Munis in Focus – Midterm Elections

The US midterm elections took place in November, and, as was predicted, Democrats took control of the House while Republicans increased their majority in the Senate. Given these results, expectations for further progress in the Republican agenda are slim. Infrastructure and investigation headlines are expected to dominate the conversation going forward. Democrats want to show they can govern and will focus on issues of agreement, including infrastructure, criminal justice reform, and drug pricing. The chances of an infrastructure spending bill depend on how Democrats propose to pay for it, and it will likely have to happen by spring/summer of 2019 to have a chance to pass. Nancy Pelosi is expected to be Speaker, which decreases the chance of impeachment as she focuses on proving she and the other Democrats can govern alongside President Trump. The Senate is more red and will be easier for Trump to get his folks confirmed, which is evident as a cabinet shuffle has already started as a result. This will also allow the judiciary to become more red-leaning.

On the municipal front, most of the $76.3 billion of bond sales were approved, which was the most on the ballot since 2006. Two key races had credit implications for munis going forward. In Illinois, democrat JB Pritzker won the election for governor. Pritzker campaigned on a progressive agenda that he plans to fund through instituting a progressive income tax, which requires a state constitutional amendment. Given Illinois’s budgetary challenges emanating from pension funding deficits, additional revenue would be viewed favorably. In California, Gavin Newsom (D) beat John Cox (R) as expected. Newsom is viewed as a modest credit negative as his agenda includes several large social policies that will challenge the state’s resources or possibly result in higher taxes. Lastly, several states passed Medicaid expansion bills that will lead to additional coverage gains, which is a credit positive for non-profit health systems in those states.

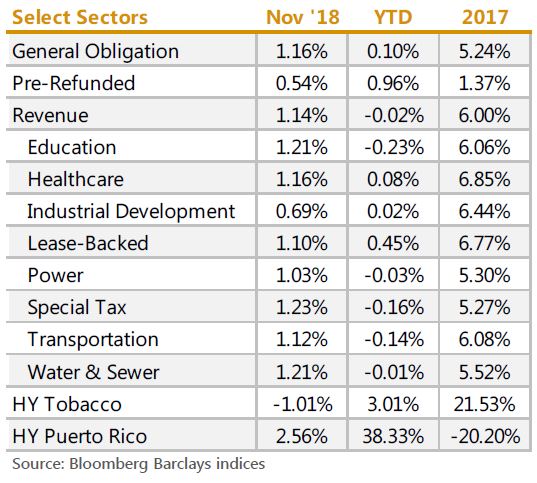

SECTOR RETURNS

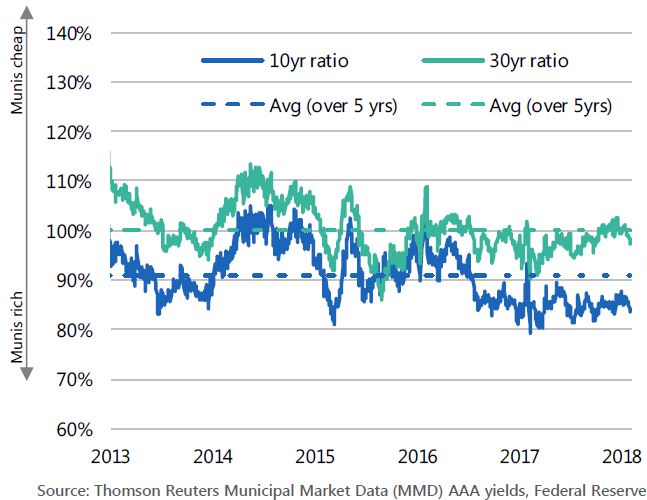

MUNICIPAL/TREASURY YIELD RATIO

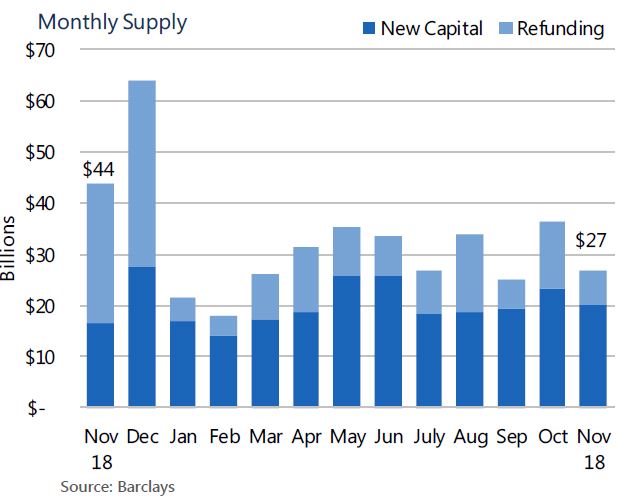

MUNICIPAL MARKET ISSUANCE

DISCLOSURES

Past performance is not a guarantee or a reliable indicator of future results.

A Word About Risk: Investing in the bond market is subject to risks,including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investors will, at times, incur a tax liability. Income from municipal bonds is exempt from federal tax but may be subject to state and local taxes and at times the alternative minimum tax.

The Bloomberg Barclays Municipal Bond Index is a rules-based, market-value-weighted index engineered for the long term tax-exempt bond market. The Bloomberg Barclays High Yield Index is an unmanaged market-weighted index including only SEC registered and 144(a) securities with fixed (non-variable) coupons. The Bloomberg Barclays High Yield Municipal Bond Index is a rules-based, market-value-weighted index that measures the non-investment grade and non-rated U.S. tax-exempt bond market. It is not possible to invest directly in an unmanaged index.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

PIMCO does not provide legal or tax advice. Please consult your tax and/or legal counsel for specific tax or legal questions and concerns. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Any tax statements contained herein are not intended or written to be used, and cannot be relied upon or used for the purpose of avoiding penalties imposed by the Internal Revenue Service or state and local tax authorities. Individuals should consult their own legal and tax counsel as to matters discussed herein and before entering into any estate planning, trust, investment, retirement, or insurance arrangement.

This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. PIMCO Investments LLC, distributor, 1633 Broadway, New York, NY, 10019 is a company of PIMCO.

©2018 PIMCO.

CMR2018-1212-370028

© PIMCO

Read more commentaries by PIMCO