As 2025 progresses, investors and policymakers are navigating a highly complex economic landscape shaped by three powerful and interrelated forces: evolving trade policy, a cautious U.S. Federal Reserve (Fed), and growing concerns over U.S. fiscal discipline. Each of these risks is reshaping expectations for growth, inflation, and asset prices, which makes this a particularly challenging environment. While these elements introduce complexity, they also may represent opportunities for savvy investors to adapt, reposition, and potentially thrive.

-

Tariffs: A Hidden Tax with Broad Reach

One of the most significant policy shifts of the year has been the escalation in tariffs. Even assuming a base tariff level of 10% plus additional tariffs on certain industries and countries, such as China, economists have described this shift as one of the largest effective tax increases in the past 50 years. These levies function as a stealth tax, raising costs not just for consumers purchasing imported goods, but also for domestic companies that depend on global supply chains. Key sectors, such as automotive manufacturing, electronics, and household appliances, are particularly vulnerable.

The immediate impact is twofold. First, manufacturers are seeing input costs rise, squeezing profit margins unless they can pass those costs to consumers. Second, these price increases are reigniting inflationary pressures at a time when the economy was hoping for relief. As a result, tariffs are likely to exert a drag on economic growth while complicating the Fed’s efforts to tame inflation. From an investment perspective, we have seen markets react to the ever-changing tariff landscape both positively and negatively. Our forecast for equity returns has increased since the start of the year as the equity market has pulled back to more attractive levels. This has increased the opportunity set for more tactical investments as resilient industries and companies fell along with those more vulnerable to the tariff landscape.

-

The U.S. Federal Reserve: Higher for Longer

Just months ago, markets were pricing in up to four rate cuts by the Fed in 2025. Currently, consensus forecast is for two rate cuts in 2025. With inflation proving stickier than anticipated, the Fed has shifted to a much more cautious stance. This “higher-for-longer” interest rate environment has significant implications for financial markets. Borrowing costs remain elevated, weighing on consumer spending and business investment. Risk assets, particularly growth stocks and long-duration bonds, are being repriced as liquidity tightens. Nevertheless, the Fed’s policy trajectory is headed in the right direction and additional rate cuts can be a powerful force in stimulating the economy and markets. There tends to be specific opportunities that exist in a rate cutting cycle that should not be overlooked.

-

Fiscal Policy: Deficits and Creditworthiness

Adding to the uncertainty is the deteriorating fiscal position of the U.S. government. Persistent deficit spending has drawn the attention of credit rating agencies with Moody’s recently downgrading its outlook on U.S. sovereign debt. While a default on Treasury securities remains extremely unlikely, the symbolism of a downgrade is powerful. Treasuries serve as a benchmark for everything from mortgage rates to corporate borrowing costs.

As interest payments on federal debt continue to balloon, concerns grow about the long-term sustainability of U.S. fiscal policy. A diminished perception of Treasury reliability could increase risk premiums. We have seen downgrades to the U.S. treasury by other rating agencies in the past and they have historically created short term volatility. Keep in mind, in aggregate the U.S. Treasury bond is still the most sought after in the world. Much like the equity market, some repricing can create near term tactical opportunities in the fixed income marketplace.

Investment Themes for a Volatile Landscape

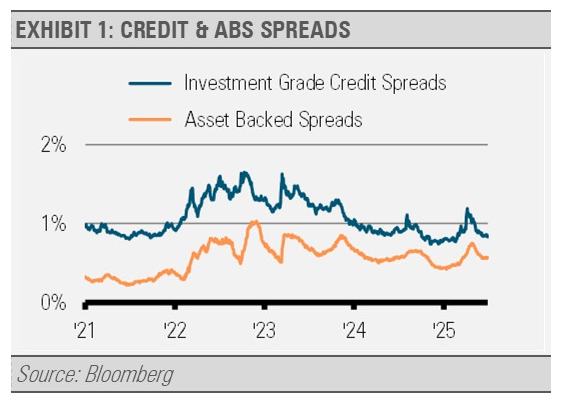

In this environment, prudent investment strategy calls for selectivity and risk management. Equities with strong earnings consistency and low financial leverage, as well as industries less directly exposed to tariff impacts, such as those in the software and insurance industries, may outperform. On the fixed income side, intermediate and short-duration corporate bonds, as well as high-quality asset-backed securities, can offer a balance of yield and capital preservation. In fact, high investment grade and high-quality asset backed securities offer an attractive yield over similar duration Treasury bonds (exhibit 1). Furthermore, the different risk profiles of corporate bonds and asset-backed securities may offer a level of diversification benefit as well.

As investors adapt to this new normal, resilience and quality are likely to outperform riskier, more speculative bets. The crosscurrents of tariffs, rates, and deficits make clear: this is a market that should reward discipline and a forward-looking approach.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.

Read more commentaries by Stringer Asset Management