What Powell Said and What It Means for Markets

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsMain Points:

- Jerome Powell’s press conference after the Federal Open Market Committee (FOMC) meeting on 20 September contained many of his most interesting remarks in a long while, especially as they relate to his views on macro-economics and the US economy.

- The main message, as noted by many commentators, was that US policy rates would remain close to present levels for a prolonged period, instead of declining by 100 bps in 2024, which was what the FOMC dots implied in June. The latest median dot shows a decline of only 50 bps next year, considerably less than was priced in the markets ahead of the FOMC meeting.

- Powell was clear that this upward shift in the path for policy rates was triggered by higher GDP growth, not by more persistent inflation. He did not seem at all concerned that rising oil prices, or a temporary pothole in GDP growth in Q4, would need to be incorporated into monetary policy in the near future.

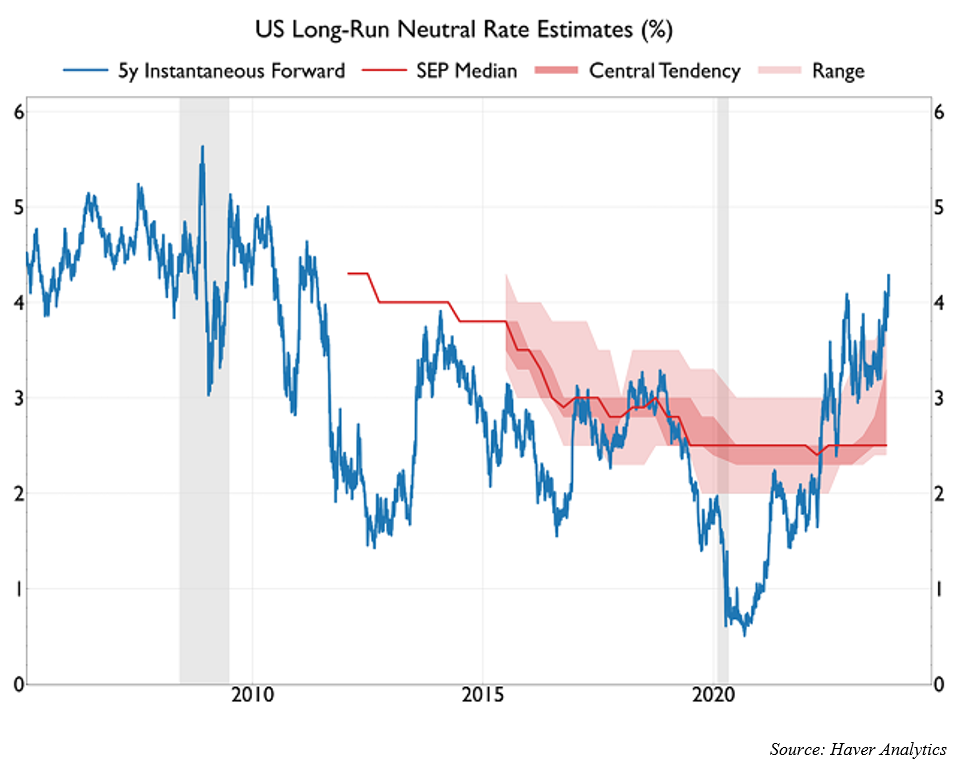

- He then stated without much equivocation that the upward revision to GDP growth forecasts has triggered a rise in his view of the equilibrium policy rate, r* (Return). This is the first time that he has clearly sanctioned this possibility.

- Powell’s remarks seem to imply that the scope for a significant rally in the bond market is limited, in the absence of a sharp shift in the economy towards recession. There will probably be a slowdown in growth soon, but this may well be seen as transitory by the Fed and therefore by markets.

- Powell also suggested that the path to a soft landing is less narrow than before, though he denied that a soft landing is now his base case. The implication of this combination of remarks for equities appears mixed, though the prospect of higher r* has understandably damaged market confidence in the near term.

Powell Sanctions Market Talk of Rising R*

Following the FOMC meeting on 20 September, market commentary has mostly concluded that Powell’s main message was “higher for longer” on Fed policy rates. We think that is indeed the right interpretation, though most of his emphasis was on the word “longer”, not “higher”.

Any remaining difference between the Fed Chair and current market pricing is mostly about the extent of the downward path for rates next year, not the level of rates at the end of this year, or indeed the peak level of rates in this cycle. Powell was unclear whether any further rate rises would be needed in the coming months, and he specifically said that one more rate hike would not be very significant.

The most important sections of Powells’ remarks were those that related to his reasoning on why policy rates would need to stay “high for longer”. He was very assertive that this was due to firmer GDP growth, not to fears of more persistent inflation. By implication, he is not worried about higher oil prices (yet). The Fed will look through higher oil prices for now.

Even more important, he was clear that firmer GDP growth may well indicate that the equilibrium policy rate, r*, has risen recently (see Graph 1 below). The key point is that this is the first time that the Fed leadership has sanctioned the idea that r* has risen this year; previously, Powell has repeatedly said that the issue is “cloudy” and has avoided taking a view.

Powell was not totally clear about why r* has gone up. He did not directly comment on fiscal policy and focused instead on the simple fact that the Fed’s GDP growth forecast for 2023 has jumped by 1% since its June forecast. This upward revision in growth is clearly a major factor in his mind.

He commented that the flows of supply and demand in the bond market may have pushed yields higher via the term premium. This is presumably driven by the budget deficit, and the Fed’s QT, though he simply labelled these factors as “bond supply”. It is not unusual for the Fed Chair to avoid commenting directly on the setting of fiscal policy, which is usually described as a matter for politicians alone to determine.

He also volunteered that the current level of r* might be higher than the policy rate that might be expected to prevail in the longer term. The dots in the latest FOMC projections show a range of 2.5-3.3% for the longer-term policy rate.

Market Implications

Since the bond market has already priced in a long run policy rate of 3.7% (ie a real rate of 1.5% plus inflation at 2.2%, based on the policy rate implied by bond prices, five years forward), it could be argued that Powell’s remarks are already reflected in the market’s expectation and indeed have been reflected for some time. However, now that the Fed has given the market the green light to contemplate a higher r* – at a level that might be higher than 2.5-3.3% in the short term – there could be bearish consequences for markets.

For bonds, higher r* means that the floor on the future trading range for bond yields has probably risen, at least in the absence of a deep recession that would mean that r* needs to be adjusted downwards again. Such a recession remains very far from Powell’s thoughts at present. (Note that he expects a “GDP pothole” in Q4 but implies that he may not pay much attention to a slowdown in growth if he thinks it is temporary – see below.)

For equities, the implications of higher r* are not entirely clear cut. An increase in r* that is driven by a rise in economic growth would seemingly trigger offsetting effects on equity values. On the one hand, the discount rate on future corporate earnings would increase, but that effect would be offset by an increase in earnings forecasts in line with a rise in nominal GDP.

Looking deeper, this arithmetic would be affected by the causes of the rise in r*. If the increase in r* is caused by supply side factors, such as the arrival of beneficial productivity effects from investment in AI, then the boost to growth would be permanent, with significant benefits for equities.

However, if the rise in r* is caused by demand-side factors, such as an increase in fiscal stimulus, then higher policy rates would be needed to achieve an unchanged outcome for real growth and inflation. In that event, the path for nominal GDP and corporate earnings would be unchanged, while the real discount rate would have risen. This would be damaging for equities.

Overall, we therefore conclude that Powell’s remarks about r* probably raise the floor and future trading range for bond yields, while having ambiguous effects on equity prices.

The Coming Dent in Q4 GDP Growth in the US

In the days after Powell’s press conference, the bear market in global bonds continued. One possible way that the bond bear market might end, or at least take a pause for breath, is a slowdown in the robust growth rates in US GDP. Several factors suggest that such a slowdown is extremely likely in the fourth quarter of 2023.

Markets now believe that a US government shutdown is likely at the end of September. Based on precedents, this will cause an almost complete blackout of economic data except for private sources, including the ADP Employment Report and some other surveys.

It will also reduce economic activity while it lasts. Our best guess is that if a government shutdown gets underway because of gridlock in Congress, it may last about 2-5 weeks, though the possible range is much wider. At the shorter end of this range the impact on Q4 GDP would be almost negligible and the Fed would ignore it. At the longer end, it could result in a moderate dent to GDP but the Fed would still see it as temporary and therefore try to look through it. At most, the FOMC might delay any final rate hike in policy rates by a few weeks.

A more serious – and unlikely – possibility is that a long shutdown would hit consumer confidence and tip the economy into a more significant slowdown. We do not expect that to happen, though it should be remembered that other factors (namely oil prices, student loan repayments and the UAW strike) may also dent the economy In Q4.

How large might the combined effects of these drags on growth prove to be? Using several different estimates published by economic research teams in the markets, we estimate the following possible impacts on quarterly annualised growth in the fourth quarter:

- A government shutdown – the growth impact might be -0.4% per two weeks of the shutdown.

- A strike by UAW impacting all three auto producers – the growth impact might be -0.3% per month of a full strike.

- The resumption of student loan repayments – the growth impact might be -0.4% this quarter.

- Higher oil prices – the $20 per barrel rise in oil prices since June might reduce annualised GDP growth in Q4 by -0.3%.

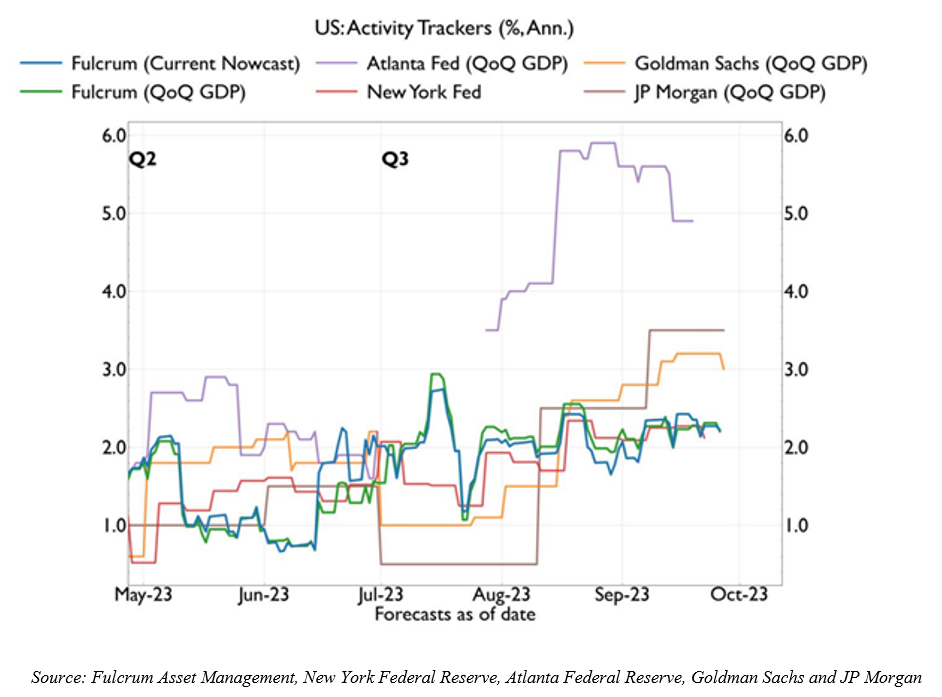

Taken together, these four shocks would therefore reduce the growth rate in Q4 by 1.4%, with a wide margin of error. Compared to the current growth rate of 2.3% (see Graph 2), this might leave the Q4 growth rate at only 0.9%.

The markets and the Fed would of course be aware that the first two effects will fully reverse and therefore boost the growth rate in 2024Q1, while the second two effects would reduce annualised growth rates only for one quarter.

Our best guess is therefore that the growth pothole will be seen as temporary and have little market impact. However, in the fog created by a data blackout – which would reduce the reliability of our nowcasts – there is possibly some risk that fears of recession might begin to take hold in the markets for a short while.

Graph 1

Graph 2

Gavyn Davies is Executive Chairman and Co-founder of Fulcrum Asset Management. Prior to Fulcrum, Gavyn was as an Economic Policy Adviser to the British Prime Minister (1976-1979) and a member of H.M.Treasury Independent Forecasting Panel (1992-1997). He was the Head of the Global Economics Department at Goldman Sachs from 1987-2001 and Chairman of the BBC from 2001-2004. Gavyn graduated in Economics from Cambridge followed by two years of research at Oxford and he is also a visiting fellow at Balliol College, Oxford.

This content is provided for informational purposes and is directed at professional clients as defined in Directive 2011/61/EU (AIFMD) and Directive 2014/65/EU (MiFID II) Annex II Section I or Section II or an investor with an equivalent status as defined by your local jurisdiction. Fulcrum Asset Management LLP (“Fulcrum”) does not produce independent Investment Research and any content disseminated is not prepared in accordance with legal requirements designed to promote the independence of investment research and as such should be deemed as marketing communications. This document is also considered to be a minor non-monetary (‘MNMB’) benefit under Directive 2014/65/EU on Markets in Financial Instruments Directive (‘MiFID II’) which transposed into UK domestic law under the Financial Services and Markets Act 2000 (as amended). Fulcrum defines MNMBs as documentation relating to a financial instrument or an investment service which is generic in nature and may be simultaneously made available to any investment firm wishing to receive it or to the general public. The following information may have been disseminated in conferences, seminars and other training events on the benefits and features of a specific financial instrument or an investment service provided by Fulcrum.Any views and opinions expressed are for informational and/or similarly educational purposes only and are a reflection of the author’s best judgment, based upon information available at the time obtained from sources believed to be reliable and providing information in good faith, but no responsibility is accepted for any errors or omissions. Charts and graphs provided herein are for illustrative purposes only. The information contained herein is only as current as of the date indicated, and may be superseded by subsequent market events or for other reasons. Some of the statements may be forward-looking statements or statements of future expectations based on the currently available information. Accordingly, such statements are subject to risks and uncertainties. For example, factors such as the development of macroeconomic conditions, future market conditions, unusual catastrophic loss events, changes in the capital markets and other circumstances may cause the actual events or results to be materially different from those anticipated by such statements. In no case whatsoever will Fulcrum be liable to anyone for any decision made or action taken in conjunction with the information and/or statements in this press release or for any related damages. Reproduction of this material in whole or in part is strictly prohibited without prior written permission of Fulcrum Copyright © Fulcrum Asset Management LLP 2023. All rights reserved.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All