Ripley's is an American franchise that features strange events, unusual objects, and unbelievable stories. It’s tagline is “Believe it or not.” The U.S. administration has also initiated some unusual actions that defy belief, and which could permanently alter the international trade landscape.

The first few months of 2025 promised to be bumpy, but not many expected the world to be on the brink of a full-blown trade war. More tariff announcements are in sight. Whatever shape they take, they will be a significant expansion of trade restrictions.

We expect average duties on goods arriving in the United States from most parts of the world to reach 10%, with Chinese imports subject to significantly higher rates. This substantial shift (from an average rate of just over 2% in 2024) will put a significant dent in economic growth in many places. Central banks will have to navigate carefully, as tariffs tend raise inflation and slow growth.

Following are our thoughts on how top areas are faring.

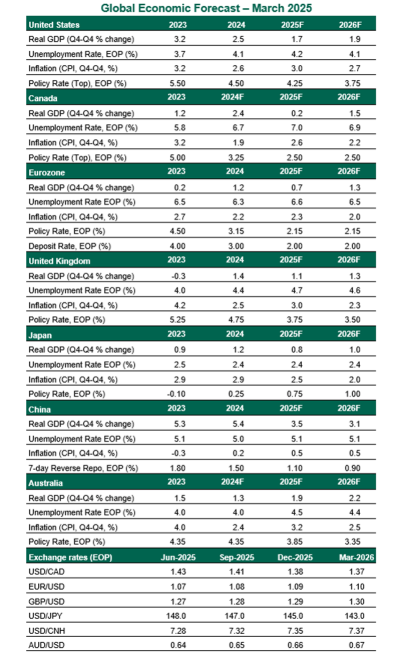

United States

- High uncertainty is cooling both business investment and consumer confidence. A downshift from above-potential to slower growth is our base case. Our forecast assumes actual average tariffs do not reach their maximum threatened level and that many of them will eventually be rescinded (at least partially). But the higher the levies go and the longer they remain in place, the stronger the probability of a downturn.

- At its March meeting, the Federal Open Market Committee held rates steady. Their decision came with cautious guidance of slower growth and higher inflation through 2026. Chair Powell acknowledged uncertainty across several policy domains (trade, immigration, fiscal policy and regulation), supporting a patient stance. Sticky inflation and a resilient labor market will keep the Federal Reserve sidelined for the time being. We anticipate one cut later this year, followed by two more in 2026.

Australia

- The Australian economy ended 2024 on a relatively favorable footing. The recovery is being underpinned by a strong labor market, moderating inflation, tax cuts and cost-of-living rebates. The federal budget extended support measures ahead of the upcoming election. Given its small direct trade exposure to the U.S., reciprocal tariffs will likely have a limited impact on the Australian economy. In our view, the second-order effects of a weaker Chinese economy will prove to be more worrisome for Australian exporters.

- The labor market in Australia remains tight, with forward-looking indicators showing no signs of easing. With domestic demand improving and productivity still weak, we continue to expect the Reserve Bank of Australia (RBA) to tread cautiously. The RBA is likely to deliver only one more cut towards the end of the year.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2025 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust