Ever wonder how factors such as inflation and gross domestic product (GDP) (also known as macroeconomic influences) affect the markets and investing? They pop up in financial news headlines all of the time, but why should the average investor care about them?

Let’s look at some of these factors, the market “regimes” they form, and how analyzing these regimes is helping us develop our latest pioneering risk-managed investment strategies.

Before I get into discussing the future of Flexible Plan, let me share a bit about the past that shaped it.

The dark ages of data and computing

Back in the 1970s when Flexible Plan’s founder and president, Jerry Wagner, laid the groundwork for our rules-based approach to investing, actionable data of all types was hard to come by. Market data—items such as advancing and declining issues, new highs and lows, prices of indexes, and interest rates—was usually provided by subscription and delivered in hard copy. This meant the data was generally limited and slow to arrive.

The same was true of economic data—items such as GDP, inflation, and unemployment figures. In fact, economic data usually got to reporting agencies and industries more slowly than market data. It was also often significantly revised and trickled out to the public at a snail’s pace. This patchy, slow stream of data meant that most early rules-based investment strategies relied largely on market data.

Further limiting the development of strategies during this time was the computing power available. The computers of the 1970s and 1980s were slow and had limited memory and data storage.

Furthermore, the internet was not widely available until well into the 1990s. Up until that time, data had to be manually entered into the computers that we did have.

Now, computing power is nearly unlimited and market data is abundant and timely. Macroeconomic data is also readily collected and delivered to those who want it. These factors have allowed firms such as Flexible Plan to explore the influences of macroeconomic forces on markets. What we are learning is that these forces not only have a meaningful influence on markets, but they may be able to be quantified in a way that is useful in developing and guiding our investment strategies.

The influence of market “regimes”

Flexible Plan has studied many different macroeconomic data inputs and their influences on markets. Among the more influential of these inputs are the trend of GDP and inflation. When considered together, we get four possible combinations of these measures, resulting in what we refer to as “regimes.” The following table shows these combinations and the approximate percentage of time that we have spent in each regime.

Our research indicates that knowing what macroeconomic regime we are in is important in understanding market moves, so we display the current market regime on our website.

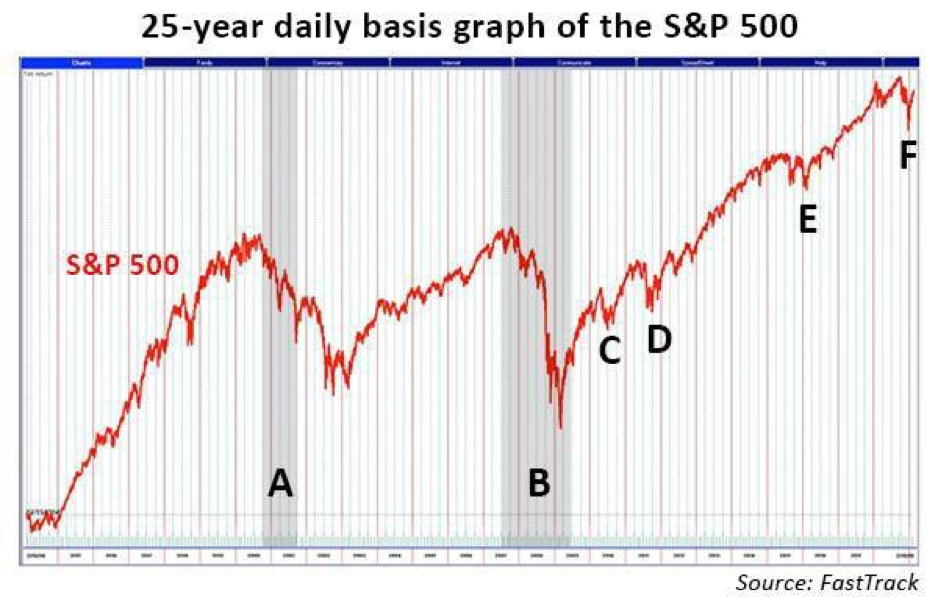

A way to understand the influence of regimes on markets is to look at how markets act when the economy is in a recession. A recession is characterized by a period of falling GDP (whether inflation is rising or falling is inconsequential). The following graph illustrates that the most significant declines in the stock market tend to align well with periods of falling GDP. The shaded areas labeled A and B represent the two most recent economic recessions as defined by the St. Louis Federal Reserve.

During these recessionary periods, stock market declines were prolonged, significant bear markets that erased more than half the value of the stock market and many stock portfolios.

It gets more interesting as we explore this concept a bit further. We have had a number of meaningful market declines in recent years during periods when we were not in an economic recession. Several of those corrections are labeled C, D, E, and F in the previous graphs. Those corrections were typically limited in magnitude (generally less than 20%) and usually short-lived, lasting a few months rather than more than a year. This difference between short-lived corrections in periods of growing GDP versus bear markets in periods of contracting GDP raises questions of how rule sets for investment strategies may be adapted to act differently depending on what regime is influencing the market.

Using knowledge of market regimes to help investors

As markets have evolved, data availability has improved, and computing power has increased, Flexible Plan has continued to examine what influences markets and how those influences may be harnessed on behalf of investors.

For example, based on what we have discussed about market regimes, it is logical that during a rising GDP regime we would want to develop a strategy rule set that biases the strategy toward moving into and staying invested in equities (to the extent permitted by an investor’s risk profile), while making it somewhat resistant to getting out of equities. Conversely, if we know we are experiencing a declining GDP economy, we would want to develop strategies that are biased toward being defensive and resistant to investing in equities.

Please note that I deliberately chose the words “biased” and “resistant.” Our research indicates that it would not be beneficial to build a rule set for a strategy that ignored market data entirely and paid attention only to macroeconomic data. Why? Because markets tend to move in advance of changes in macroeconomic conditions. This is not to say that markets (and market data) are always correct. Frequent, short-lived corrections highlight that markets often erroneously anticipate changes in macroeconomic conditions. Within rule sets, no one rule is the key to success. The use of regimes in rules-based strategies is but another tool that may be used in increasing their effectiveness.

At Flexible Plan, we have a large Research team that is continually in pursuit of ways to manage the risks associated with investing and how to take advantage of the opportunities presented by the markets in which we invest. Near the top of the Research project list today is the study of regimes and how to have strategies and portfolios self-adapt their respective rule sets over time as the more influential regimes change.

It is the nature of markets, economies, governments, and technology to change over time. For that reason, we will forever be adapting existing strategies and developing new ones to provide thoughtful, tested, dynamically risk-managed options for investors to use in the pursuit of their financial goals.

FPI Research update

With equity markets up last week, our trend-following equity strategies did very well. But it was our recently reformulated S&P Tactical Patterns strategy that outperformed all of our strategies, nearly doubling the S&P 500 Index’s return for the week. WP Aggressive also did well, rising over 3.5%.

Other strategies had a difficult time navigating the market environment: Sector Index Rotation was down about 1.9% for the week, and Managed Income Aggressive was down about half a percent for the week as long-term Treasurys fell slightly for the week.

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS. Inherent in any investment is the potential for loss as well as profit. A list of all recommendations made within the immediately preceding twelve months is available upon written request. Please read Flexible Plan Investments’ Brochure Form ADV Part 2A carefully before investing. View full disclosures.

© Flexible Plan Investments

Read more commentaries by Flexible Plan Investments