SUMMARY

- Many investors, nervous after nine years of U.S. economic expansion and market rallies, are seeking to protect gains without losing exposure to risk assets that may continue to appreciate. Two common approaches are constant proportion portfolio insurance (CPPI) and tail risk hedging (TRH).

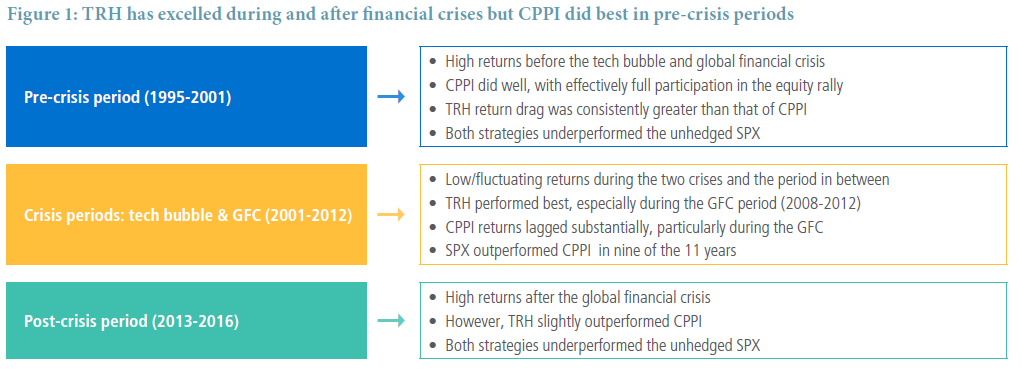

- CPPI would likely be successful in a sustained market sell-off but not participate fully if markets rebound. It effectively locks-in some or all of its portfolio losses.

- TRH seeks to put a floor under portfolio losses in a risk-off event while allowing the underlying portfolio to remain fully invested in risk assets. Given today’s low interest rates and muted equity volatility, investors may find TRH more appealing.

Many investors are nervous after nine years of U.S. economic expansion and rallies that have sent most asset prices to record levels. What strategies can seek to protect gains without losing exposure to risk assets that may continue to appreciate? Two common approaches are constant proportion portfolio insurance (CPPI) and tail risk hedging (TRH). Although both have merit, our historical analysis suggests that TRH may be the preferred strategy given low interest rates and low implied volatility in equity markets.i

CPPI is a low-cost trading strategy that attempts to protect principal and maintain equity market upside potential. It’s been popular historically, especially among more risk-averse equity investors. To seek these seemingly incompatible objectives, however, compromises must be made.

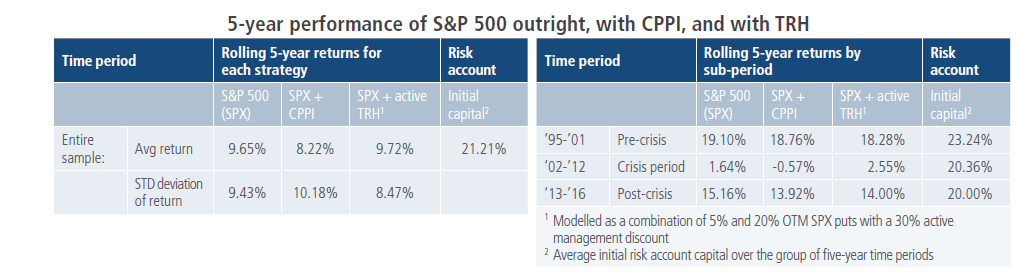

Consider a typical CPPI structure that has a five-year investment horizon, aims to provide a minimum return of 85% of principal at maturity, and maintains initial participation in the equity market at the same level as if the investor had simply invested directly in stocks (i.e., 100% participation). As time passes and market conditions change, the exposure to equities adjusts dynamically to attempt to protect the targeted minimum 85% return of principal at maturity. In practice, if the equity market falls from its initial level, the strategy reduces (and potentially eliminates) its equity exposure – a path-dependent approach.

Investors typically implement CPPI for a five-year term, with the initial investment divided into two accounts:

- A safety account, often invested in short-term government securities, which aims to provide the target minimum return of principal at maturity, and

- A risk account, which contains the balance of the investment and collateralizes the equity market exposure. The beginning equity exposure (taken via futures) is equal to 100% of the total strategy investment, with maximum leverage of five times. As a result, the account can withstand as much as a one-day 20% equity sell-off.ii

This paradigm implies a minimum starting value of 20% in the risk account, with no more than 80% in the safety account. Therefore, given today’s low interest rates, the target minimum return of principal at maturity must be lower than 100%, because the 80% invested in short-term government securities for five years won’t provide enough return to reach 100%.

CPPI dynamically reduces the loss from risk-off events by reducing equity exposure as markets fall, which occurs quickly due to the leveraged nature of the risk account and the ample liquidity of the futures market. Clearly, rapid de-risking is beneficial in a sustained sell-off because it reduces losses as the market moves lower.

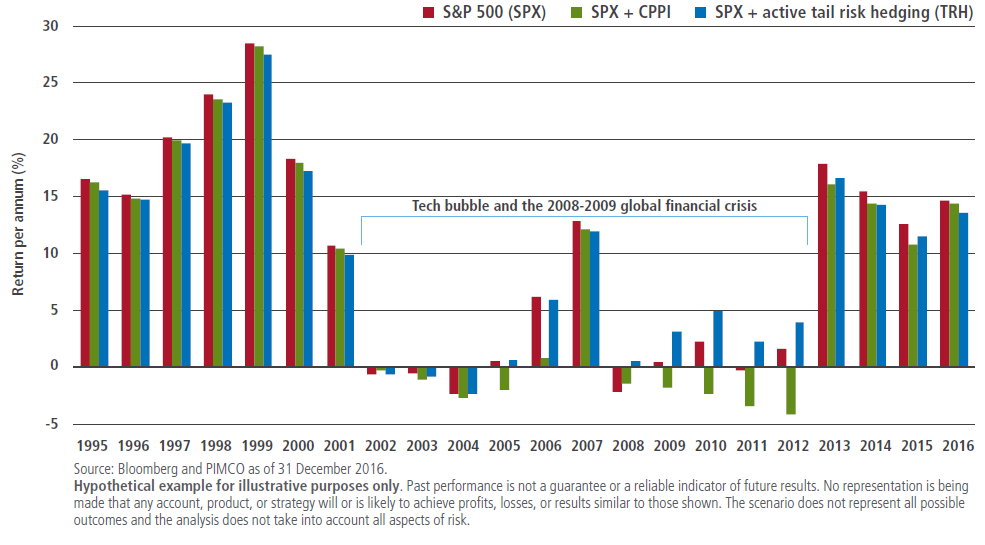

There is a potential drawback, however. If the equity markets rebound, the CPPI structure will not participate fully due to this de-risking (an example of the path-dependent nature of CPPI). This was the case during the 2008 financial crisis, when a hypothetical CPPI strategy (over the five-year investment horizon) would have underperformed the S&P 500 for several years. Effectively, when the strategy de-risks in a crisis, it has “locked-in” some or all of its losses, because there is less participation in a post-crisis rally.