Key Takeaways

- June saw a spike in oil prices, followed by a sharp pullback, but investors seemed relatively unphased. Why? The move itself was modest compared to other changes seen in recent history and proved to have little impact on the equity market itself.

- Since 2020, data shows that the correlation between oil prices and the U.S. stock market has a modest positive correlation. Further, gasoline and energy goods only account for 4% of consumer spending, down from 6% in 1990.

As oil shocks go, the late June spike in oil was one of the less disruptive ones. After surging more than 30% at the onset of the Iran/Israeli conflict, crude oil experienced the sharpest 2-day pullback since 2022. Even at the peak in oil prices, equity markets were incredibly resilient. My take is that absent a much sharper and prolonged spike in the price of crude, oil prices are not a major risk to stocks.

Stocks & Oil: It’s complicated

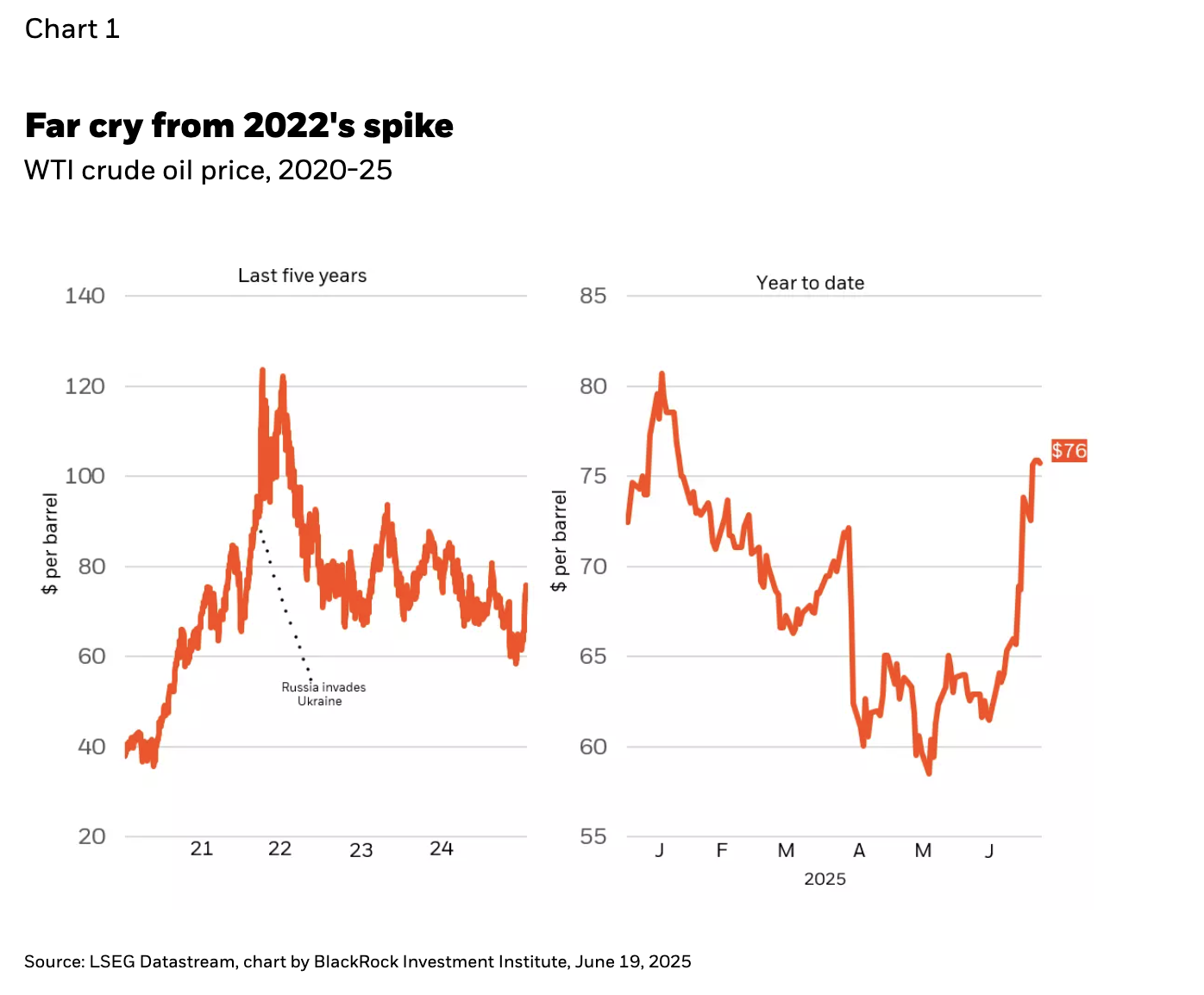

Why did investors look past the recent spike in oil prices? I’d cite several reasons, starting with the magnitude or lack thereof. While a 35% spike in oil is not trivial, it is modest relative to the doubling that occurred during the first Gulf War. Also worth highlighting that even at the peak of nearly $75/barrel, crude prices were still below the January peak and only back to last year’s average price, at around $75/barrel (see Chart 1).

Even when oil does spike, the relationship between stocks and oil is not what you’d expect. Based on data from Bloomberg, since 1990 there has been a modest positive correlation, approximately 0.15, between changes in oil prices and changes in the S&P 500. While this seems counter-intuitive, it makes sense when you consider that both stocks and oil are cyclical assets. In other words, both tend to rise when the economy is strengthening and fall on rising recession fears.

A good example of this dynamic occurred in May of 2020. Oil prices advanced nearly 90%, with the U.S. benchmark West Texas Intermediate (WTI) advancing from $18 to $35/barrel. That same month the S&P 500 rallied 4.5%. Both oil and stocks took comfort in an unprecedented set of monetary and fiscal packages, as well as a surprisingly resilient U.S. consumer.

Energy commands less wallet share

The risks from rising oil prices are normally two-fold: higher inflation leading to tighter monetary conditions and higher gasoline prices crowding discretionary spending. Both are less of a threat today. The Fed is likely to look past any temporary impact from oil on inflation. On the consumer side, energy spending is a far smaller percentage of wallet share than back in the early 90’s. According to the Bureau of Economic Analysis in 1990 gasoline and energy goods accounted for roughly 6% of consumer spending. Today, it is around 4%.

To be certain, lower-end consumers are more exposed to spikes in gasoline, particularly in the context of higher inflation on select consumer goods due to tariffs. But the key point is that, in aggregate, the U.S. consumer sector is less exposed to energy prices than was the case 35 years ago. And to the extent consumers are more insulated, the stock market probably is as well.

Russ Koesterich, CFA, JD, Managing Director and portfolio manager, is a member of the Global Allocation team as well as the lead portfolio manager on the GA Selects model portfolio strategies.

To obtain more information on the fund(s) including the Morningstar time period ratings and standardized average annual total returns as of the most recent calendar quarter and current month end, please click on the fund tile.

The Morningstar RatingTM for funds, or "star rating", is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure (excluding any applicable sales charges) that accounts for variation in a managed product's monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year 60-119 months of total returns, and 50% 10-year rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period actually has the greatest impact because it is included in all three rating periods.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© BlackRock

Read more commentaries by BlackRock