In its trade war with the US, China may not ultimately have the upper hand, but it is not without its own weapons of war.

The first is its currency. By keeping it artificially low, it can offset what would otherwise translate into price increases on its exports to the US. Keeping prices down may help China maintain its market share, but such a move comes at a cost.

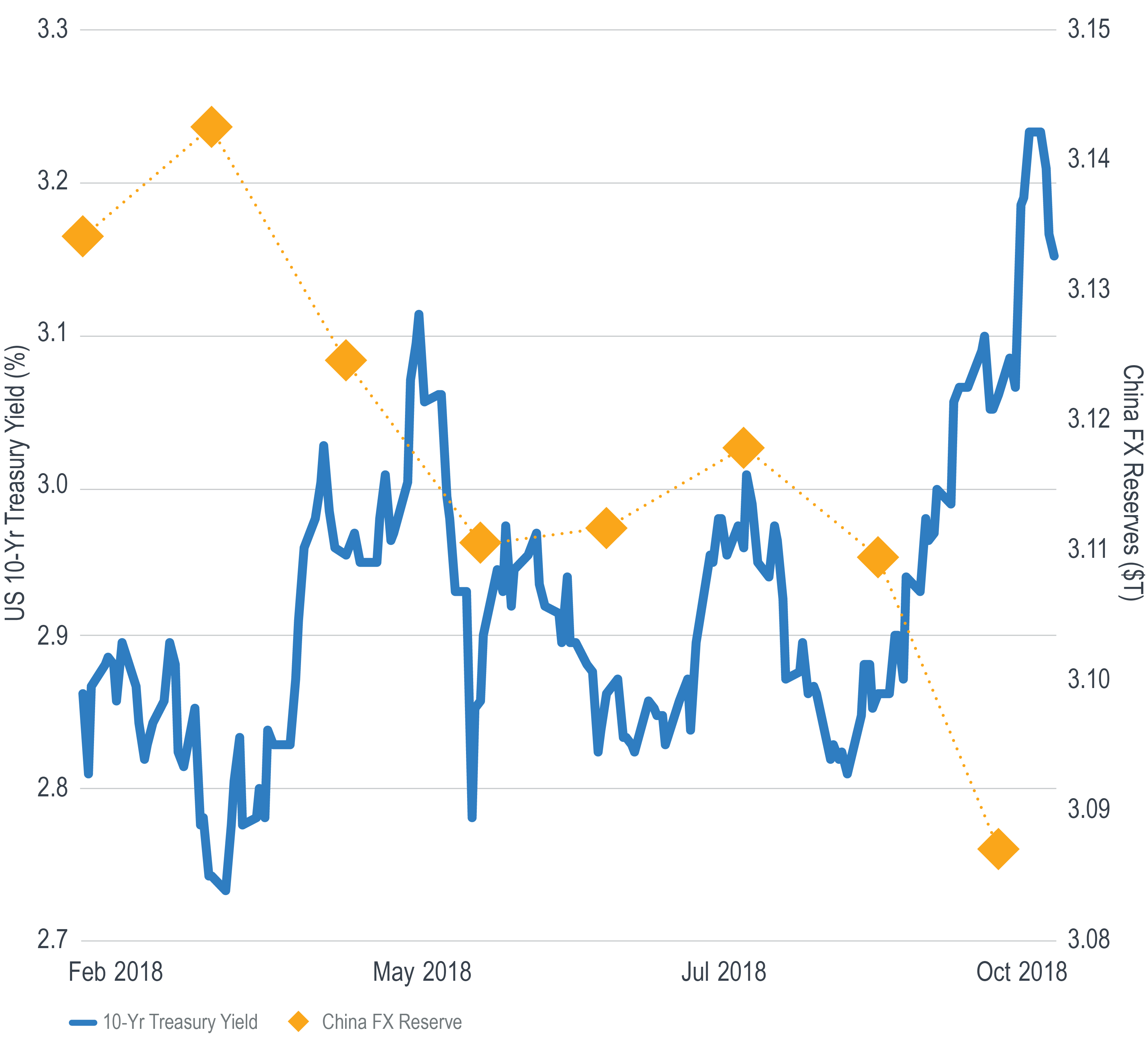

The second weapon is its holdings of US Treasury bonds. The most recent data from the US Treasury show that with $1.17 trillion of US Treasury bonds China is the largest foreign holder.1 By selling its sizable holdings, China has the potential to generate upward pressure on US interest rates.

Perhaps not coincidentally, US Treasury yields have been trending higher this year while China has been gradually reducing its foreign exchange reserves.

Just this week, the White House announced that President Trump would meet with Chinese President Xi Jinping at the G20 meeting next month to ease the escalating trade tensions.

Given recent market turmoil, market participants will be keeping a close eye on how the trade talks unfold.

1As of July 2018, posted at treasury.gov on September 18, 2018.

Unless otherwise noted, data is sourced from Bloomberg.

Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

The results shown are historical, for informational purposes only, and do not guarantee future results.

Any discussion of risks contained herein with respect to any product or service should not be considered a disclosure of all risks or a complete discussion of the risks involved.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.

Data included in this document has been sourced from providers that Milliman FRM believes to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by Milliman FRM as to the accuracy or completeness of the source data or any other information in this document.