Munis In Focus

Short term rates have been on the rise over the past few years as the Fed has implemented its consistent, yet gradual, rate hikes, including the most recent increase in the Federal Funds Rate in September. Volatility also returned to the markets in October, affecting both stocks and bonds, as geopolitical tensions, trade frictions, and mixed earnings guidance fueled a broad market sell-off. Additionally, muni funds have seen several consecutive weeks of outflows, totaling $3.96 billion in the month of October. These outflows have been across all fund categories, starting in September and continuing through the entirety of October. The chart below shows the connection between the increasing volatility in the muni market and the subsequent outflows.

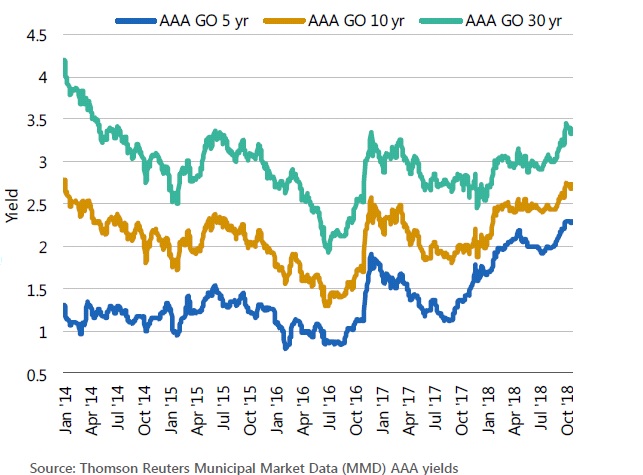

Together, these market conditions have culminated in muni yields increasing to levels that have not been seen since 2014, across all portions of the municipal yield curve. Municipal yields have been rising for the majority of 2018, reversing course after falling throughout 2017 (see chart below). Tax reform, along with the increased volatility in markets and the recent outflows in muni mutual funds, has led to a slightly steeper muni curve than September’s curve. The MMD curve also remains significantly steeper than the US treasury curve. At the end of October, the 30 year MMD/UST ratio was 100% with the 30 year AAA GO yield at 3.38, versus 3.39 for the 30 year treasury yield. At the short and intermediate portions of the curve, the AAA GO 5 and 10 year yields have been climbing steadily for much of 2018, and both are at their highest levels in years, at 2.30 and 2.73 respectively, as of October 31. When adjusted for taxes, munis have offered returns in line with equities with about half the volatility – a key potential benefit when markets turn. And despite isolated high profile downgrades, municipal fundamentals have improved and defaults remain low versus comparably rated corporate bonds. While credit challenges when the cycle turns will likely make active credit selection critical, we believe munis may offer U.S. taxpayers compelling advantages as they contemplate the end of the economic expansion.

Muni Open End Flows vs Volatility

AAA Go Historical Yields

AAA Go Historical Yields

DISCLOSURES

Past performance is not a guarantee or a reliable indicator of future results.

A Word About Risk: Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investors will, at times, incur a tax liability. Income from municipal bonds is exempt from federal tax but may be subject to state and local taxes and at times the alternative minimum tax.

The Bloomberg Barclays Municipal Bond Index is a rules-based, market-value-weighted index engineered for the long term tax-exempt bond market. The Bloomberg Barclays High Yield Index is an unmanaged market-weighted index including only SEC registered and 144(a) securities with fixed (non-variable) coupons. The Bloomberg Barclays High Yield Municipal Bond Index is a rules-based, market-value-weighted index that measures the non-investment grade and non-rated U.S. tax-exempt bond market. It is not possible to invest directly in an unmanaged index.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

PIMCO does not provide legal or tax advice. Please consult your tax and/or legal counsel for specific tax or legal questions and concerns.

The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Any tax statements contained herein are not intended or written to be used, and cannot be relied upon or used for the purpose of avoiding penalties imposed by the Internal Revenue Service or state and local tax authorities. Individuals should consult their own legal and tax counsel as to matters discussed herein and before entering into any estate planning, trust, investment, retirement, or insurance arrangement.

This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. PIMCO Investments LLC, distributor, 1633 Broadway, New York, NY, 10019 is a company of PIMCO.

© 2018 PIMCO.

CMR2018-1119-365893

© PIMCO

Read more commentaries by PIMCO