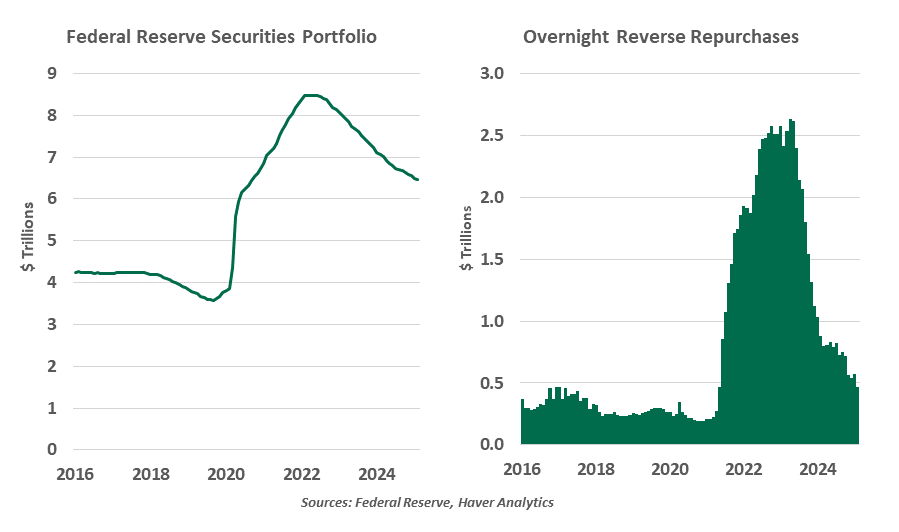

From its peak of nearly $9 trillion three years ago, the Fed’s holdings of Treasuries and mortgage-backed securities have declined by over $2 trillion. The magnitude of quantitative tightening (QT) is startling, but so is the lack of market reaction to such a change.

The Fed’s interventions in bond markets are most impactful when making purchases. In moments of stress, the Fed uses asset purchases to add liquidity to the financial system, which can boost aggregate demand. But after their initial deployment, the funds have less of a stimulative effect. Winding down the balance sheet is a marginal step toward tighter monetary conditions, but tends not to cause decisive market shifts.

The Fed’s balance sheet is nearing its steady state.

QT has taken the form of Treasury instruments coming to term. When a security held by the Fed expires, Treasury repays the face value to the Fed. The Fed does not reinvest the proceeds, and the value is written down. No currency is taken out of active circulation.

Liquidity is less ample today. Overnight reverse repurchase volumes—typically money market fund assets not held in Treasuries—have fallen by over 80% and are nearly back to their pre-pandemic level. The return of the debt ceiling is forcing the Treasury to spend down its general account, a boost to liquidity that will be temporary. While the exact point to end the drawdown is difficult to calibrate, these circumstances make it an appropriate time for the Fed to change tack.

At this week’s meeting of the Federal Open Market Committee, reinvestment of Treasury holdings was reduced from a monthly cap of $25 billion to $5 billion, significantly slowing the rate of the balance sheet decline. This adjustment should help to avoid shocks to the interbank lending market, like was seen in the last tightening cycle in 2019. The Fed’s decisions around rate actions will be front and center in the year ahead; the management of its balance sheet should remain uneventful.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust