The 10-year U.S. Treasury yield broke 3% on 24 April to much fanfare. Stock markets tumbled, and with the media blitz that followed, many investors may have started to see “3%” in their dreams.

We think crossing 3% – or any particular rate level – is not especially significant in itself. Indeed, it wasn’t long before the yield slipped back to the 2s, a function, in a way, of the many factors we believe are likely to restrain the increase in yields.

Rather than fixating on a particular point estimate, we focus on the long-term factors driving rates, and prudent portfolio construction. Following the global financial crisis we described our New Normal worldview of modest global growth amid headwinds such as aging demographics, low productivity gains and high debt levels. We later outlined our New Neutral view of policy rates, and the likelihood that the federal funds rate would tend toward a neutral level lower than in past cycles.

This month we will revisit our views on these long-term trends at our annual Secular Forum, bringing our investment professionals and distinguished outside speakers together in Newport Beach for three days of presentations and rigorous debates. For now, let’s discuss PIMCO’s views ahead of our forum.

Interest rate outlook

What can investors expect from rates now that the 10-year yield has flirted with 3%? We think historical patterns can provide some guidance.

First, the 10-year Treasury yield has tended in recent cycles to rest where the fed funds rate peaks.

Currently, the fed funds rate is in a range of 1.5%–1.75%. Based on current market pricing, investors are expecting the rate to rise approximately 55 basis points by the end of 2018, bringing it to just over 2.0%. After that, our current New Neutral framework suggests that the fed funds rate will not likely increase beyond the low-3% range. In general, we think secular forces, from high debt loads to demographics and low productivity gains, will keep interest rates lower than in previous rate-hiking cycles. Low global rates will help, too.

Importantly, in stark contrast to 2013 when the 10-year yield also broke 3%, markets today are priced for the Fed to end its hikes below 3%, well below the near-5% that was feared back then.

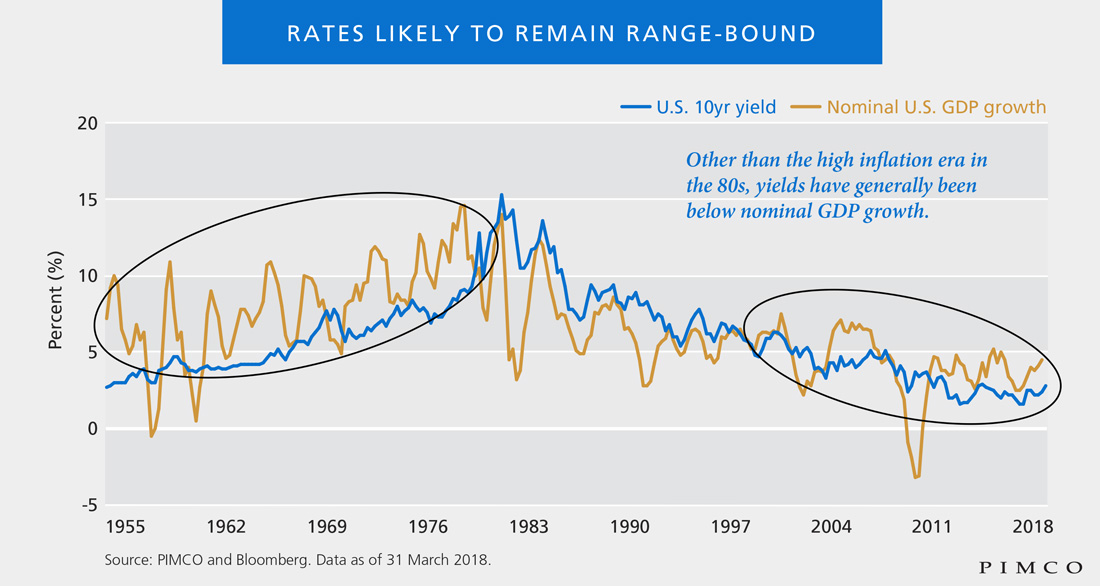

As the chart shows, the 10-year Treasury yield also has a potential resistance level: It has historically stayed below nominal U.S. GDP growth. We do not anticipate GDP going much higher in the foreseeable future, save for a relatively short bump up from fiscal stimulus, and recession is likely over the secular horizon. Moreover, with the Fed still holding trillions of dollars in bonds from its quantitative easing program, yield gains in the current cycle will be constrained.