Master limited partnership (MLP) investors received some good news last week. The Federal Energy Regulatory Commission (FERC) issued a final ruling that clarifies and softens a previous order issued in March, which would have disallowed a long-standing policy enabling MLPs to earn an income tax allowance in their pipeline rates. The March ruling precipitated a 13% drop in the Alerian MLP Index and hit MLPs exposed to natural gas especially hard (due to the regulated nature of these assets), with many correcting to 10-year lows.

The final FERC ruling issued 18 July essentially excludes MLPs with a C corporation parent – the most common ownership structure – from the proposed policy changes. The modified ruling triggered sharp rebounds for the names hurt most by the March policy announcement, helping the Alerian index close up 2.9% over the past three days and bringing overall year-to-date gains to 2.4%.

While the final order pertains primarily to long-haul natural gas pipelines, we see positive implications for MLPs in general, including regulated liquids pipelines, as it indicates FERC’s willingness to update its views and provides a supportive backdrop for returns on capital employed.

Simplification transactions will likely move forward

To overcome the headwinds arising from the March proposal, a number of MLPs announced simplification transactions that would convert them from MLP structures into traditional C corporations. Although the final ruling appears to diminish the need for some to do so, we expect these transactions to go forward nonetheless given other potential benefits. These include lowering their cost of capital, reducing the complexity of their corporate structures and broadening their investor bases, given that MLPs are not included in most broad-market equity indexes.

Investor takeaways

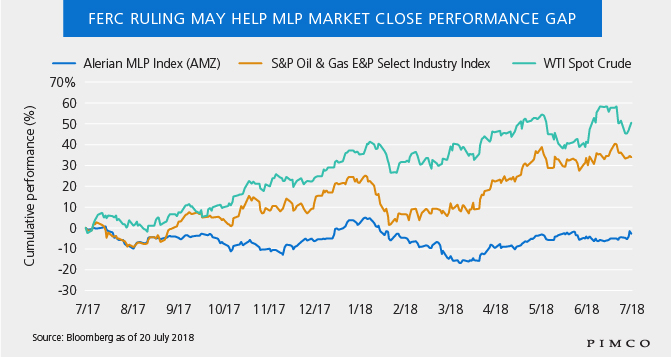

We see the tide turning for the midstream energy sector after a frustrating few months and four years of underperformance, during which the Alerian index corrected 31%. The FERC’s surprise announcement in March overshadowed an otherwise healthy first-quarter 2018 earnings season, where many beat expectations owing to higher commodity prices, production growth and solid margins. While still early, second-quarter earnings appear to be off to a good start, and we expect the underperformance of the Alerian index relative to the S&P Oil & Gas E&P Select Index and WTI spot prices to narrow in coming months (see chart).

Several key factors support our constructive view on MLPs, including still-high starting yields, improving company fundamentals, attractive valuations relative to high yield and other income-oriented sectors, and a robust oil and gas production backdrop. This utility-like sector currently offers an attractive yield of around 8% with potential for mid-single-digit distribution growth (pointing to 12%–14% total return potential over the next 12 months), supported by fee-based cash flows backed by long term take-or-pay contracts.

Investing in midstream energy isn’t without risks, including commodity price risk as well as shifts in macroeconomic or investor sentiment, interest rate expectations or a particular issuer’s financial condition. Nonetheless, we believe MLPs may offer compelling risk-adjusted returns in today’s market.

John M. Devir and Danny Seth are portfolio managers on PIMCO’s MLP & Energy Infrastructure strategy and are contributors to the PIMCO Blog.

DISCLOSURES

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in MLPs involves risks that differ from equities, including limited control and limited rights to vote on matters affecting the partnership. MLPs are a partnership organised in the US and are subject to certain tax risks. Conflicts of interest may arise amongst common unit holders, subordinated unit holders and the general partner or managing member. MLPs may be affected by macro-economic and other factors affecting the stock market in general, expectations of interest rates, investor sentiment towards MLPs or the energy sector, changes in a particular issuer’s financial condition, or unfavorable or unanticipated poor performance of a particular issuer. MLP cash distributions are not guaranteed and depend on each partnership’s ability to generate adequate cash flow. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

Return assumptions are for illustrative purposes only and are not a prediction or a projection of return. Return assumption is an estimate of what investments may earn on average over the long term. Actual returns may be higher or lower than those shown and may vary substantially over shorter time periods.

The Alerian MLP Index is the leading gauge of large- and mid-cap energy master limited partnerships (MLPs). It is a float-adjusted, capitalization-weighted index, which includes 50 prominent companies. It is not possible to invest directly in an unmanaged index.

© PIMCO

© PIMCO

Read more commentaries by PIMCO