Clarity Amid the Noise

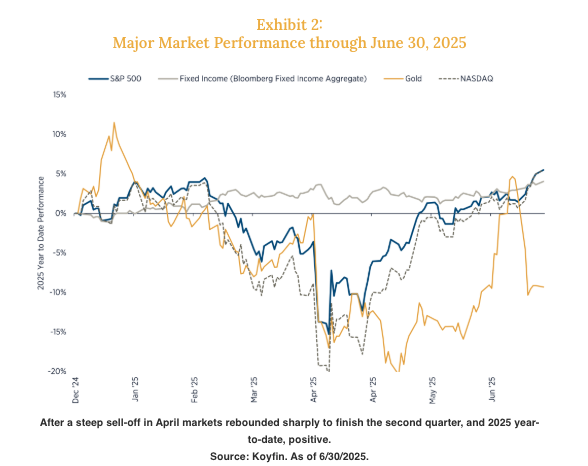

Markets have a way of humbling even the most seasoned investors. The first half of 2025 reminded us of this, as an aggressive 15%+ selloff in April was matched with a nearly 20% gain in less than 80 days, one of the fastest recoveries in history. While trade tensions, tariff announcements, and policy uncertainty dominated the news cycle throughout the quarter, disciplined investors who stayed focused on the long-term, rebalanced and deployed fresh capital, saw their portfolios recover and push to new highs by June.

This mid-year market outlook comes at a time when volatility, policy uncertainty, and shifting leadership are colliding with surprising resilience in both the economy and equity markets. Looking back this year has been a year of volatile emotions – early euphoria, fear-driven selloff, and then an optimism fueled rebound. Importantly, the market’s dramatic drop and recovery are a reminder to all investors that long-term investing is about discipline. Timing the market may be tempting, but staying invested continues to be the more rewarding strategy.

The defining characteristic of 2025’s first half has been the implementation and evolution of new trade policies, creating both challenges and opportunities for investors. The escalation that began in February with targeted tariffs on China, Canada, and Mexico culminated in April’s sweeping tariff announcements, before moderating toward a more measured approach in Q2.

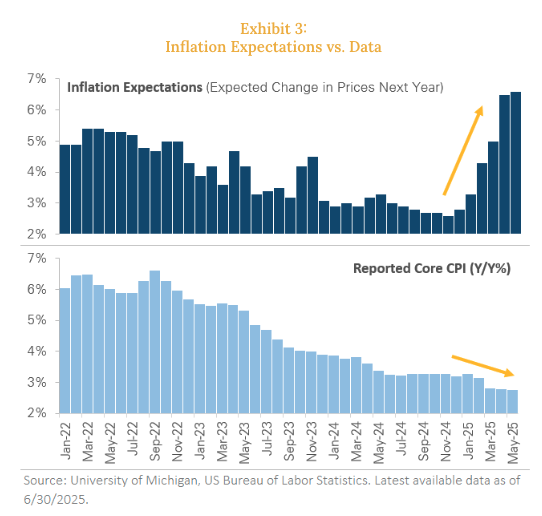

Looking ahead to the second half of 2025 the backdrop remains noisy. Tariff policy continues to shift, inflation expectations are rising (recent commentary from the Fed suggests it would have already cut rates if not for tariff-related inflation concerns), and consumer confidence is softening. However, hard economic data continues to suggest a more resilient economy – corporate balance sheets remain healthy, consumer spending is resilient, and the Federal Reserve’s patient approach to monetary policy is providing a supportive backdrop.

For investors, the opportunity set is broadening. We continue to favor U.S. large-cap equities, high-quality municipal bonds, and select international opportunities where valuations remain attractive. The key is filtering signal from noise and staying focused on what we can control: building diversified portfolios aligned with long-term goals.

The Economy and Markets

-

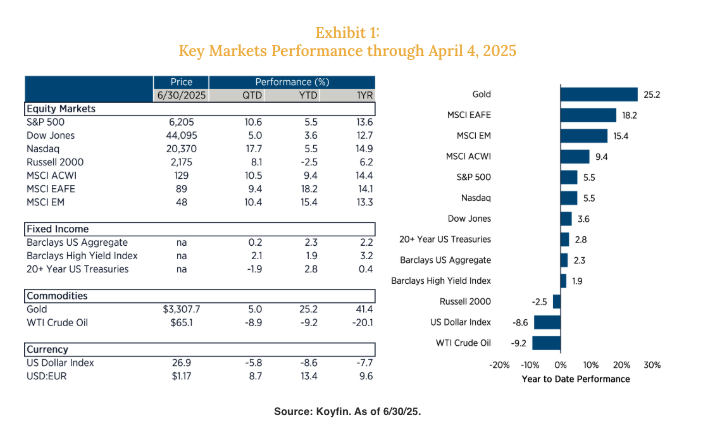

Market Rebound Catches Most Off Guard. The S&P 500 gained 10.8% in Q2 after dropping 4.3% in Q1, bringing the year-to-date return to +6.1%. A mid-quarter rally, fueled by easing trade tensions and resilient earnings, helped reverse earlier losses. Small caps and tech stocks led the way.

-

Tariff Whiplash. Trade policy drove market swings as sweeping tariffs were announced in early April, only to be softened by temporary exemptions in May. The result was an extremely bifurcated quarter, with April weakness followed by a surge in May and June.

-

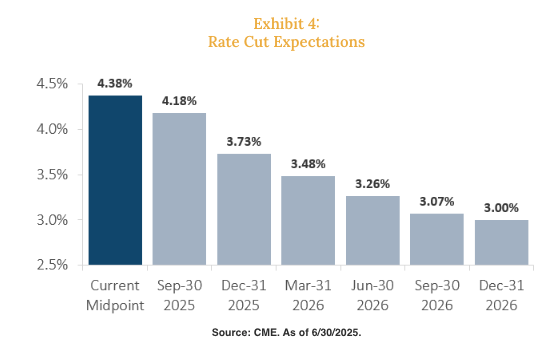

Fed on Hold, Cuts (Maybe) Coming. The Federal Reserve held rates steady in Q2 but is expected to cut twice in the second half of 2025. Tariff-driven inflation and slowing growth have created a complex environment, with the Fed noting they would have cut rates already in the absence of tariffs. Markets are pricing in rate cuts starting in September, which we expect will drive further market upside.

-

Economic Data Weakening. First quarter US GDP growth came in at 2.5% despite trade policy headwinds, demonstrating the economy’s underlying resilience. At the same time consumption and business investment are slowing, and forward-looking indicators such as hiring, manufacturing, and consumer sentiment suggest a softer back half of the year.

-

Dollar Weakness Fuels International Outperformance. Non-U.S. equities have outperformed in both Q1 and Q2, driven by a weaker dollar and relative valuation advantages abroad. Developed international markets in particular are attracting capital as US foreign policy remains uncertain.

TIMELY TOPICS

Where to Deploy Capital in 2H25

The back half of this year presents a unique environment: decelerating growth, persistent political risk, and a market that has already rebounded significantly. Where should investors look?

We believe three themes stand out:

-

Equities and Risk On Trades: Valuations are coming down and corporate earnings continue to support equity upside. With rates more likely to come down vs. up we see greater return opportunity in equities.

-

Global Diversification Matters Again: With the dollar weakening and U.S. valuations stretched, developed international markets provide compelling opportunities. Earnings growth in Europe and Japan is catching up, and global infrastructure exposure can add ballast.

-

Infrastructure and Real Assets: AI-driven power demand, aging demographics, and essential real estate (like medical and grocery-anchored properties) are all tailwinds for infrastructure and real assets. Select listed infrastructure and REITs offer both income and long-term growth exposure.

As always, our focus remains on filtering out the noise, staying invested with intention, and building portfolios aligned with long-term objectives. As we assess this mid-year market outlook, investors who remain nimble and diversified continue to be best positioned to navigate what comes next

Please read important disclosures here.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Defiant Capital Group

Read more commentaries by Defiant Capital Group