This is now the third consecutive quarterly letter in which we express a cautious stance toward both the global economy and financial markets. At this point, perhaps “cautious” is too mild a descriptor.

For the first six months of the year, commodities were the only primary asset class to offer a positive return. As of July, there was truly “no place to hide.”

In the third quarter, commodities joined US and international equities, US Treasury bonds, and gold delivering a negative return. Commodities played catch up to the downside – they were the worst performing primary asset class in the third quarter down 10.9%. The Barclays Aggregate Bond Index held up “best” down 4.7%. US equities fell 4.9% and global equities were down 7.2%.1 “Safe-haven” assets, typically go-to investments in periods of economic and financial stress, fared even worse. Long-dated US Treasury bonds and gold continued their poor performance in the third quarter. Gold was down 8.2% and Treasury bonds lost 10.3%.

This brought year-to-date totals through September 30th to: commodities +19.8%, gold -8.1%, Barclays Aggregate Bond Index -13.8%, US equities -24.4%, global equities -26.1%, and the US Treasury long-bond -28%.

Through September, a 60/40 benchmark was down 20.1% for the year. Grey Owl’s All-Season2 strategy finished the same period down 12.9%.

Economic Growth

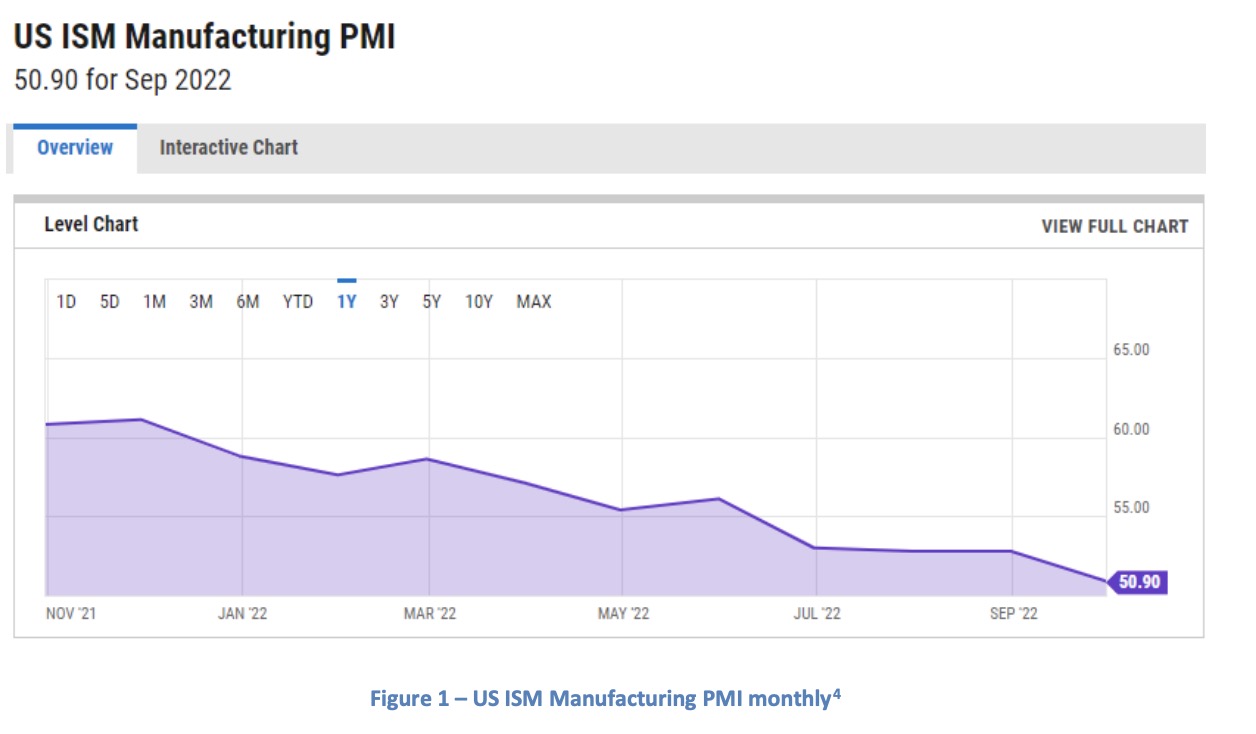

To summarize the state of the US economy, we again present the US ISM Manufacturing Purchasing Manager Index (PMI). Slowing since November of last year, the deceleration continued into September and is now teetering on a contractionary reading. The ISM PMI is a reasonably accurate leading indicator of overall economic growth. Its persistent slowdown continues to portend a decelerating US economy.

Corporate Profits

Last quarter we indicated our belief that “downward revisions in earnings are probable. Until that occurs, continued pressure on equities and other risky financial assets remains likely.”

At the end of June, consensus expectations for S&P 500 full year 2022 operating EPS was $224.54. We pointed out that this implied 12.6% annual growth from the 2019 level of $157.12 (pre-Covid) high in EPS. That expectation was almost DOUBLE the 5.7% annual earnings growth from 1999 to 2019.5 We were (and are) skeptical of that rate of growth now that the trillions of dollars of Covid-related government direct subsidies to businesses and transfer payments to individuals are gone.

Fast forward to today and downward revisions have finally begun. At this point, they are still modest. Now, the consensus expects $206.74 full-year 2022 operating earnings. While this number is down a considerable amount from the $224.54 expectation earlier in the year, it is only down a bit from the actual $208.21 in 2021.

Further, actual earnings are beginning to reflect the new lower consensus (and are likely pushing expectations even lower). As of October 28, just over half (251) of all S&P 500 companies have reported and earnings are down 3.2% compared to last year.