Japanese government bonds yield virtually zero. Yields on German bunds remain stuck below 50 basis points (bps). U.K. gilts yield only about 125 bps. Do non-U.S. bonds such as these hold any value to dollar-based investors?

Yes, quite a bit, it turns out.

For a dollar-based investor, hedging foreign currency exposure on lower-yielding global bonds may potentially result in higher yields than U.S. Treasuries. Essentially, investors are getting paid to hedge the currency risk back to the US dollar. Other potential benefits for those who invest internationally and hedge their U.S. currency exposure include improved diversification and defense against rising U.S. interest rates.

Why hedging may pay

Despite low bond yields in many countries outside the U.S., hedged yields may be quite attractive for U.S. dollar-based investors. The yield to maturity of hedged global bonds (as represented by the Bloomberg Barclays Global Aggregate Index ex-USD (USD Hedged)) was 3.16% as of 30 June 2018 – nearly equal to the 3.27% for the main U.S. bond index (represented by the Bloomberg Barclays US Aggregate Bond Index).

How is that possible? Hedging foreign currencies back to the U.S. dollar currently adds about 220 bps of carry because of favorable short-term interest rate differentials. In order to hedge currency exposure in a foreign bond, investors effectively pay the short-term rate in the foreign currency and receive the short-term rate in their home currency.

If short-term rates for U.S. dollars are higher than those for the target currency – as they are in many cases today – the cost of hedging may be negative; in other words, investors could get paid to hedge.

We expect this dynamic to continue over the cyclical (six- to 12-month) horizon as the Federal Reserve continues to raise rates while most other developed market central banks remain on hold.

Other potential benefits

The investment case for global bonds is not just about relative yields. Harry Markowitz, a Nobel laureate economist and the father of modern portfolio theory, called diversification “the only free lunch in finance” for its potential to reduce risk without sacrificing returns. Global bonds are a great example of the potential benefits of diversification.

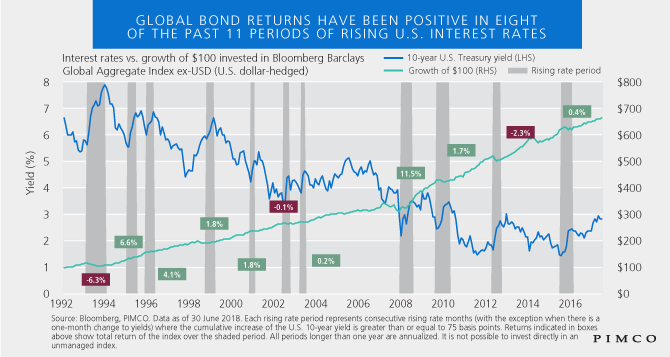

Case in point: Global bond returns were positive in eight of the past 11 periods of increasing U.S. interest rates (see chart). In the first six months of this year, they delivered a positive return of about 1.4%, while the Bloomberg Barclays US Aggregate Bond Index fell around 1.5%.

Because economic cycles and hence monetary policies are not in perfect alignment globally, diversification into global bonds may reduce portfolio volatility by giving investors exposure to countries with varying yield curves. In a way, because economic cycles vary across countries, there is a natural rotation of best- and worst-performing global bond markets. At times, this may allow global bonds to help dollar-based investors buffer their portfolios from the effects of rising U.S. interest rates.

Even during periods of stress, when correlations between U.S. and global bonds increase, global bond markets may not be perfectly correlated, so diversification potential remains.

In sum, we view global bond strategies like broccoli in your diet – if consumed regularly, they may deliver sustained benefits over time.

Sachin Gupta is head of PIMCO’s global portfolio management desk. Olivia Albrecht is a strategist focused on global fixed income.

DISCLOSURES

Past performance is not a guarantee or a reliable indicator of future results. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Derivatives may involve certain costs and risks, such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. Diversification does not ensure against loss.

Statements concerning financial market trends are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

© PIMCO

© PIMCO

Read more commentaries by PIMCO