US Equity Multiples Are Back at Cycle Highs: But It’s Not the Usual Suspects

Forward P/Es in the US have climbed back to 22.5x — matching the highs of the current cycle.

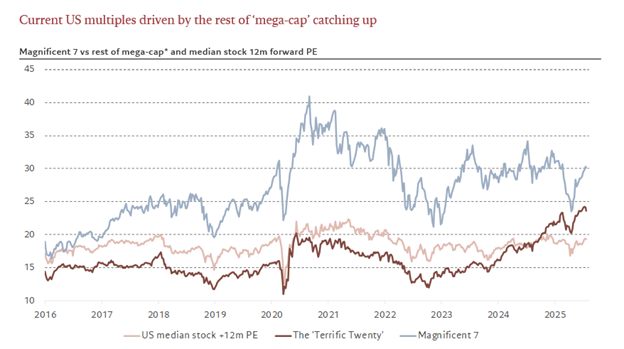

But this time, it’s not the Magnificent 7 driving the rerating.

In fact, the Mag 7 have derated significantly — from 42x forward earnings at the post-COVID peak to around 29x today. Over the past two years, their valuations have been flat, while performance has been powered by strong earnings delivery. Their premium to the rest of the market is now near the bottom of the AI-era range.

So far, so good.

So why are US multiples rising?

A group of 20 mega-cap stocks — the “Terrific 20” — has been a key driver of the move. These companies span a broad set of sectors more closely tied to the real economy, including financials, energy, industrials, consumer, and legacy tech. Names like Broadcom, Walmart, JPMorgan, Berkshire Hathaway, Visa, and GE Aerospace now account for ~17% of the MSCI US index, compared to 33% for the Mag 7.

This cohort has re-rated by ~50% over the past two years. At the individual stock level, many of the moves appear justified. But collectively, this presents a problem: more of the market is now expensive.

Why it matters

Broader participation is a positive — when it’s driven by earnings.

But when more of the market gets expensive, the narrative that “US equities aren’t overpriced, just a few exceptional companies are” becomes harder to sustain.

Today, the top two-thirds of the US market by index weight trades at 25x forward earnings. That’s not isolated.