We expected 2025 to unfold in two halves, starting with a supportive macro backdrop carried over from 2024. We also braced for elevated uncertainty in the second half of the year, believing tariffs would eventually take hold.

Instead of a smooth start, markets whipsawed in April when US tariff policy came sooner—and more extremely—than expected. Meanwhile, more pro-growth fiscal policy and expectations for rate cuts were pushed back to later in the year.

As we look to the second half of 2025, key macroeconomic drivers will likely include the direction of US fiscal and trade policy, the Federal Reserve’s monetary-policy stance and timing of potential rate cuts, and ongoing geopolitical and other related uncertainties.

Recession remains a tail risk. However, we believe its probability is relatively low and our base case is for a downshift to moderate economic growth, depending on how the global trade situation unfolds. We think multi-asset income investing is well suited for this environment, not only for yield potential but for resilience against a more uncertain backdrop.

Stay “Close to Home” Given a Volatile Backdrop

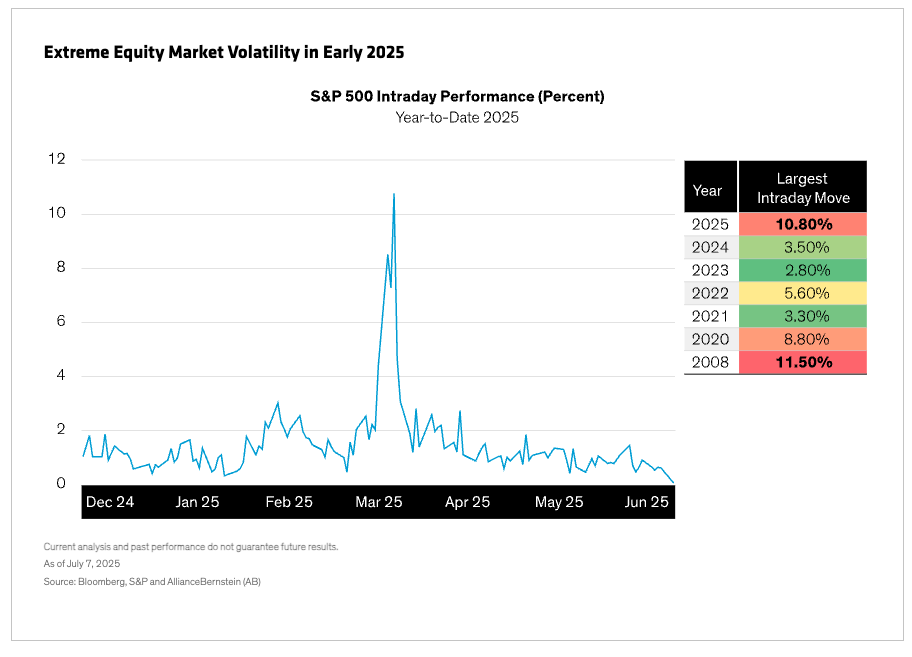

Policy shifts have driven extreme bouts of market volatility in the first half of the year, particularly among US markets. It has been a bumpy ride for US Treasuries and the dollar in particular, while US stocks experienced their largest intraday moves since the global financial crisis of 2008 (Display). In this environment, we think it’s best to trust diversification that aligns with strategic allocations rather than overly tactical market timing.

Credit Where Credit is Due

After widening in the weeks around tariff announcements, credit spreads are now closer to their historical lows—reflecting the relatively benign macroeconomic backdrop. Credit has been remarkably resilient so far this year, more so than equities, and has been an important source of both income and diversification for multi-asset strategies.

Spreads (or valuations) may look expensive, but we believe that it’s more important to focus on yield levels. In fact, yield-to-worst has been a better predictor of return over the next three-to-five years than spread, even in the most challenging bond markets. And today, yields across credit are attractively high. We currently prefer higher-quality issuers, such as BB-rated, over lower-rated bonds to help manage tail risk.

Positioning for a Steeper Yield Curve

We continue to view duration, or sensitivity to changes in interest rates, as an important diversification lever within a multi-asset income strategy. We expect US inflation to peak in the third quarter due to earlier tariff pressures, but with labor and wage trends cooling, the Fed should have room to resume rate cuts by year-end.

In the meantime, interest rates are still trying to find balance between easing policies on one side and rising yields among longer maturities on the other. This had caused a steady steepening of the yield curve. As a result, we think it’s prudent to lean toward short-to-intermediate bond maturities, where the risk-reward trade-off between yields and interest-rate risk is more attractive.

Casting a Wider Net for Equity Opportunities

From our perspective, markets are probably past the worst of the trade war turmoil, and tariff levels will likely settle just above where they began the year. We’re not out of the woods, but with a little more policy clarity than a few months ago, businesses are better able to lay out plans. Labor markets, manufacturing and services output, and corporate earnings have also shown resilience.

We continue to buy into the case for US exceptionalism, believing that the country’s unique qualities still support compelling and diverse investment opportunities versus other countries. But we also see the many benefits of global diversification among stocks and bonds.

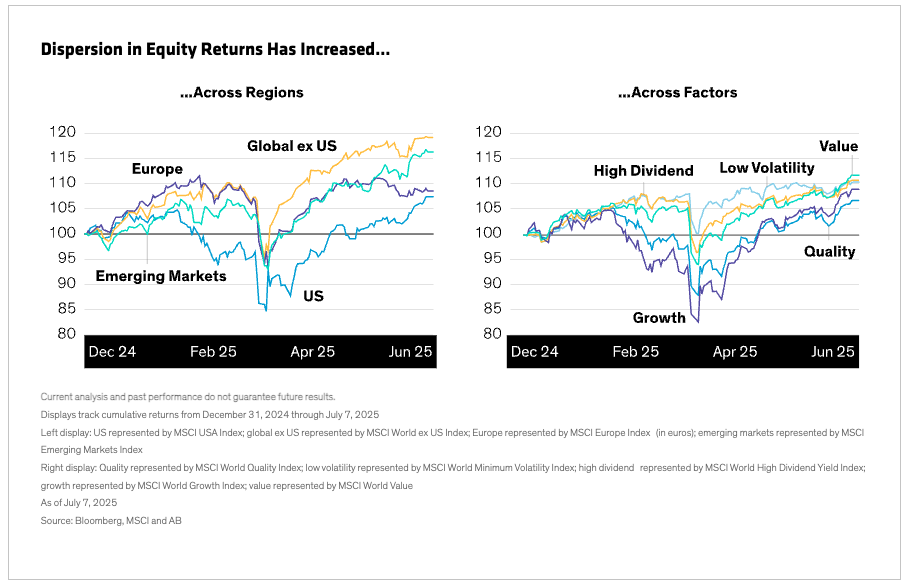

Despite their volatile patch in April, global stock markets touched record highs by midyear. Returns have continued to broaden beyond a concentrated handful of US-technology highfliers to companies across sectors, regions (Display, left) and factors, such as growth, value and high-dividend payers (Display, right). This reinforces why we believe a broad mix of equities makes for effective multi-asset income strategies.

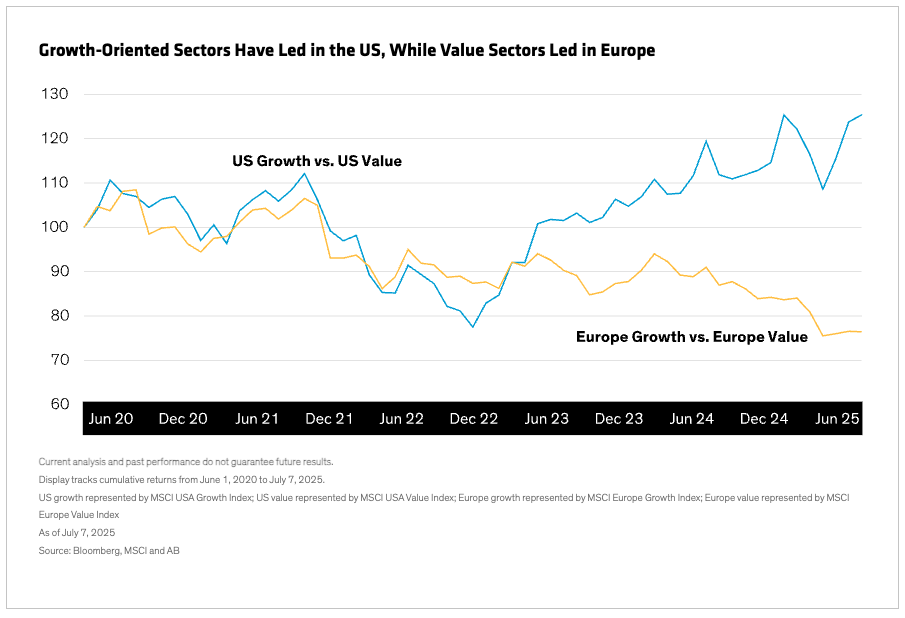

US large-cap stocks, global dividend payers and select cyclical names seem attractive right now. To us, it’s a powerful combination that offers tech growth and innovation exposure, which has led in the US. It’s complemented by value and income potential from European companies (Display), especially banks, which should benefit as monetary policy normalizes across more regions. The broader exposure also helps balance equity risk among different types of growth drivers, from reinvestment and share buybacks to dividends and pricing power.

Multi-Asset Income and the Big Picture

We expect slower economic growth in the second half, but the degree depends on the evolving tariff situation. Other key macroeconomic drivers will include the timing of additional rate cuts as well as geopolitical and election-related uncertainties. Nonetheless, pro-growth fiscal policy, including the One Big Beautiful Bill Act’s sweeping tax cuts, should help offset some of that drag, which we think makes a recession less likely.

By fanning out across markets and factors, multi-asset income strategies have tended to navigate uncertainty effectively. Since environments can change quickly, investors still need to stay flexible. But from our perspective, a multi-asset income strategy is well-equipped to respond, offering resilience and attractive risk-adjusted return potential.

The views expressed herein do not constitute research, investment advice or trade recommendations, and do not necessarily represent the views of all AB portfolio-management teams, and are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein