Chart of the week: 02/11/2019 – 02/15/2019

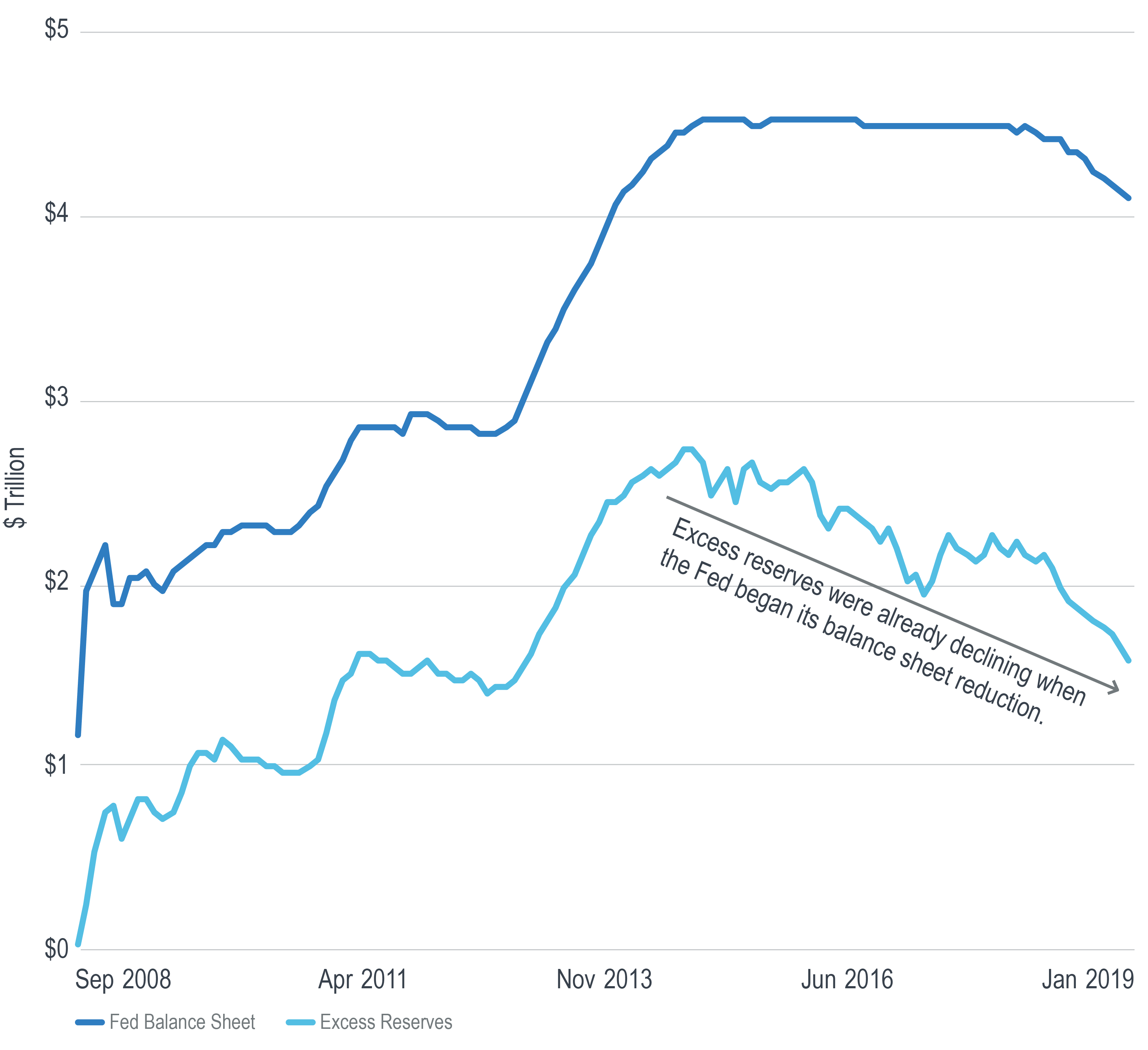

Size of Fed Balance Sheet and Excess Reserves

Is the Fed on a course to resume QE?

The Fed’s implementation of quantitative easing (QE) and the subsequent growth of its balance sheet resulted in the creation of $2.7 trillion in excess reserves in the banking system.

With the existence of excess reserves, the Fed lost its ability to control the fed funds rate via conventional reserve management. As a result, the Fed has had to resort to using the reverse repo market and the interest rate on excess reserves (i.e., the administered rates) in order to control the fed funds rate.

After the size of the balance sheet peaked in January 2015, the Fed didn’t begin actively shrinking it until October 2017. During those 22 months, however, excess reserves in the banking system had already started declining as banks continued to issue more loans. Since then, the implementation of quantitative tightening (QT) via balance sheet reduction has accelerated the decline in excess reserves.

A continuation of loan growth and QT would eventually eliminate all excess reserves from the system. That, in turn, would enable the Fed to control the fed funds rate just as it did prior to the financial crisis, a practice one might reasonably assume the Fed would want to return to. Recent comments from Chairman Powell, however, suggest that this is not the case.

After a dovish pivot on rates in the January 30th FOMC meeting, Powell noted in the post-meeting press conference,

“We want to have a buffer because we want to be operating in an abundant reserves regime, where we operate through our administered rates. If you operate too close to that point of scarcity then you wind up having to have these big ongoing interventions in the market. We don’t want the Fed to have a large ongoing presence in the market around this, in managing the Fed funds rate. We’d rather have it set by our administered rates.”

If loan growth continues to reduce the amount of excess reserves, and the Fed continues to insist on using the administered rates that excess reserves require, it would seem that eventually the Fed will not only have to stop QT, but will have to actually resume QE in order to maintain Powell’s “buffer.”

Among the many questions this raises, none may be more important or interesting than, “why is the Fed doing this?” and “what are the risks for the financial system?”.

The answers to these questions and others related to them will be important for market participants to understand as the Fed’s post-crisis policy continues to evolve.

Unless otherwise noted, data is sourced from Bloomberg.

Recipients must make their own independent decisions regarding any strategies or securities or financial instruments mentioned herein.

The products or services described or referenced herein may not be suitable or appropriate for the recipient. Many of the products and services described or referenced herein involve significant risks, and the recipient should not make any decision or enter into any transaction unless the recipient has fully understood all such risks and has independently determined that such decisions or transactions are appropriate for the recipient.

The results shown are historical, for informational purposes only, and do not guarantee future results.

Any discussion of risks contained herein with respect to any product or service should not be considered a disclosure of all risks or a complete discussion of the risks involved.

The recipient should not construe any of the material contained herein as investment, hedging, trading, legal, regulatory, tax, accounting or other advice. The recipient should not act on any information in this document without consulting its investment, hedging, trading, legal, regulatory, tax, accounting and other advisors.

The materials in this document represent the opinion of the authors and are not representative of the views of Milliman, Inc. Milliman does not certify the information, nor does it guarantee the accuracy and completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express consent of Milliman.

Data included in this document has been sourced from providers that Milliman FRM believes to be reliable from information available publicly or with consent of the provider of the source material. To the fullest extent permitted by law, no representation or warranty, express or implied is made by Milliman FRM as to the accuracy or completeness of the source data or any other information in this document.