Most investors would jump at the chance to add more money to their portfolio, but they often fail to consider the hidden costs associated with it. These costs may not be explicit, as in the form of fees or expenses, but they can implicitly manifest as an increased level of risk.

This misunderstanding has sparked extensive discussion over the past few years as more investors focus on the surging U.S. equity market, particularly U.S. growth equities, and wonder if they have somehow “missed out” by sticking with a globally diversified portfolio.

A more concentrated portfolio of U.S. equities may make sense for some direct contribution (DC) plan participants, but for the vast majority, staying the course with a diversified approach is the right decision. While this may seem like common sense, a recent Columbia University study examined 3 million investors enrolled in 296 401(k) plans and found that most individuals are underexposed to international securities. These U.S.-concentrated portfolios have performed well of late, but they subject investors to portfolio characteristics that may not align with their objectives.

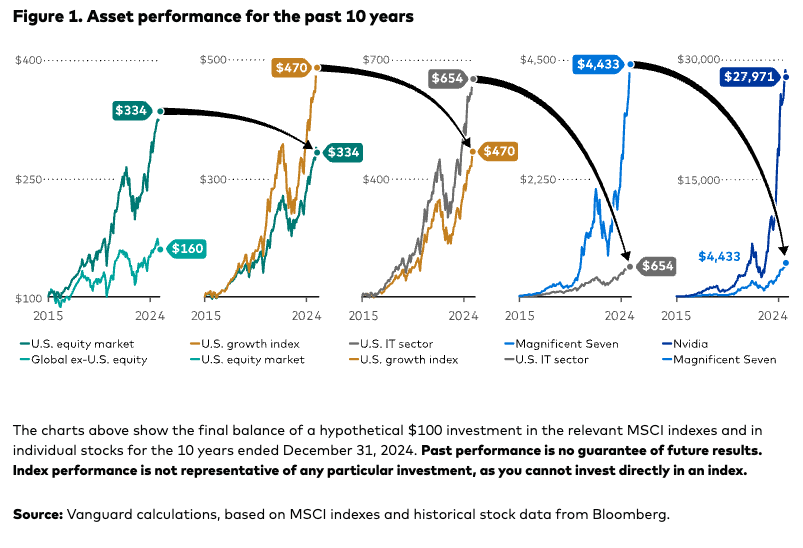

Still, it is worth noting that the past 10 years have not been as favorable to globally diversified portfolios compared with previous decades. In a recent article, Roger Aliaga-Díaz, Vanguard’s global head of portfolio construction and portfolio manager of the Target Retirement Fund series, discusses the disadvantage of chasing outperformance at the expense of portfolio diversification. As illustrated in Figure 1, Aliaga-Díaz explains how “a $100 investment in U.S. stocks 10 years ago would have grown to $334 by the end of 2024 (an annualized 13% return)—more than twice the final balance of $160 (an annualized 5% return) for a similar investment in non-U.S. stocks.”1 It is understandable that some equity investors are feeling like they are missing out.

But based on this logic, asks Aliaga-Díaz, why stop with global diversification? “The same argument could apply to all levels of portfolio diversification,” he says. “Looking at market results over the 10 years ended December 31, 2024, why bother with broadly diversified U.S. equity exposure when U.S. growth stocks outperformed the broad U.S. market by 1.4 times ($470 versus $334)? Why invest in value stocks at all?”

Finally, Aliaga-Díaz applies the fallacy of this argument to the information technology (IT) sector, which outperformed growth stocks by 1.4 times: “Why not just concentrate the entire equity portfolio in that sector? And why not further weed out the underperforming parts of the sector? The Magnificent Seven outperformed the IT sector by 6.8 times.2 One stock, Nvidia, outperformed the collective return of the Magnificent Seven by 6.3 times” (as shown in Figure 1).

While we are fairly certain that no plan sponsor has chosen a qualified default investment alternative entirely invested in Nvidia, many participants are now debating whether a portfolio with a heavier allocation to U.S. stocks or U.S. growth equity would improve investor outcomes. Although simulations might suggest that this approach could lead to a higher overall portfolio value, they overlook the crucial aspects of utility, which is the level of satisfaction associated with all possible outcomes that can take place when investing, and risk management. It is essential to recognize that an additional dollar means different things to different investors; what benefits one participant may not benefit another.

Global diversification in target-date funds

We design our target-date funds (TDFs) with the long-term retirement goals of participants in mind. This approach has remained consistent for more than 20 years since the inception of Vanguard Target Retirement Funds. To ensure that these funds meet their objectives, we annually revalidate our assumptions, inclusive of asset class projections and investor characteristics, to ensure that the allocation remains suitable to meet investor needs.

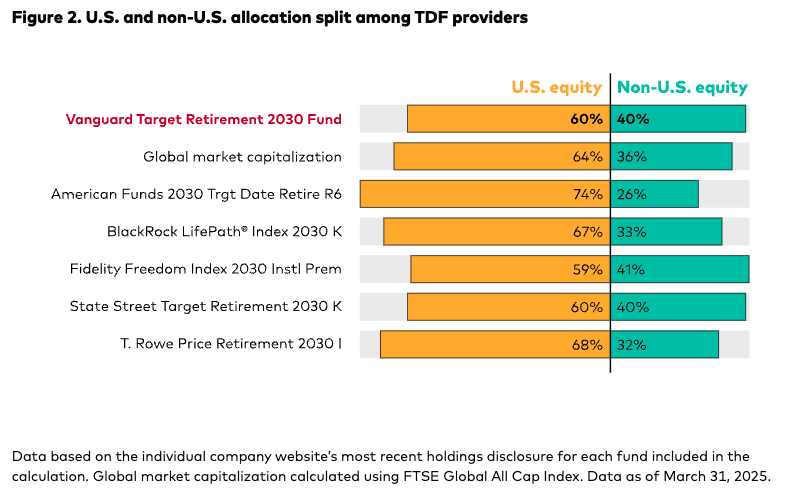

While the performance of the allocation to international equities has trailed that of the allocation to U.S. equities as of late, investors have still seen returns that allow them to maintain a high probability of achieving their retirement goals. Additionally, as Figure 2 shows, the international equity exposure within our Target Retirement Funds, while material, remains relatively in line with both the global equity market capitalization, which is a general guide for this series, and other competitors’ allocations to these securities.

Given the potential for a multidecade investment timeline and that the primary purpose of a TDF is to help investors prepare for retirement, we prioritize a strategic asset allocation that can deliver consistent and reliable results. This approach has been beneficial across multiple market cycles and remains a key investment principle behind Vanguard Target Retirement Funds.

The case for international equities still holds

This is not to say that there is no merit in choosing a TDF with less global diversification. Certain plan demographics, such as salary or retirement age, can make a case for different approaches. With that said, Vanguard looks to make changes that positively impact the needs of all investors. As the world’s largest provider of TDFs, we believe in making decisions that can serve the broadest swath of participants, generally leading us away from shifts in the allocation that result in a less diversified portfolio.

Long-term investors, like those invested in TDFs, need products built for multiple market cycles. For Vanguard, this means ensuring we provide a well-diversified portfolio with an asset allocation that is rigorously reviewed on a continuous basis. This approach has served investors well for more than 20 years, and we maintain our conviction in its ability to do so in the future.

This article was previously published on vanguard.com

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Sources:

1 Returns in all the scenarios are based on our calculations using the relevant MSCI indexes through the 10 years ended December 31, 2024.

2 The Magnificent Seven are the seven stocks that have driven much of the market’s returns over the past few years: Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla.

Notes:

For more information about Vanguard funds, visit vanguard.com to obtain a prospectus or, if available, a summary prospectus. Investment objectives, risks, charges, expenses, and other important information are contained in the prospectus; read and consider it carefully before investing.

- Investments in Target Retirement Funds are subject to the risks of their underlying funds. The year in the fund name refers to the approximate year (the target date) when an investor in the fund would retire and leave the workforce. The fund will gradually shift its emphasis from more aggressive investments to more conservative ones based on its target date. An investment in a Target Retirement Fund is not guaranteed at any time, including on or after the target date.

- All investing is subject to risk, including the possible loss of the money you invest. There is no guarantee that any particular asset allocation or mix of funds will meet your investment objectives or provide you with a given level of income. Diversification does not ensure a profit or protect against a loss.

- Investments in stocks or bonds issued by non-U.S. companies are subject to risks including country/regional risk and currency risk.

- Funds that concentrate on a relatively narrow market sector face the risk of higher share-price volatility.

Vanguard funds not held in a brokerage account are held by The Vanguard Group, Inc., and are not protected by SIPC. Brokerage assets are held by Vanguard Brokerage Services, a division of Vanguard Marketing Corporation, member FINRA and SIPC.

For additional financial information on Vanguard Marketing Corporation, see its Statement of Financial Condition: Audited and Unaudited

Broker-Dealer Form Client Relationship Summary (Form CRS) and Investment Advisor Form Client Relationship Summary (Form CRS)

© 1995–2025 The Vanguard Group, Inc. All rights reserved. Vanguard Marketing Corporation, Distributor of the Vanguard Funds. Your use of this site signifies that you accept our terms & conditions of use.

© Vanguard

Read more commentaries by Vanguard