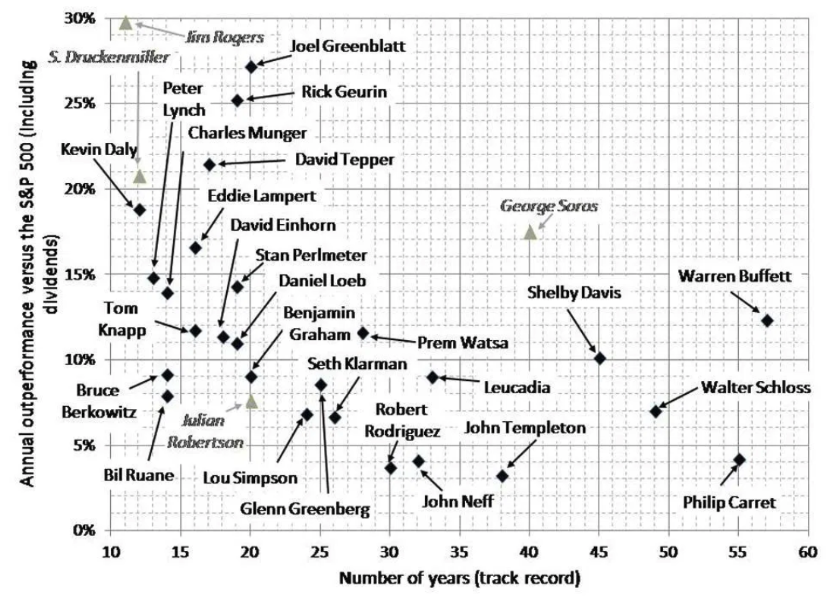

Warren Buffett has one of the greatest long-term investing track records of all time. The chart below shows the excess return (y-axis) over the market of some of history’s best performing investors and the number of years (x-axis) behind each track record – Buffett is way over to the right highlighted in yellow. Buffett’s total excess return over the market, a result of compounding 55+ years of market beating returns, may never be matched by any investor again.

Source: Excess Returns: A Comparative Study of the Methods of the World’s Greatest Investors

Disappearing Alpha

But over the last 10-20 years, it’s been a different story for Buffett’s alpha. Berkshire Hathaway has trailed the market since January of 2009, and if you go back to the year 2000, while there’s alpha in Berkshire’s 9.2% annual return, it’s less than half of Berkshire’s 20.3% annualized return back to 1965.

Buffett’s returns are often touted in the press, but even Warren himself admits future returns won’t be anywhere close those generated in the first 25 years of Berkshire’s existence. It’s the reality given Berkshire’s size, opportunity set, competition and more. But in classic Buffett style, he’s been honest with investors, saying publicly that the returns of the Berkshire and the U.S. market, from this point forward, will be “very close to the same”.

Investors Sticking With the Program

So while Buffett’s ability to generate long-term alpha may be disappearing, it was a recent discussion with Dr. Wes Gray of Alpha Architect, Toby Carlisle of the Acquirers Funds and the investing team at Resolve Asset Management – Adam Butler, Rodrigo Gordillo and Mike Philbrick – along with a comment from an investor who watched our recent podcast, “Can Warren Buffett Be Quantified”, that got me thinking about the contributions Buffett has made that go beyond his investment track record.

On ReSolve's Riffs on Value Investing podcast, Wes, Toby and the Resolve crew (all quantitative investing practitioners) dedicate some time to talk about Buffett, the underperformance of value stocks and Berkshire’s returns post 2009.

Around the 20-minute market, Wes makes a very good point. What’s impressive about Buffett, he says, isn’t so much the returns (whether they are market beating or not in the current environment), but rather how many investors have stayed invested in the stock, despite it trailing the market. As Wes explains, lots of Berkshire investors have bought into Buffett’s investing philosophy and process and have stuck with the program. The fact that they’ve stayed committed to Buffett, and not focused on short or medium-term results, is perhaps the greatest service Buffett has done for his investor base.

And we can back this up with a little data from Lawrence Cunningham, professor at George Washington University and author of multiple books on Buffett and Berkshire, from this MarketWatch piece.

Cunningham defines what he calls “high quality” shareholders. These are shareholders that “acquire large stakes and hold them for long periods. They see themselves as part-owners of a business, understand operations and focus on long-term results, not current market prices,” writes Cunningham. It’s these kinds of investors that most companies want investing in their stock, and in the case of Berkshire, the data reported by Cunningham shows it's exactly these types of investors he is attracting.

Berkshire’s High Quality Shareholder Base

- “Almost all Berkshire shares were held by concentrated investors — their Berkshire holdings being twice their next largest position”

- “98% of Berkshire shares outstanding at year-end were owned by those who owned at the beginning of the year”

- Buffett’s success in attracting QSs has been an important reason for Berkshire’s success. They gave him a long-term runway, helped promote a rational stock price and deterred shareholder activists from seeking to break up the conglomerate as it grew.

Eight Timeless Buffett Contributions That Go Beyond Performance

I would argue that the contributions, ideas and principles Buffett has consistently communicated over time, now transcends his performance and has much wide influence. I've attempted to come up with eight timeless contributions that go beyond his track record to try and get at the core reasons why investors believe in and trust Buffett even if the long-term alpha potential is fleeting. These views fan out further than just Berkshire, and financial advisors and those managing money for investors can learn from ideas, principles and concepts that Buffett has continuously espoused over the years that have contributed to developing a trust and commitment from investors that is probably unrivaled in the world of investing today

1 Educating

If you were to pick just one piece of investment related reading a year, I would argue it should be Buffett’s annual letter to shareholders (you can read all the letters back to 1977 here). While the letters have sometimes had a specific focus, there is a consistent drumbeat to most of his messages – it basically comes down to long-term buying of good businesses at what are hopefully reasonable prices, controlling your temperament and believing in the U.S. stock market and corporate America over time

In a podcast with David Perrel, Wall Street Journal Columnist Jason Zweig highlights and praises Buffett and Charlie Munger’s long-term consistency in espousing their investment beliefs.

What’s remarkable about both Charlie Munger and Warren Buffett is that every year for decades at the Berkshire Hathaway meaning they’ve taken on this task of answering questions on any topic from anybody. And, remarkably, they always give the same answers and people keep coming back. And I think it’s because that sort of constant is rare in the business community and in public life as well. And people appreciate always hearing the same message delivered the same way.

Consistent messaging and driving home their investing philosophy year after year are big reasons why stockholders stick with Buffett over time.

2 Promoting the importance of controlling emotions and combating biases

One of my favorite quotes from Buffett is below:

“To invest successfully does not require a stratospheric IQ, unusual business insights, or inside information. What’s needed is a sound intellectual framework for making decisions and the ability to keep emotions from corroding the framework.”

In The Intelligent Investor, Ben Graham, Buffett’s mentor, wrote about the concepts of margin of safety, investing over speculating, and not letting Mr. Market, which can be irrational in the short run, get the best of you. Graham’s teaching and writings were instrumental in shaping Buffett’s views on investing. As he said in his 1987 letter to shareholders, “Ben Graham, my friend and teacher, long ago described the mental attitude toward market fluctuations that I believe to be most conducive to investment success.”

Graham, and then Buffett, were writing about behavioral finance decades before behavioral finance was even a finance subject. They understood the important to emotional discipline and long-term thinking.

As Ben Graham once said, “In the short run, the market is a voting machine but in the long run it is a weighing machine.” What this means is that in the short-term the popularity in the stock market means a lot but over time it’s the underlying fundamentals that matter the most.

3 Being a long-term optimist

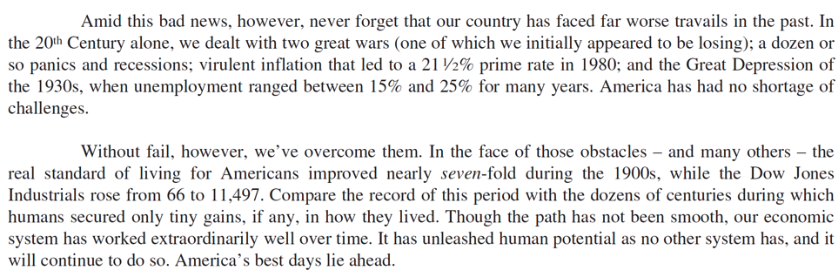

The paragraphs below were taken from Berkshire’s 2008 annual shareholder letter. Buffett has always remained a steadfast, long-term optimist on America and capitalism. He may not always think stocks are cheap, but the idea that as a country and economy we are advancing and the cash flows generated by corporate America will be higher in the future are continuous reminders from Buffett.

Source: 2008 Annual Berkshire Hathaway Letter

The same message continued in May of this year at Berkshire’s shareholder meeting when Buffett gave a historical perspective on the markets and investors’ attitude toward stocks after the Great Depression. While Buffett may not have been putting large amounts of cash to work in what was the quickest 35% decline and quickest recovery in history, he still delivered a reliable conclusion: “never bet against America”.

4 Buying stocks when they go on sale

This point and the last two are somewhat joined at the hip since some of the best times to buy stocks are during bear markets or when things seem the darkest. This is also when things are usually the cheapest.

In October 2008, Buffett wrote this Op-Ed piece for the New York Times, Buy American. I Am. In it, he wrote: “A simple rule dictates my buying: Be fearful when others are greedy, and be greedy when others are fearful.”

Every 5-6 years, on average, stocks fall by roughly 35%. Sometimes they fall more, sometimes less. But each time they fall, history would tell you this presents an opportunity to buy more stocks at lower valuations and future expected returns go up, not down, but often times investors let fear govern their decisions and they sell stocks after most of the damage is done.

Just remember this Buffett quote next time stocks fall 30% or more.

“Whether we're talking about socks or stocks, I like buying quality merchandise when it is marked down.”

5 Evolving investment process

Since Buffett was heavily influenced by Ben Graham, he started as a deep value investor, looking for stocks that traded near or below what a private investor might pay for them. If you could find stocks at these levels, there was likely a margin of safety embedded in the valuation.

But at some point in the late 80s or early 90s, and under the influence and advice from Charlie Munger, Buffett transitioned to a quality investor – i.e. looking to buy great businesses at attractive and fair prices. This opened up a much larger universe for Buffett, and as Berkshire grew in size, he was able to invest (or buy outright) in much larger, high quality businesses that he believed had earnings power and had a protective moat around their business and future profits.

As humans, our early experiences, successes and failures influence us greatly. For Buffett, he had success as a deep value investor and possibly some of his best performing years ever. The fact he was able to pivot and embrace high quality investing is impressive and a good lesson for all us because sometimes our success, and even survival, requires a change in how we view things.

6 Focus on Fees

Buffett is outspokenly critical of investment firms and products, including hedge funds, that charge exorbitant fees. In this interview, he makes the case calling the 2% and 20% (i.e. 2% asset management fee and 20% of profit) model obscene (see video below).

Here is the other thing: you can invest in Berkshire Hathaway for a 0% fee. So you can effectively buy a company that has a track record of effectively allocating capital, buys quality private and public stocks, flexes its cash balance and looks for buying opportunities and entry points on quality assets -- you effectively get all that for no fee. Buffett’s is not going to charge you to invest in Berkshire.

7 Respect Simplicity

Ben Carlson of Ritholtz Wealth Management summed this up perfectly in this piece, “My Too Hard Pile”. Buffett stays within his circle of competence. There are many businesses he understands and many he doesn’t. He avoided technology companies for years, but as their business models became more understandable and products more pervasive, he adjusted and invested in them and now Apple is Berkshire’s largest position.

Take a look at Berkshire’s acquisition criteria and you’ll get a sense on the value Buffett places on keeping deals simple, fair and straightforward. The criteria can be boiled down to: a large purchase, a firm with long-term earnings power, good returns on equity and little debt, and a management team in place that runs a simple business. Lastly, the seller needs to name a price so that Buffett can determine the expected return. Lots of M&A deals start without with a price that needs to be negotiated, but Berkshire requires that companies that come to their doorstep already have a buyout price in mind. This keeps deal making relatively simple and efficient.

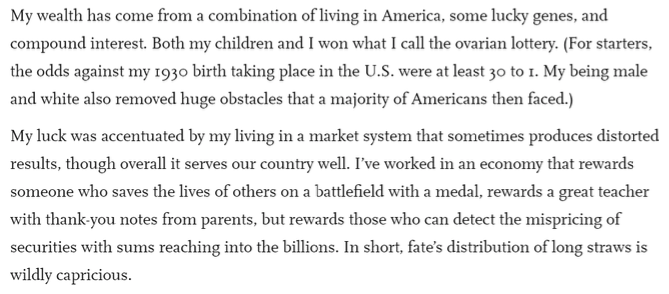

8 Give Back with Humility

Buffett has committed to donating 99% of his wealth to philanthropy through The Giving Pledge and despite being one of the world’s wealthiest individual, he maintains a relatively humble lifestyle and keeps an even humbler attitude toward his success. The excerpt below was taken from the letter he wrote when committing to The Giving Pledge.

Buffett’s long-term performance record is inimitable, and as I highlighted at the very start of the article, even though the last 10-15 years haven’t been Berkshire’s best relative to the market, that doesn’t matter because investors have “stayed with the program”, remained committed and received the return the shares have generated, which is better than many other investors. But past performance is exactly what is says it is: in the past. These eight contributions, largely influenced and persistently advocated by Mr. Buffett, can also act as a framework for many advisors as they look to help their clients meet their goals over the long-term.

© Validea

Read more commentaries by Validea