The bull market is alive and well, even amid widespread talk of the “death of U.S. exceptionalism.” Early 2025 saw a sharp shift in investor sentiment. Concerns over erratic trade policy, soaring debt, and weakening dollar pressure challenged America’s long-standing market dominance. Markets fell sharply in April and May, feeding a narrative of declining “US exceptionalism” as the leading technology stocks (known as the “Magnificent 7”) significantly underperformed the broader index.

The April sell-off began with President Trump’s sweeping “Liberation Day” tariff package on April 2. With nearly all sectors hit by tariffs, stocks plunged almost 20% from record highs, officially entering correction territory. To rationalize that decline, the media narratives ran wild after the preceding two years of 20% gains, with the most bearish headlines available. Reports from PineBridge, Standard Chartered, and iA Global Asset Management suggested the end of U.S. exceptionalism as global fund flows shifted. Even Societe Generale’s Alain Bokobza warned that fading confidence could drive a prolonged rotation out of U.S. stocks.

That rotation of fund flows came from the decline in the U.S. Dollar Index, which dragged on U.S. returns for international investors. This makes sense as foreign investor returns get hit twice when domestic share prices fall simultaneously with a weaker dollar. That is why there is a negative correlation between those two asset classes. However, it should be noted that the decline in the dollar this year follows a sharp rally last year, and the bull market in the dollar remains.

Nonetheless, capital flows were reallocated globally, allowing European equities to outperform U.S. markets this year. However, is this the end of “US exceptionalism?”

A Different Picture Emerges

Despite fears of declining US exceptionalism, debts and deficits, a falling dollar, and tariffs, equities rallied from the April lows with unexpected strength. Leading that charge were the very stocks the bearish media proclaimed dead.

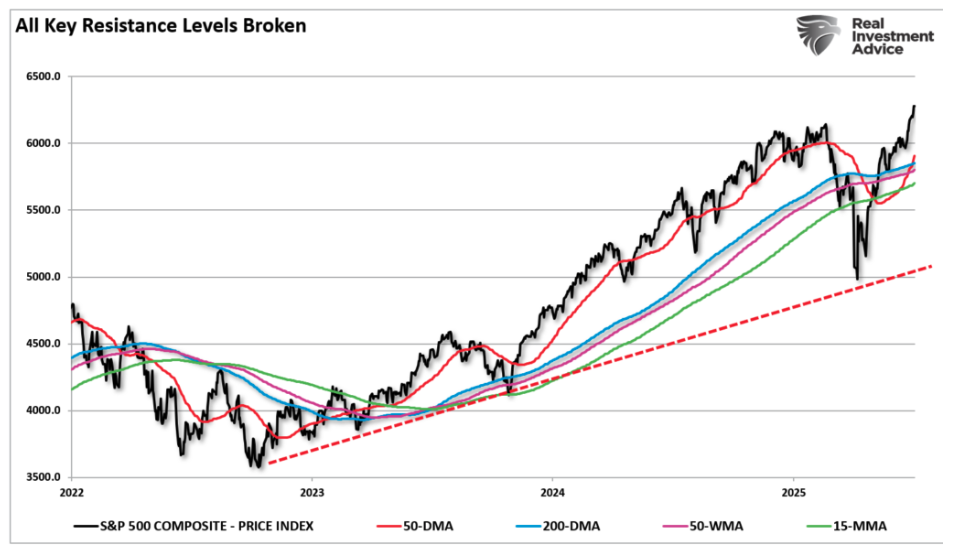

Equity markets’ technical posture painted a different picture against that pessimistic canvas. By mid-April, after several days of heavy losses, markets rebounded sharply. A 90-day tariff truce announced on April 9 triggered a 9.5% one-day rally in the S&P 500, the largest since 2008. Despite still‑high inflation and 4.5% bond yields, markets held key support at the 200‑day moving average, suggesting the correction phase had ended.

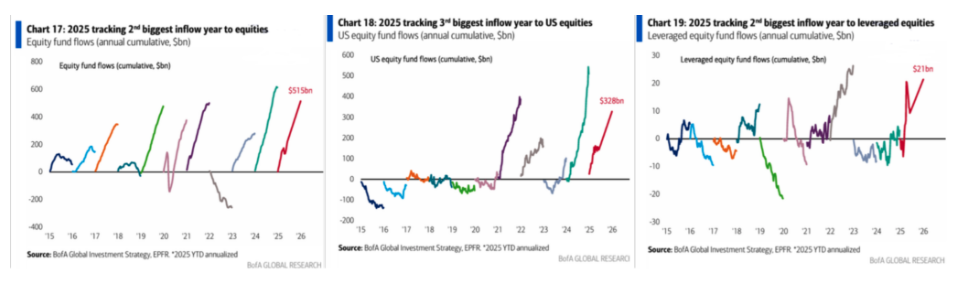

Most notably, the “dual equity pain trade” further supports the rally. Many institutional investors trimmed U.S. exposure in April, creating underweights that fuel contrarian inflows, particularly back into quality U.S. assets. JPMorgan notes the path of least resistance favors new highs, and fundamentals reinforce that view. As the most recent #BullBearReport pointed out, retail investors piled into US equities ($515 billion) and another $21 billion into “leveraged” equities.

The rebound isn’t surprising, as we noted on April 7th. That pullback “washed out” investor euphoria, paving the way for any “good news” to facilitate gains. To wit:

That dip served as a healthy reset. Investor sentiment swung from euphoria to skepticism, which is required to continue the bull market.

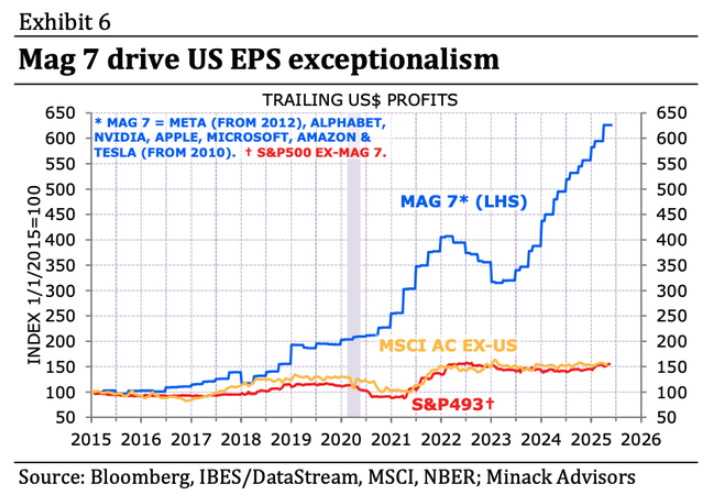

Fundamentals also underpin this market’s resilience. Employment added 147,000 jobs in June, while in a weakening trend, it is still growing. However, corporate earnings grew steadily across sectors, and the tech-heavy “Magnificent 7” continues to deliver strong results, driving much of the rebound. Despite headlines suggesting Europe is the place for growth, the “Mag 7” stocks drive corporate earnings versus the rest of the index and the world. (h/t @eggswhite)

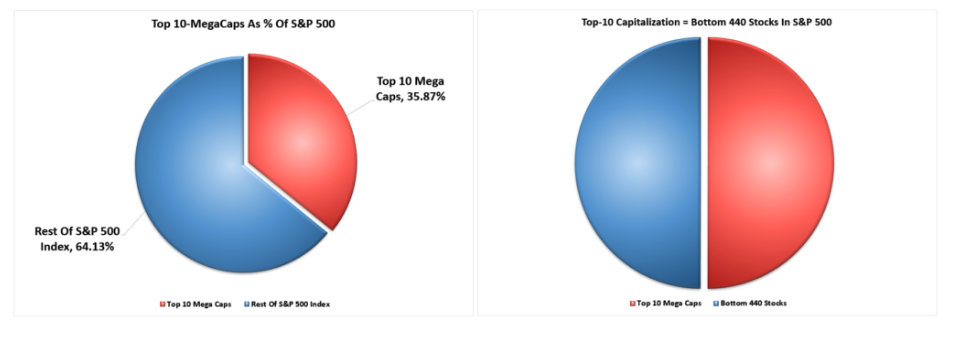

Furthermore, those seven stocks have contributed over $2.4 trillion to market gains since May. This is due to the hefty weighting in the S&P 500 index, which absorbs $0.36 of every dollar invested. Furthermore, the top 10 stocks impact the S&P 500 index the same as the bottom 440 stocks combined.

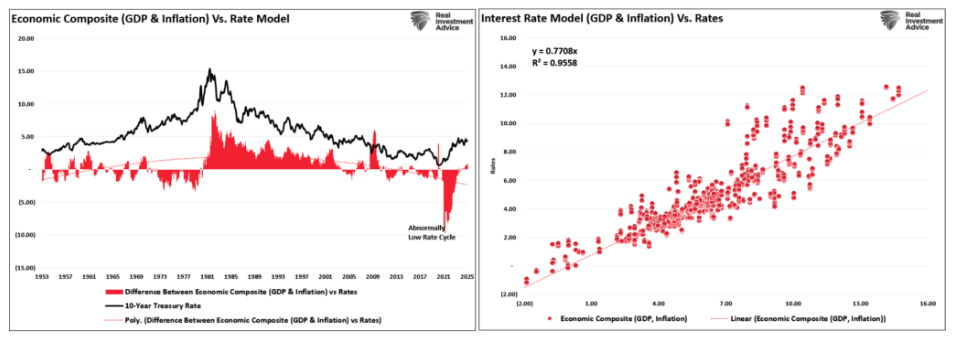

Economically, inflation is easing. Core measures hover near 2.3%, and bond yields stabilized. Long-term Treasury yields around 4.5% reflect a market no longer panicking as yields have normalized to current economic and inflation growth rates. (The left chart shows the difference between current rates and the economic growth and inflation interest rate model.)

The “dual equity pain trade” further supports the rally. Many institutional investors trimmed U.S. exposure in April, creating underweights that fuel contrarian inflows, particularly back into quality U.S. assets. JPMorgan notes the path of least resistance favors new highs, and fundamentals reinforce that view.

Global dynamics also play a role. Even amid U.S. outflows, international capital repositioned in Europe and emerging Asia is a rotation, not a complete exit. At the same time, robust inflows into U.S. tech, AI, and large-cap growth show that America’s competitive strength remains intact. Most importantly, the dollar’s recent weakness supports U.S. exports and earnings for multinationals, offsetting earlier fears.

Technically Speaking, The Bull Market Is Intact

Multiple factors have converged to support the recent rally despite the narrative of U.S. decline.

- The April drawdown reset valuations, reducing euphoria and creating technical support.

- U.S. economic indicators—jobs, corporate earnings, inflation—remain strong.

- Institutional repositioning has triggered rebound buying in quality names.

- Global flows rotate but do not abandon U.S. markets entirely.

- The Federal Reserve maintains a cautious stance, supporting market confidence.

In other words, as we discussed in “Narratives Change, Markets Don’t,“ short-term market declines generate headlines to rationalize events.

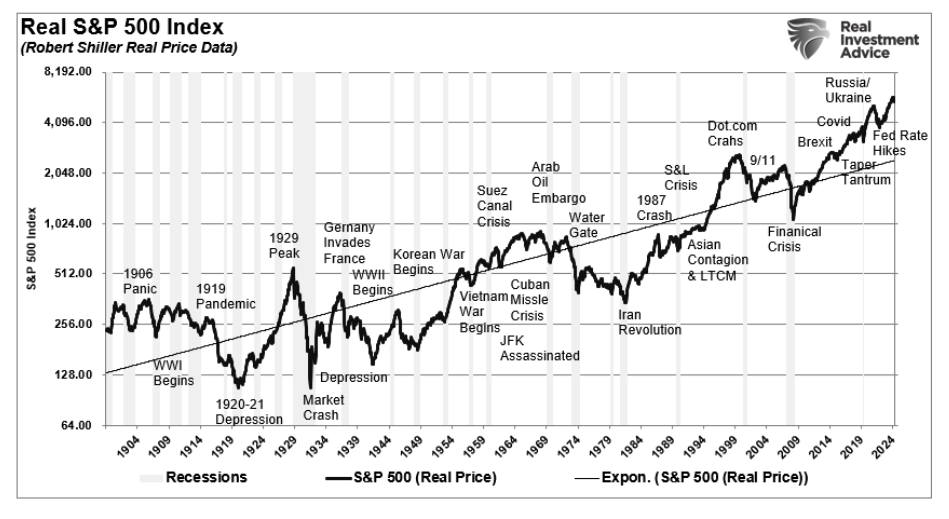

The point for investors is that despite headlines and narratives, the bull market’s resilience builds from cold, hard data. Throughout history, we have faced familiar risks: trade policy uncertainty, political volatility, and inflationary pressure.

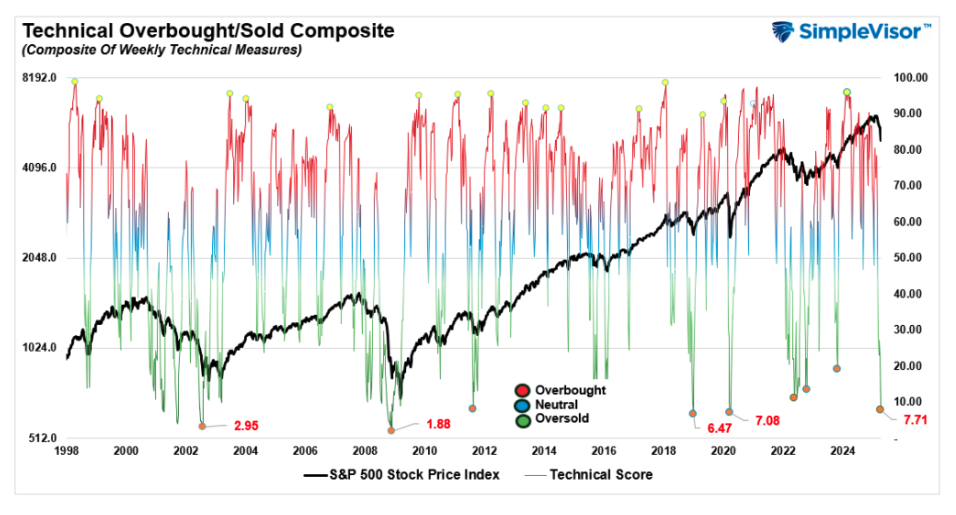

These elements are part of a broader tapestry already reflected in prices. As shown, the market responded by holding the rising bullish trend line from the October 2022 lows and then accelerating on signs of stabilization. The market rally above key moving averages, the breakout to new highs, and the reversal of the “Death Cross” are all very bullish developments suggesting the bulls remain in control.

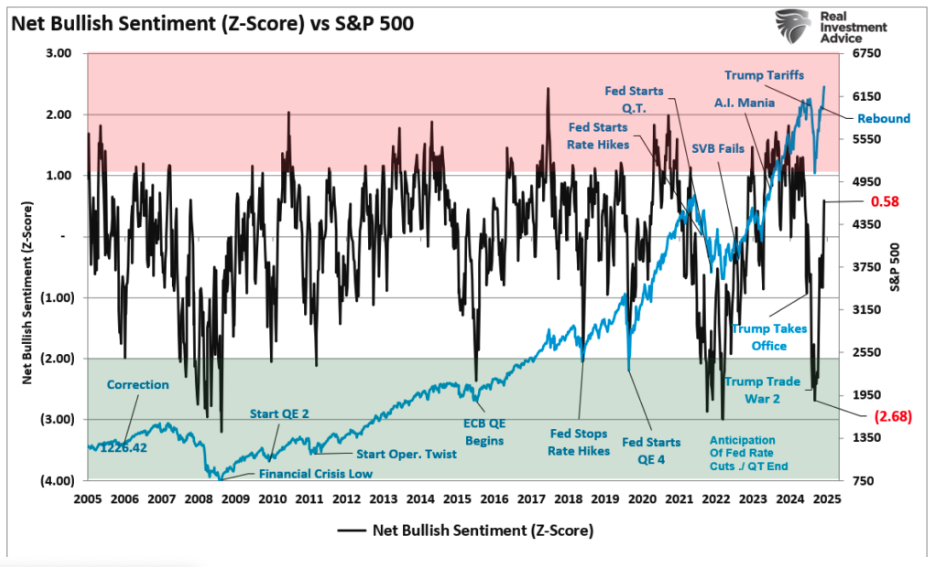

With these key resistance levels behind us, and sentiment turning bullish, but not near extremes, this suggests the April “Liberation Day” correction is behind us, and the bull market is continuing.

Despite ongoing headlines from media outlets touting “the end of U.S. exceptionalism,” the correction laid the groundwork for further gains. Technicals validate this trend, while fundamentals, from labor markets to corporate profits, reinforce it. Investors who continue to fall prey to the narrative will eventually realize the data does not support it. Yes, March and April were stormy, but they may have strengthened, not broken, the bull market’s core by providing a healthy correction to reset previous exuberance.

Whether invested in the Magnificent Seven, high-quality cyclicals, or diversified funds, the path forward remains constructive. As we concluded in our articles on market narratives:

There will always be a headline or analyst warning you to step aside. Sure, some of those concerns may be valid. However, reacting emotionally, rather than logically, often results in poor investor outcomes.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Real Investment Advice

Read more commentaries by Real Investment Advice

There will always be a headline or analyst warning you to step aside. Sure, some of those concerns may be valid. However, reacting emotionally, rather than logically, often results in poor investor outcomes.

There will always be a headline or analyst warning you to step aside. Sure, some of those concerns may be valid. However, reacting emotionally, rather than logically, often results in poor investor outcomes.