This commentary was originally posted on April 8th.

With the latest round of US tariff measures announced in early April, we’ve downgraded our US economic outlook. We expect slower growth and higher inflation for 2025. If this plays out, we think the Fed will cut policy rates by 75 basis points in 2025, possibly more.

The back and forth over specific tariff measures remains very fluid, as recent headlines can attest, and if the policies announced April 2 don’t stay in place, the situation could change considerably. But if they do stay in effect, the impact could be dramatic. We think those policies, combined with cuts in domestic spending and government jobs, would reduce growth in 2025 US GDP to a range of 0% to 0.5%, with a significant chance of recession.

Tariff Impact Flows Through to US Price Levels

The April tariffs have boosted the effective tariff rate by roughly 25% from last year, which we expect will push prices for US consumers and businesses higher. Slower growth and declining commodity prices may blunt some of the impact, but we’ve raised our inflation forecast for this year to 4% for the core Consumer Price Index. That’s about 1.5% higher than core inflation would have been without tariffs.

Those higher prices equate to a roughly $4,000 cost for the average US family, which is almost 10% of post-tax median income. It’s true that price increases in the wake of the COVID-19 pandemic were even bigger, but aid from the federal government helped US households to weather that earlier period. Such payments seem highly unlikely this time around.

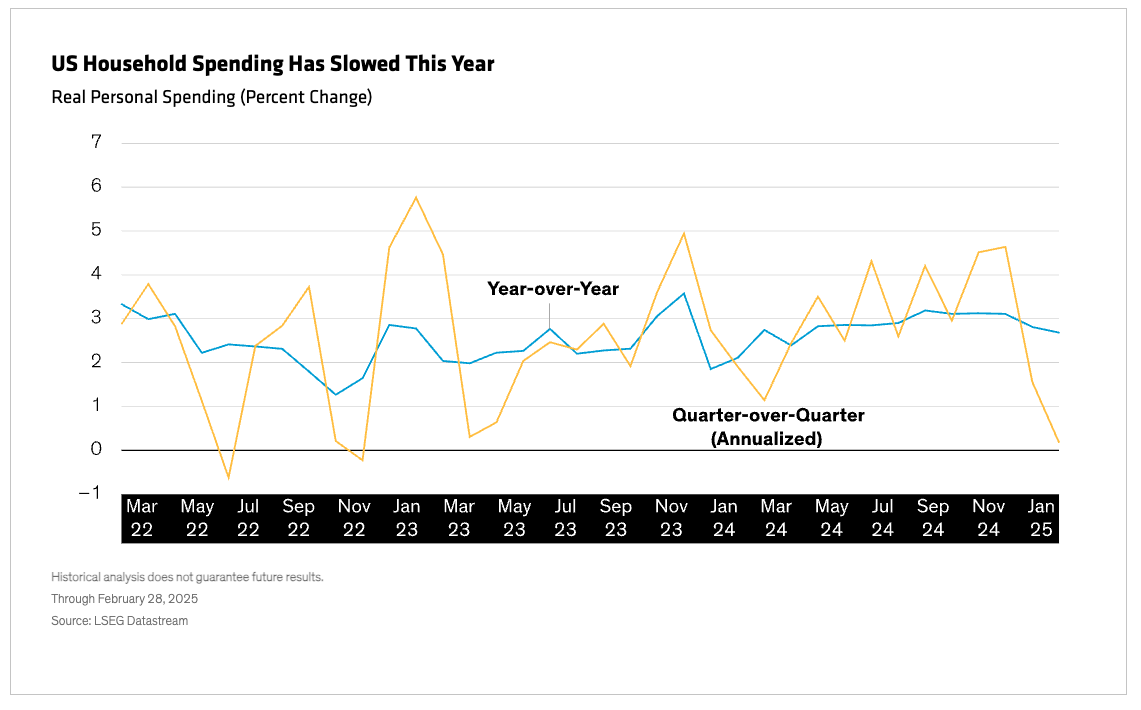

The expected slowdown isn’t a directional change from our prior forecasts. Household spending has already slowed this year (Display) and falling measures of consumer confidence suggest more to come—even before last week’s tariff announcements. Of course, confidence can be volatile, and other factors can influence spending. But we think the impending tariffs on top of existing economic data skew risks clearly to the downside going forward.

Strong Starting Point Likely Means Economic Slowdown, Not Collapse

At this point, we expect a slowdown, but it’s important to remember that the starting point for the US economy is strong. The labor market is robust and stable, providing households with a steady source of income. Households don’t have the excess-savings cushion that they had post-pandemic, but labor income has outpaced inflation this cycle—if that holds, the US economy won’t collapse.

The March payrolls report also illustrates the job market’s resilience. The headline gain of 228,000 jobs keeps the longer-term average hiring rate steady at around 150,000 per month. With migration flows having dried up last year and remaining subdued this year, that’s more than enough to absorb new entrants to the labor force and keep the unemployment rate steady at around 4%. That’s up from the post-pandemic overheating but still very low historically.

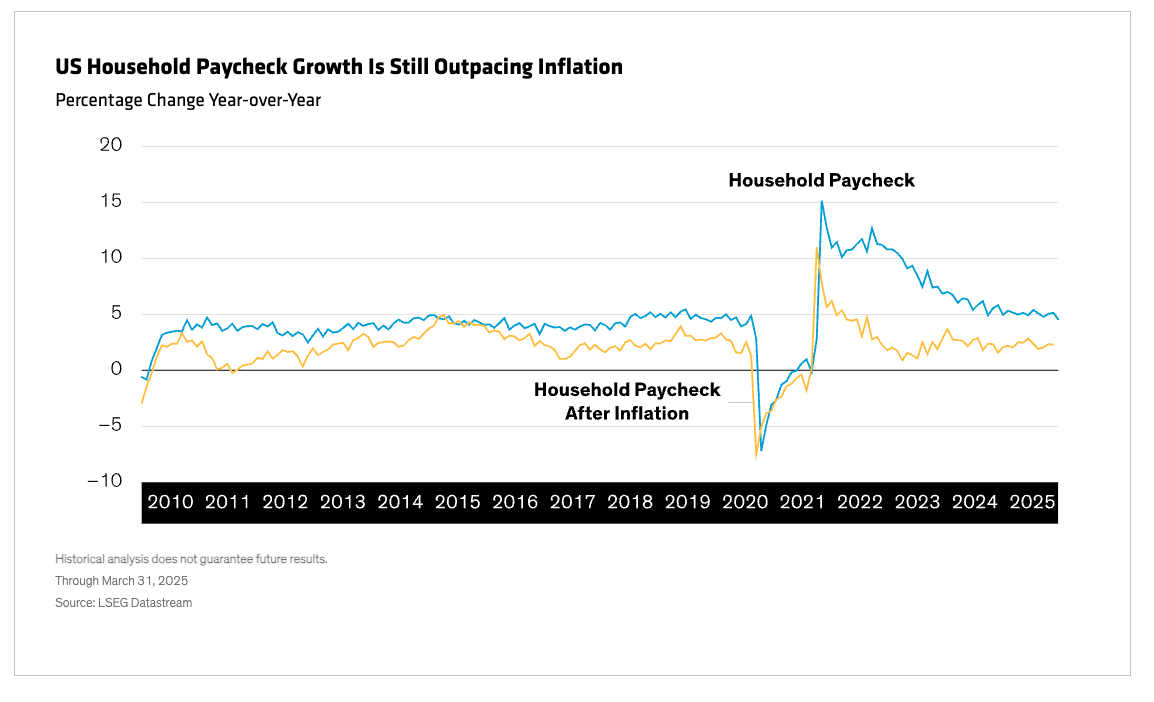

The administration’s efforts to reduce government employment appear to be bearing fruit; federal employment has fallen for three consecutive months. Beyond that, the basic patterns of the labor market remain in place, with healthcare the strongest sector. The combination of solid hiring and decent wage growth is keeping the growth rate of the household paycheck in positive territory after accounting for inflation (Display).

Multiple 2025 Rate Cuts Likely on Tap…if Inflation Behaves

For now, we expect the Fed to wait for data to guide its decisions. If the economy slows, as we expect it will, the Fed will be inclined to cut rates even if price levels are high. The view is that actual inflation tells us what the economy was doing but not what it will do. The Fed has cut rates before with inflation elevated, and we expect it to do so again unless—a very big “unless”—inflation expectations become unanchored.

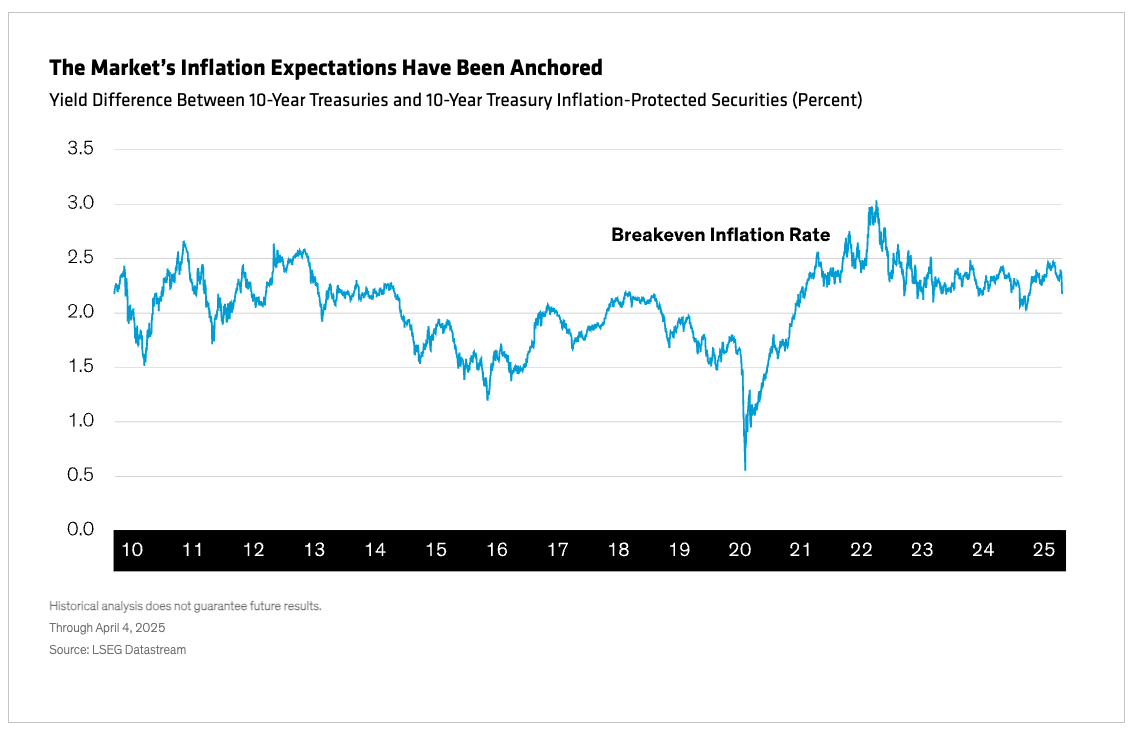

A rise in inflation expectations—not the actual inflation rate itself—was the defining feature of the 1970s inflation shock, making the initial shock persist. The Fed has learned from that experience, and Chair Jay Powell’s recent comments make clear that inflation expectations are the key variable to monitor right now. The vast majority of indicators, including market-based (Display), still point to inflation expectations staying anchored. The University of Michigan survey is the notable exception.

If expectations remain well anchored, the Fed will be able to cut rates and support the economy. We expect 75 basis points in rate cuts over the rest of 2025 starting in the summer. We see greater risk that rate cuts top that level than fall short of it. The policy rate at the end of this cycle will likely be below 3%, a level intended to stimulate economic growth.

Markets will continue to wrestle with the implications of an expanding trade war. As headlines suggest, other countries may not give in but retaliate, escalating the conflict, and there’s ample room for the US to do the same. While it’s possible that some of the announced tariffs won’t “stick,” we think most of them likely will, and we haven’t yet seen the impact flow through to the economic data. That means this story is far from over.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein