Key Takeaways

- Markets will likely stay unsettled into the second half of the year. Context and discipline are key ingredients for investment strategies.

- Equity markets are still concentrated, but we see opportunities in quality, both value and growth, and low-volatility and high-dividend stocks for defensively minded investors.

- All-in bond yields remain attractive, and relative value opportunities are present within US credit markets and globally as yield curves diverge.

- High municipal yields, a steep yield curve and attractive valuations give investors the tools to design a muni bond allocation with strong potential.

Macro Resilience, but Watch for Signs of Strain

Despite heightened policy uncertainty, equities rebounded in the second quarter as the fundamental picture appeared largely unchanged. The US economy remained resilient, helped by the minimal impact of new tariffs on consumer inflation reports. Still, at this point most paths forward suggest higher inflation rates into year end.

The labor market has cooled, but driven by fewer hires rather than layoffs, and wage growth continues to outpace inflation. We’re watching for potential cracks, given recent developments such as jobless claims topping their pre-pandemic level. But we’re not sounding the alarm yet, because unemployment remains well behaved.

Economic growth remains relatively stable, though the data are noisy. For only the fourth time in a decade, real growth in gross domestic product (GDP) was negative. But strong demand for imports—which are subtracted from GDP—played a sizable role. We’re monitoring a downshift in consumer spending and business activity, especially in services, where a decline in new orders is flashing yellow.

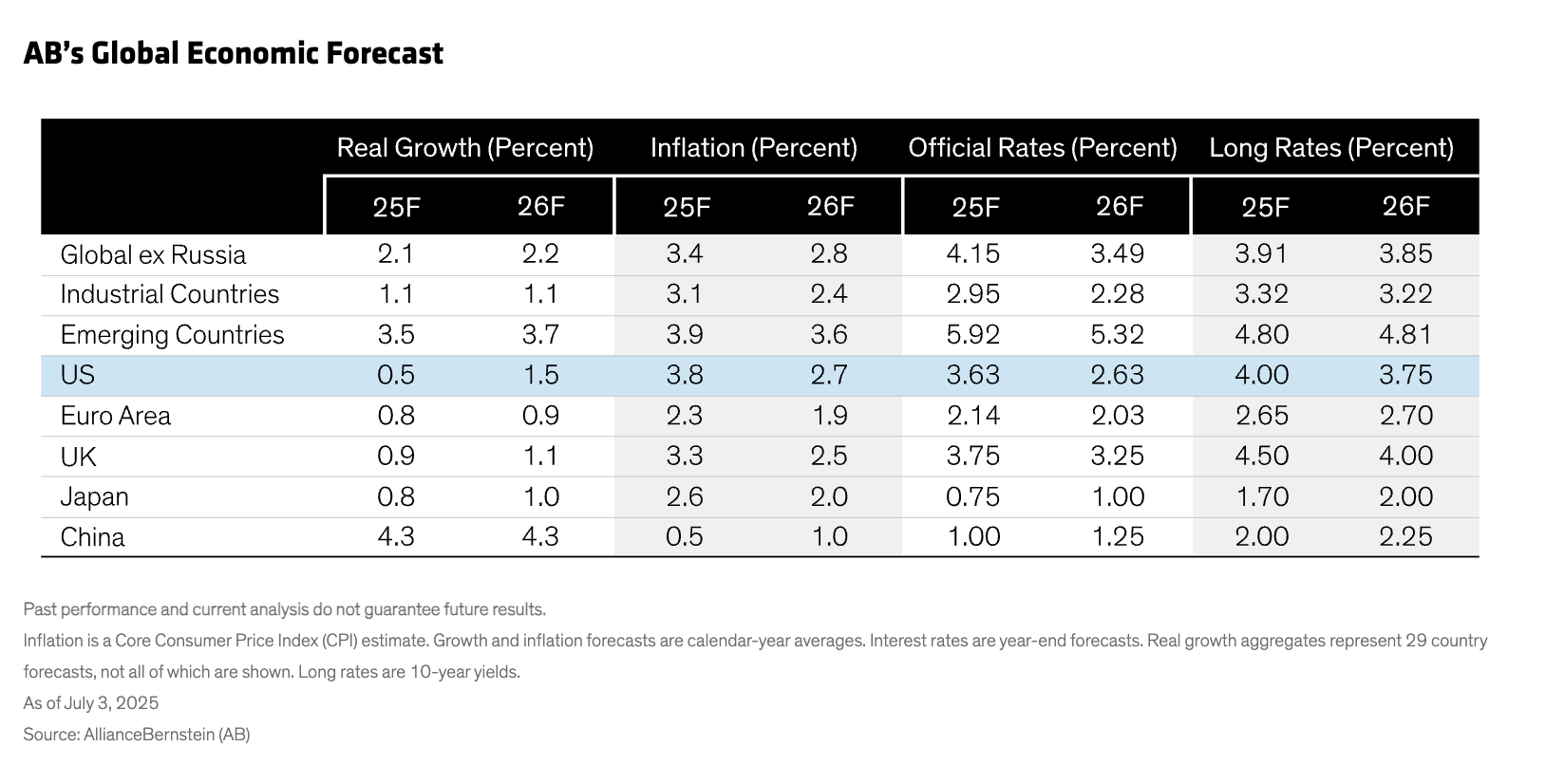

As for the Fed, uncertainty over fiscal policy—not fundamentals—has delayed expectations for the next rate cut. As debate continues within the central bank, the market still expects a lower terminal rate. The 10-year US Treasury yield, meanwhile, has bounced around a lot over the past two years; our forecast calls for a 4% yield at the end of 2025 and 3.75% at the end of 2026 (Display).

Concentration Remains in Equity Market, but Quality Still Resonates

With the investor pendulum having swung back toward euphoria, valuations for the S&P 500 are near record highs. Earnings growth should continue, but the rate bears watching. Overall, 2025 estimates are higher than 2024’s, but revisions have been trending lower. Only a few sectors have seen positive to limited revisions since last summer’s estimate peak, and many of them face trade pressures.

In the second quarter rally, the growth style caught up with value and international stocks continued to advance. The S&P 500 is still concentrated, but Mag Seven leaderboard has been shuffled relative to 2023–24. Forecasting equity returns is especially challenging now: Tariffs, fiscal-policy uncertainty and immigration’s potential labor impact stand as possible headwinds. On the other side of the coin, corporate tax cuts, deregulation and the AI boom could provide tailwinds.

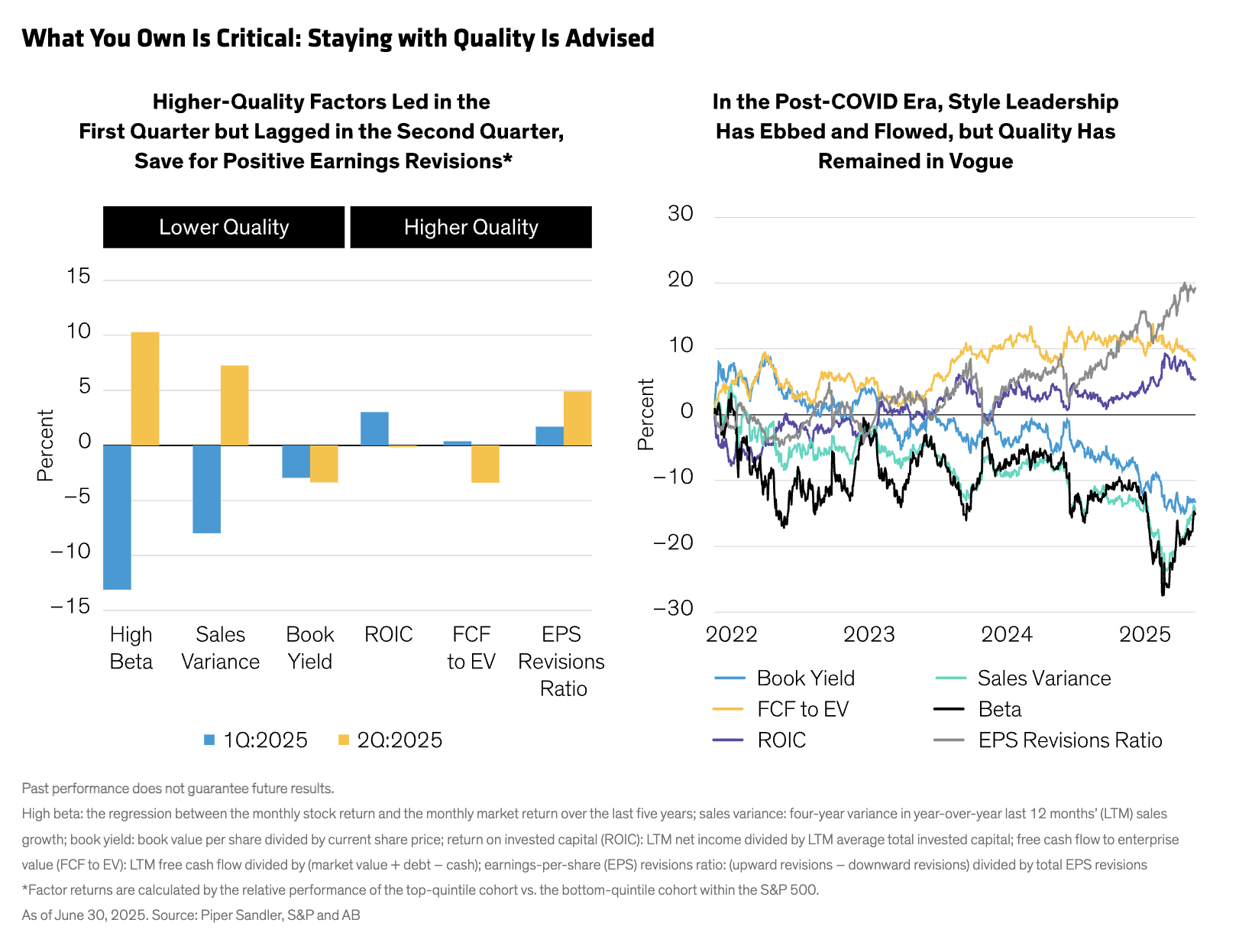

For equity investors facing a potentially turbulent environment, what you own is critical, and we think sticking with quality is warranted (Display). In the post-COVID era, style leadership has ebbed and flowed but quality has stayed in vogue. Because policy variables are style-agnostic, we think it makes sense to say “yes” to both growth and value.

For defensive-minded investors, low-volatility and dividend-growth stocks may make sense with the market pricing in minimal macro risks. Also, a solid earnings picture for international equities and a weaker US dollar seem to support opportunities in that arena, where we maintain conviction on services versus goods given the still-murky trade environment.

Bond Markets: All-In Yields Still Look Compelling

In the bond world, the US Treasury yield curve has continued to steepen, with longer maturities seeing historic volatility. In our view, the US Treasury market should remain resilient despite deficit concerns. Markets are digesting the new supply, and foreign demand for Treasuries is still robust—it remains the largest and most liquid bond market.

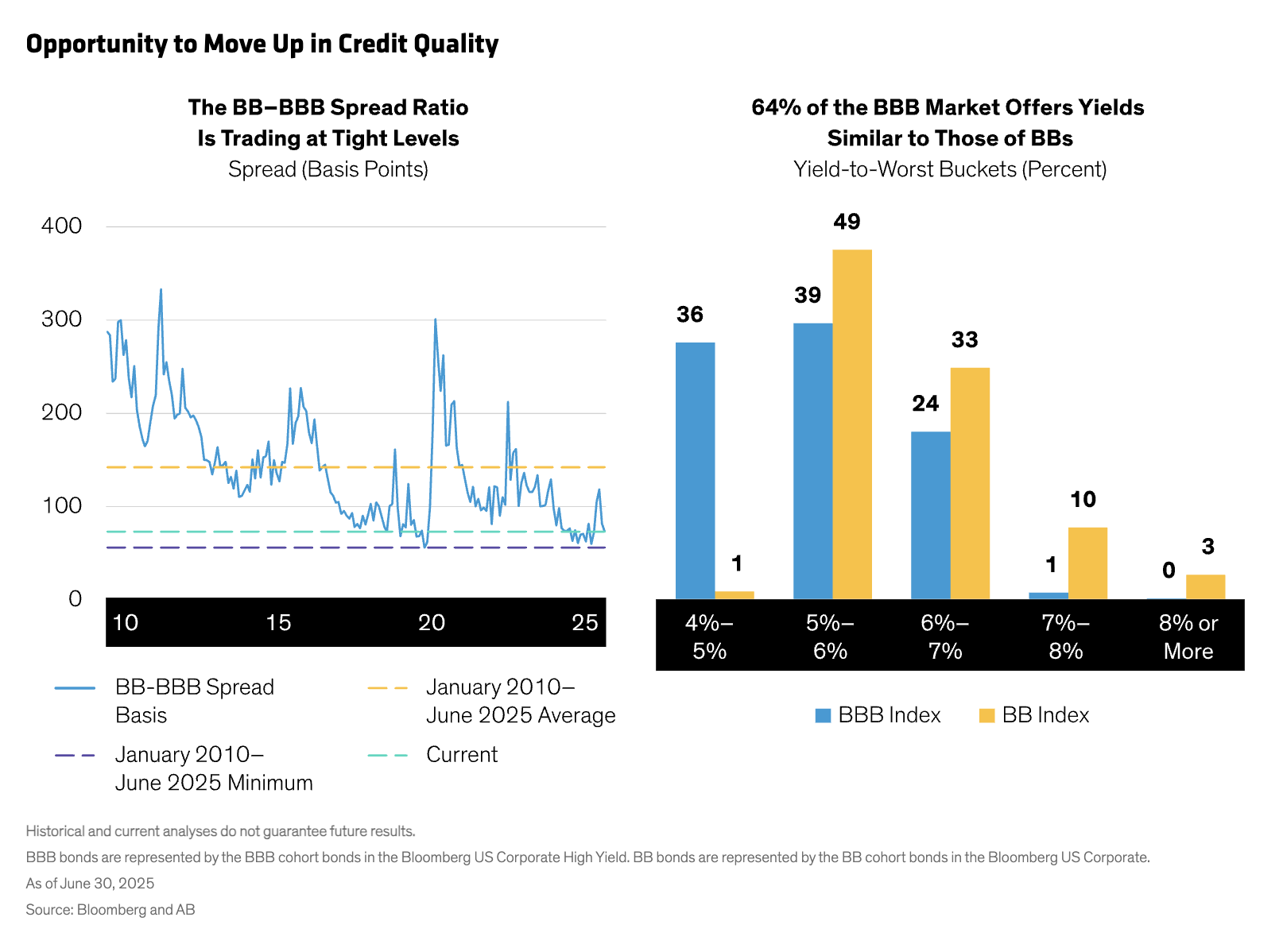

Credit spreads have returned to pre-liberation day levels, but all-in yields are still attractive and relative value opportunities remain. For example, investors can move up in quality from BB rated bonds to BBB rated bonds without giving up much—or, in some cases, any—yield (Display). US high yield spreads are also tight but still compelling, and yield to worst has been a strong predictor of future returns. While technical conditions have weakened, fundamentals remain supportive.

Because yields are diverging among regions, tapping into a global opportunity set may enhance diversification and returns. We think investors should spread their investments beyond the US to sectors such as global investment-grade and high yield credit, emerging market debt and even securitized sectors such as commercial mortgage-backed securities.

Muni Yields, Curve and Prices Paint an Attractive Picture

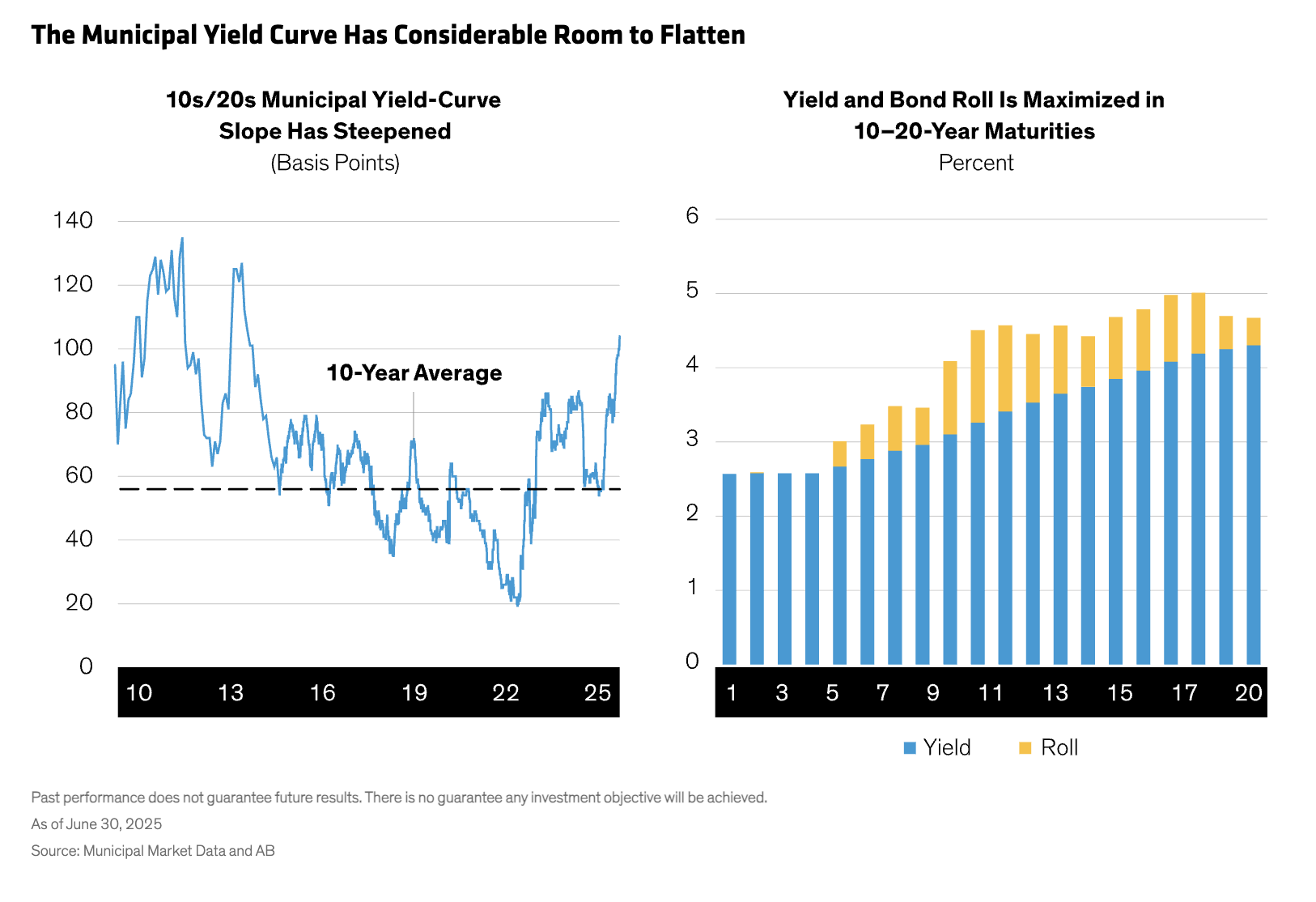

Municipal and Treasury yields have diverged in 2025, with Treasury yields falling year to date and muni yields rising with a surge in issuance. Today, municipal yields are high, the muni yield curve is steeper than that of Treasuries, and muni bonds are priced attractively. From our vantage point, this presents a compelling entry point.

The main reason for the steepening muni yield curve has been weaker demand for long-duration bonds. From the current starting point, therefore, we see considerable room for the yield curve to flatten (Display). A barbell maturity structure that combines short maturities with longer maturities, in our view, may maximize potential returns from yield and roll.

As for municipal credit, it has held its value well because technical conditions have been firmer, and today its income profile is extremely compelling, based on our assessment. All told, we think it makes sense to design muni allocations with an overweight to credit and overweight to duration through a barbell maturity structure. And above all, hold fast and stay agile.

The Big Picture View

We’re not surprised by the macro and market resilience, but it’s too soon to say we’re out of the woods. Markets will likely stay unsettled into the second half of the year, especially as potential pain from uneven fiscal policy comes into sharper focus. Although we expect more variables to start flashing yellow, the US economy and Fed are in relatively strong positions. In an environment where market “mania” has quickly taken hold, context and discipline will be essential for investors.

The views expressed herein do not constitute research, investment advice or trade recommendations, and do not necessarily represent the views of all AB portfolio-management teams, and are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein