Key Forecast Trends

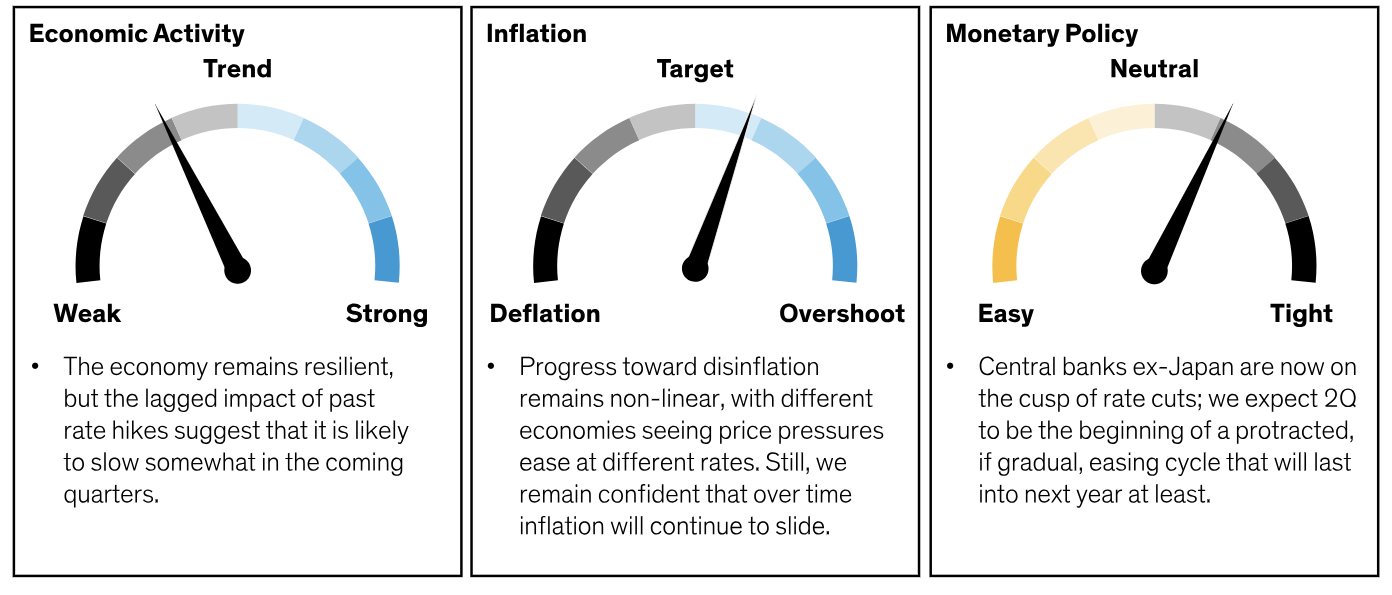

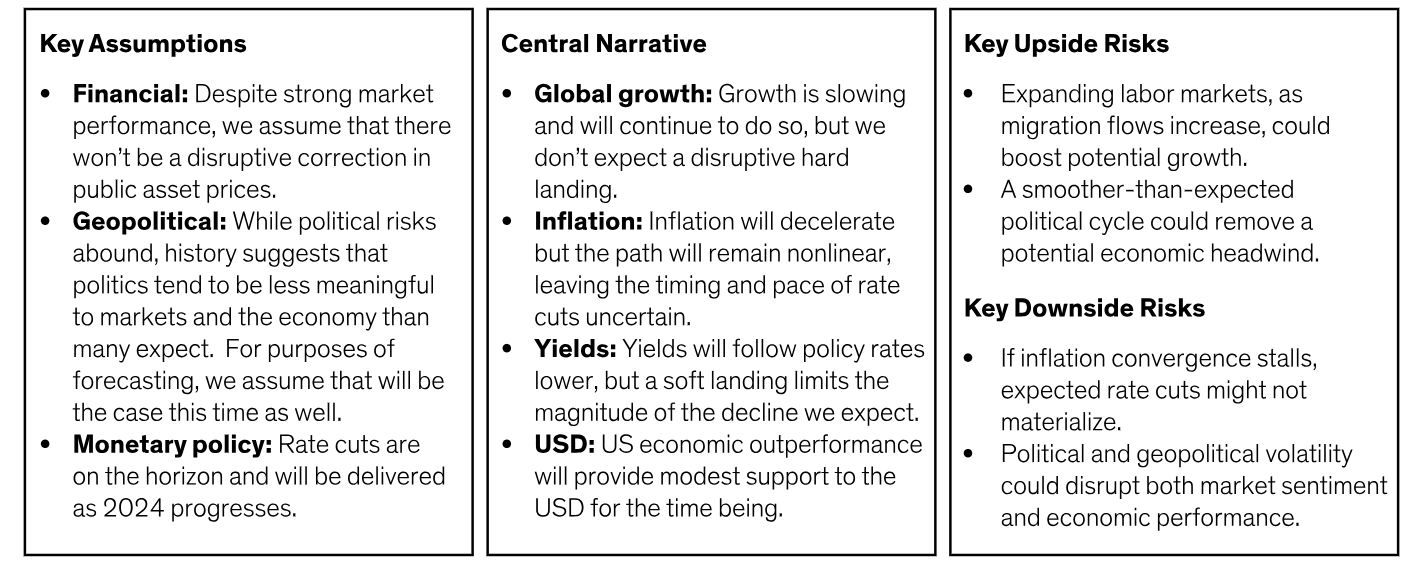

- The global economic picture didn’t change much since last quarter, and we continue to see a soft landing as the most likely outcome.

- With growth relatively strong, the road back to the Fed’s 2% inflation target has been bumpy, which could continue.

- We still feel that most major central banks will start to ease this year, they just may not begin at the same time.

- On the other hand, the Bank of Japan is completing efforts to ramp inflation back up, and last quarter began to dismantle its yield curve control framework.

- China’s low inflation is a more proximate threat; although we don’t expect a crisis there, we don’t see meaningful pickups in growth or market sentiment either.

- Volatility from political risk tends to have slight economic or financial market impact. This time could be different, of course, so we’ll be monitoring global elections closely.