds spreads in the BB to A category continue to be cheap or in line with longterm averages according to Bloomberg/ Barclays.

In summary, we continue to believe, the Fed’s decision to raise short-term rates, into an economy that is barely growing at 2.00%, will ultimately have the desired impact, slowing growth and reducing speculation in markets that are most overvalued. In the recent Fed minutes, a number of Fed members specifically noted high valuations in equity markets in particular. This is a very rare occurrence and therefore worthy of serious analysis and consideration. It is our view, that the Fed may be concerned that the euphoria that has permeated the risk markets more broadly must be constrained in order to avoid yet another financial calamity. Given limited tools in the Fed tool kit, we share their concern. We continue to monitor economic data closely for any indications of a slowdown in economic growth. As we do, we believe investors will be well served as they wait out the gathering clouds and associated uncertainty in the relative safety of the municipal bonds we select.

If you should have any questions about the best manner in which to take advantage of the prevailing municipal bond market inefficiencies we are seeing, please do not hesitate to contact us directly.

Best Regards,

Andrew Clinton

CEO/Founder

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Clinton Investment Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. The PSN universes were created using the information collected through the PSN investment manager questionnaire and use only gross-of-fee returns. The PSN/Informa content is intended for use by qualified investment professionals. Please consult with an investment professional before making any investment using content or implied content from any investment manager. advice from Clinton Investment Management, LLC. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request.

© Clinton Investment Management

Read more commentaries by Clinton Investment Management