April 2025 Monthly Market Commentary

-

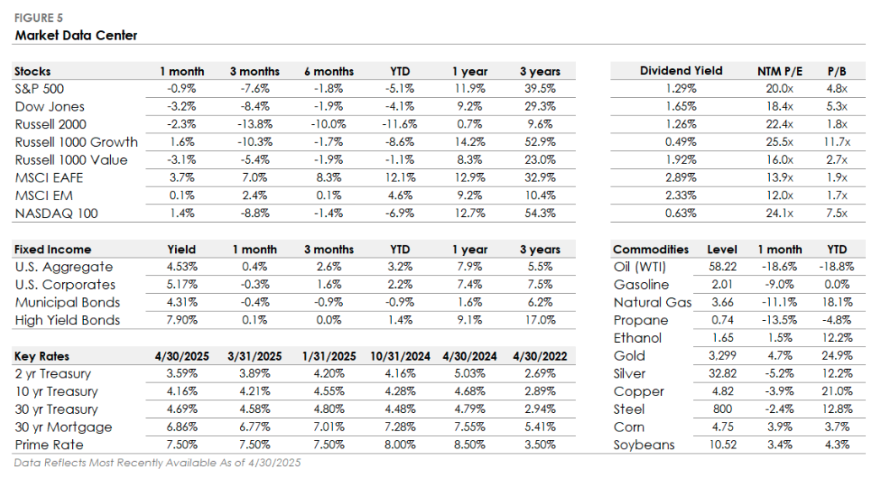

US Stocks: The S&P 500 finished April slightly lower, declining 0.9%, but a significant improvement from its early month decline of over 10% following aggressive tariff announcements from Washington. Technology emerged as the leading sector, followed closely by Consumer Staples, Industrials, and Utilities. Conversely, Energy fell sharply by 13.9%, driven by an 18.6% collapse in oil prices.

-

International Stocks: International equities outperformed US markets, with Developed Markets gaining 3.7% and Emerging Markets squeezing out a 0.1% gain.

-

Bonds: Bond markets navigated similar volatility but ultimately finished nearly flat. The US Aggregate Bond Index finished April with a 0.4% positive return, although underlying bond performance was mixed. High-yield bonds were slightly positive (+0.1%) while investment grade bonds fell modestly (-0.3%).

Markets Rebound from an Early-April Selloff as Trade Tensions Ease

Stocks declined in early April after the White House unveiled sweeping tariffs, with the S&P 500 falling over -10% in the first week. However, after the administration paused tariffs and trade tensions eased, the S&P 500 rebounded to finish the month with a loss of less than -1%. Interest rates were volatile in April as the market navigated tariff headlines and economic uncertainty but ultimately ended the month unchanged, with Treasury and corporate bonds flat.

Outside the stock and bond markets, gold surged to a record high amid increased market volatility. Elsewhere, the U.S. dollar weakened due to concerns about the direction of U.S. policymaking. These developments echo our commentary earlier this year on the significant influence of Washington’s decisions on global financial markets.

An Update on This Year’s Key Market & Economic Trends

The late-month sell-off was not driven by a single event but rather a confluence of factors that underscored a cooling economic backdrop. Economic data underperformed expectations, with the services sector contracting and consumer confidence weakening. The decline in consumer demand, a key pillar of recent economic strength, signaled potential headwinds ahead. At the same time, renewed policy uncertainty emerged in Washington, including tariff threats and proposed spending cuts, fueling concerns that restrictive fiscal policies could further dampen growth. Tech stocks faced additional pressure after Nvidia’s much-anticipated earnings report failed to sustain enthusiasm for AI-related investments, triggering broader weakness across the sector.

Investor Sentiment Turns Cautious Amid Policy and Growth Concerns

The persistent theme for 2025 has been “policy uncertainty.” The latest introduction of tariffs has increased caution among businesses and consumers, although what Trump’s final tariff policy will look like remains unknown. This uncertainty is impacting financial markets, which are now focused on how tariffs may affect future economic growth and corporate earnings. Recent economic data indicates that tariffs pulled forward some consumer demand, but forward-looking surveys suggest growth could slow as policy uncertainty delays spending and investment decisions.

Additional thoughts below.

-

Shift in Equity Leadership: The “Magnificent 7” mega-cap tech stocks have reversed last year’s strong performance and are down over 15% YTD (vs. over +60% in 2024). In contrast, traditionally defensive sectors such as Utilities, Consumer Staples, Health Care, and Real Estate are outperforming, as investors gravitate toward more stable parts of the market.

-

International Markets are (Finally?) Shining: 1Q25 marked the first time since late-2023 that international markets outperformed US equities, delivering one of their best relative performances since 2000. Given the Trump administration’s policy stance Europe and other developed nations are for the first time looking to significantly reinvest in their own economies and infrastructure. These tailwinds are boosting investor appetite for geographical diversification.

-

Bond Markets Showing Volatility: Treasuries experienced heightened volatility, driven by tariff developments, debt concerns, and mixed signals on inflation and growth. Credit spreads have widened, and high-yield bonds are under pressure as markets reprice downside risks.

-

Federal Reserve Watch: The Fed’s anticipated easing remains on hold, balancing inflation concerns with potential growth moderation from tariffs. Markets still expect four rate cuts this year, starting in June, signaling rising expectations for economic cooling.

Our Perspective

We continue to advocate for disciplined portfolio management amidst ongoing volatility. As we’ve consistently emphasized, market swings tied to policy shifts are not unusual. Volatility, while uncomfortable, creates opportunities. Investors should remain focused on long-term objectives, avoiding reactionary moves driven by short-term headlines. That said, given policy changes we view enhancing exposure to international economies and defensive sectors as a potentially strategic opportunity to enhance diversification.

Please read important disclosures here.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Defiant Capital Group

Read more commentaries by Defiant Capital Group