nflation has been calm for so long that many retirement investors have overlooked its potentially corrosive effects. But for defined contribution (DC) plan portfolios designed to last decades, we believe inflation remains one of the greatest potential risks, making inflation-hedging assets critical. In fact, the vast majority of respondents to the 2017 PIMCO DC Consulting Support and Trends Survey supported offering a variety of inflation-hedging strategies in a DC plan’s core investment menu or in a custom target-date strategy.

Although inflation may seem a distant threat, even modest inflation can prove devastating to retirees who depend on income that does not adjust with inflation. After 20 years of 3% annual inflation, for instance, $50,000 in retirement income would buy only about $27,000 worth of goods and services; with 5% inflation, the value shrivels to only about $18,000.

One way to help protect against the threat of inflation is to consider a broad set of diversifiers including real assets like Treasury Inflation-Protected Securities (TIPS), commodities and real estate investment trusts (REITs). These asset classes tend to have low correlations to stocks and bonds and may provide portfolio diversification benefits during inflationary periods, when stocks and bonds may suffer.

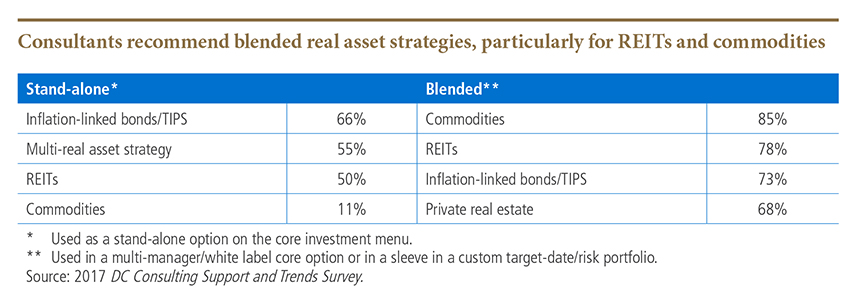

In addition to a stand-alone allocation to TIPS, the majority of consultants surveyed recommended that plan sponsors gain real asset exposure through a multi-asset approach.

Now could be an opportune time to act. PIMCO expects U.S. inflation to average 2% over the secular horizon of three to five years. After years of missing their inflation targets, central bankers appear especially determined to achieve their price-target objectives. The following table shows the percentage of consultants who recommended specific inflation-fighting assets in stand-alone and blended allocations.

© PIMCO

© PIMCO