Last week's economic data presented a picture of consumer resilience emerging alongside the continued challenge of rising inflation. While consumer spending staged a significant rebound in June, inflation heated up for a second straight month. This occurred even as consumer sentiment improved to its best level since February, though consumers remain cautious about future price increases. The market reacted positively to the data, climbing to a new record high on Thursday, despite earlier volatility in the week from rumors that President Trump would fire Fed Chair Jerome Powell.

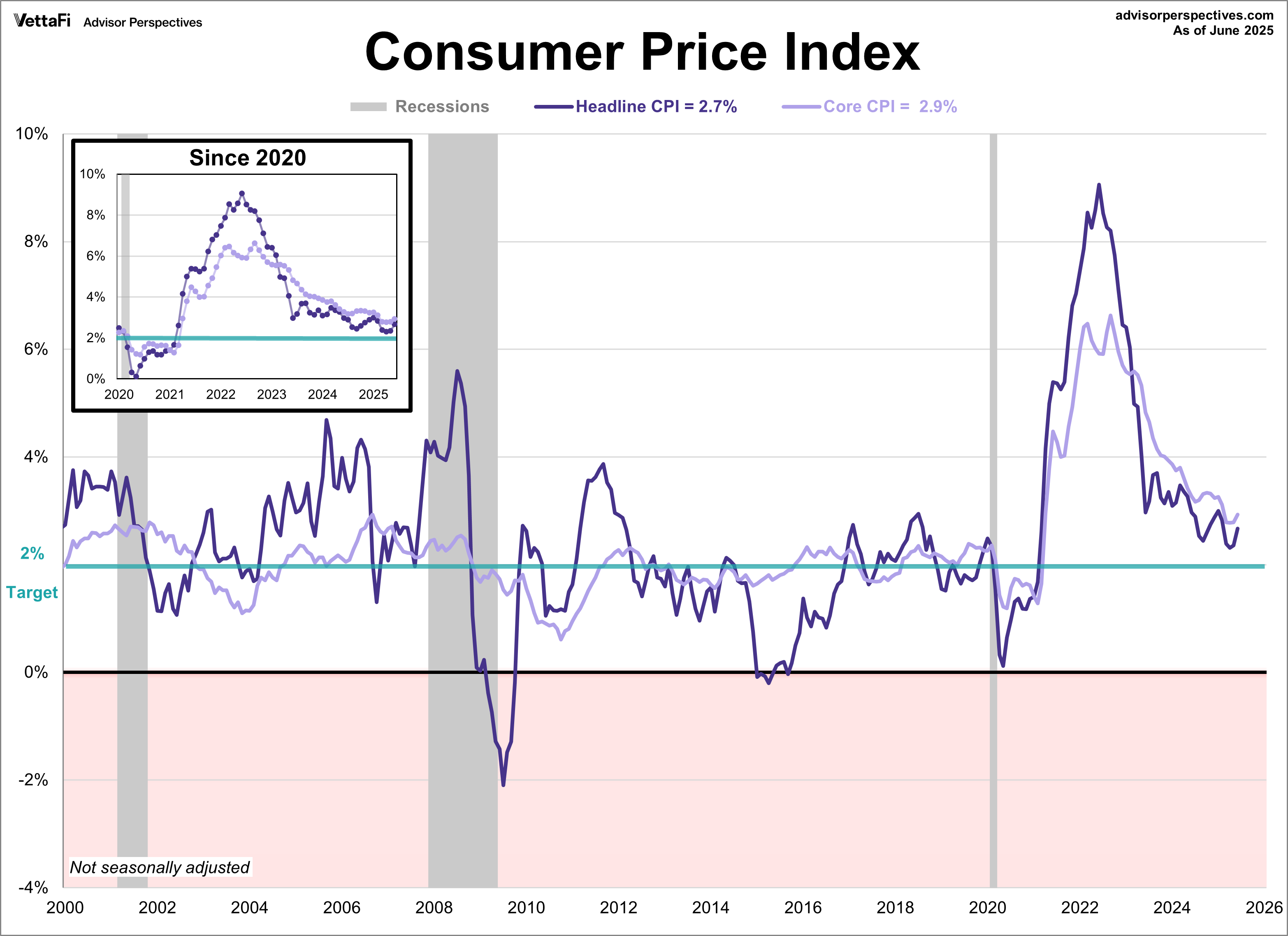

Consumer Price Index

Inflation heated up for a second straight month in June as the effects of tariffs are starting to take hold. In June, the Consumer Price Index (CPI) rose 2.7%, an uptick from 2.4% in May and higher than the expected 2.6% growth. On a monthly basis, prices were up 0.3%, as expected. Core inflation, which excludes volatile food and energy prices, rose to 2.9% in June. This was up from 2.8% May but below the expected 3.0% annual growth. Core prices were up 0.2% on a monthly basis, less than the projected 0.3% increase.

Driving the overall price increase in June were higher shelter, gasoline, and food costs. Additionally, the indexes for household furnishings, medical care, recreation, apparel, and personal care all rose from the previous month. On the opposite end, the indexes for used cars, new vehicles, and airline fares declined.

The latest report showed signs that tariffs are beginning to push prices up for certain consumer goods, specifically apparel, footwear, and furniture, while other categories appear less tariff-sensitive. The full inflationary impact of tariffs will continue to evolve over the coming months, which will likely keep the Fed in “wait-and-see” mode.

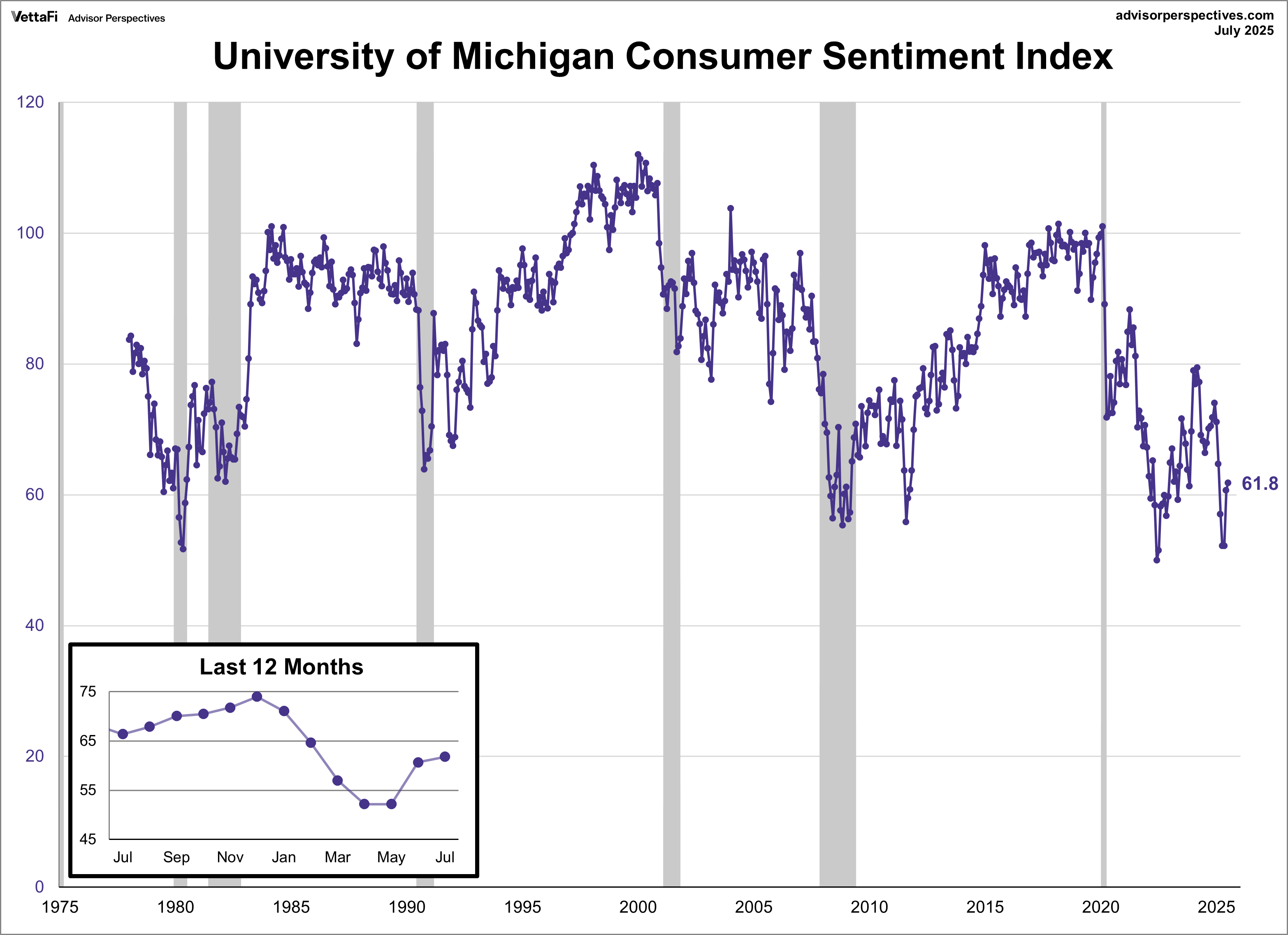

Michigan Consumer Sentiment

Consumer sentiment improved for a second straight month in July but consumers remain unconvinced that inflation risks have subsided. The Michigan Consumer Sentiment Index increased 1.1 points to 61.8 this month, its highest level since February but still on the historically low end. This represents a 1.8% increase from June’s final reading and a 6.9% drop from one year ago.

The current conditions index rose for a second straight month to its highest level since January while the expectations index increased for a third consecutive month to its highest level since February. Notably short run business conditions improved while expected personal finances pulled back. Based on responses, consumer confidence seems to be primarily influenced by inflation and shifting trade policy as other policy developments had minimal impact on sentiment.

Inflation expectations eased for both near and long term. Year ahead expectations cooled for a second straight month from 5.0% in June to 4.4% in July. Meanwhile, five-year expectations edged lower for a third consecutive month to 3.6%. Despite softening expectations this month, both series remain historically high, reflecting consumers’ beliefs that there is still substantial risk that inflation will increase in the future.

The Consumer Discretionary Select Sector SPDR ETF (XLY) is tied to consumer sentiment.

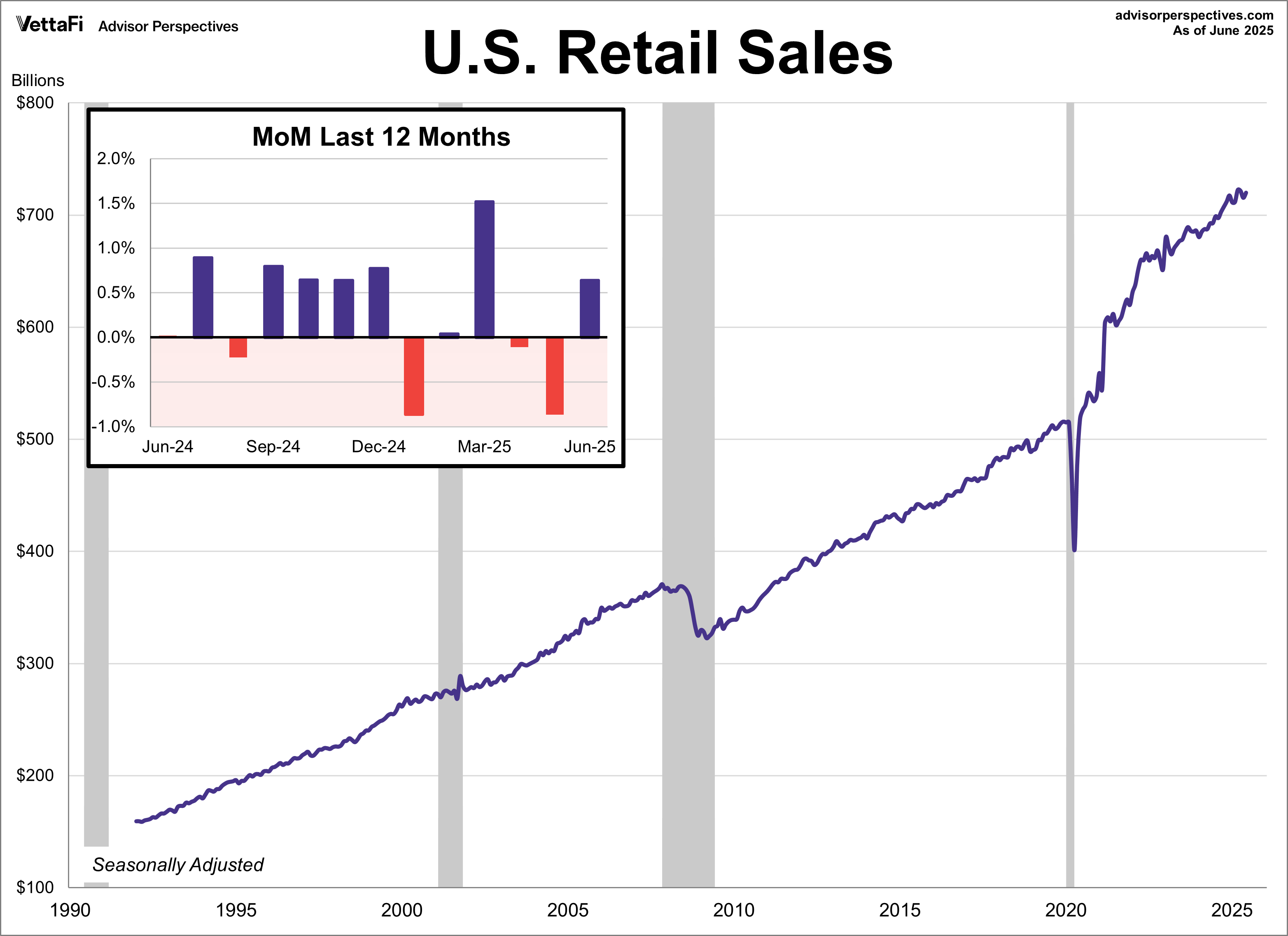

Retail Sales

Consumer spending rebounded in June after two straight months of decreased spending due to growing concerns about tariff-driven price increases. Retail sales rose 0.6% in June, a sharp contrast to the 0.9% decline in May. This was significantly higher than the expected 0.1% monthly rise.

The increase in sales last month was seen across many types of businesses. Spending at motor vehicle dealers (1.2%), building material stores (0.9%), clothing stores (0.9%), and restaurants and bars (0.6%) were among categories that saw the largest monthly increases. On the other end, there was a decline in spending at furniture stores (-0.1%) and electronic stores (-0.1%).

Core sales, which exclude autos, also surprised to the upside last month, posting a 0.5% monthly gain. This was up from May’s 0.2% decline and higher than the expected 0.3% growth. Meanwhile control purchases—a crucial GDP input and an even more “core” view of retail sales—beat expectations, rising 0.5% from the previous month. This was higher than the expected 0.3% growth

Retail sales could impact the SPDR S&P Retail ETF (XRT), VanEck Retail ETF (RTH), Amplify Online Retail ETF (IBUY), and ProShares Online Retail ETF (ONLN).

Market Reactions

The S&P 500 notched a new record high last Thursday, its ninth of the year. The index ultimately finished the week up 0.6%, its third weekly gain in the past four weeks. As a result, the SPDR S&P 500 ETF Trust (SPY) rose 0.6% last week. Meanwhile, the S&P Equal Weight Index was down 0.1% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) fell 0.1%.

The 10-year Treasury yield finished the week at 4.44%, while the 2-year note finished at 3.88%.

The CME FedWatch Tool currently shows a 95% likelihood that the Fed will hold rates steady at their meeting next week. Markets are pricing in two 25 basis point cuts for this year coming at the September and December meetings. Additionally, three 25 basis point cuts are projected in 2026.

Economic Data in the Week Ahead

The economic calendar for this week is relatively light. The most notable release will come on Friday with June’s durable goods data which will show trends in new orders for manufactured goods, reflecting both business spending and consumer demand for big-ticket items. Other releases for the week include June’s data for existing and new home sales as well as the Chicago Fed National Activity Index (CFNAI) and the Kansas City Fed regional manufacturing index.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Read more commentaries by VettaFi