Research Sector Update: A Return to Fundamentals

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey takeaways:

- After pulling back in the first quarter, risk assets such as leading technology stocks rebounded in Q2 as economic growth proved resilient and corporate earnings expanded despite trade frictions.

- However, with policy uncertainty ongoing, companies exposed to secular themes such as AI, electrification, and medical innovation may be best positioned to deliver gains going forward.

- We think investors should stay focused on these themes and use volatility to add to high-quality companies at potentially attractive valuations.

The second quarter began in dramatic fashion with “Liberation Day” tariffs announced on April 2. Broad U.S. equity indices plunged by 10% or more over the next several days, as investors began to assess the negative impacts that tariffs might have on global economic growth and corporate profitability.

Markets shook off these fears relatively quickly, however, as corporations reported generally strong quarterly earnings growth and provided better-than-feared guidance. Easing trade tensions also increased investor appetite for risk. We get the sense that fears over trade policy may already have peaked, an assessment that has boosted the performance of risk assets. We have also been encouraged by positive signs of growth outside of the U.S., especially in Europe, which may present opportunities for companies with international exposure.

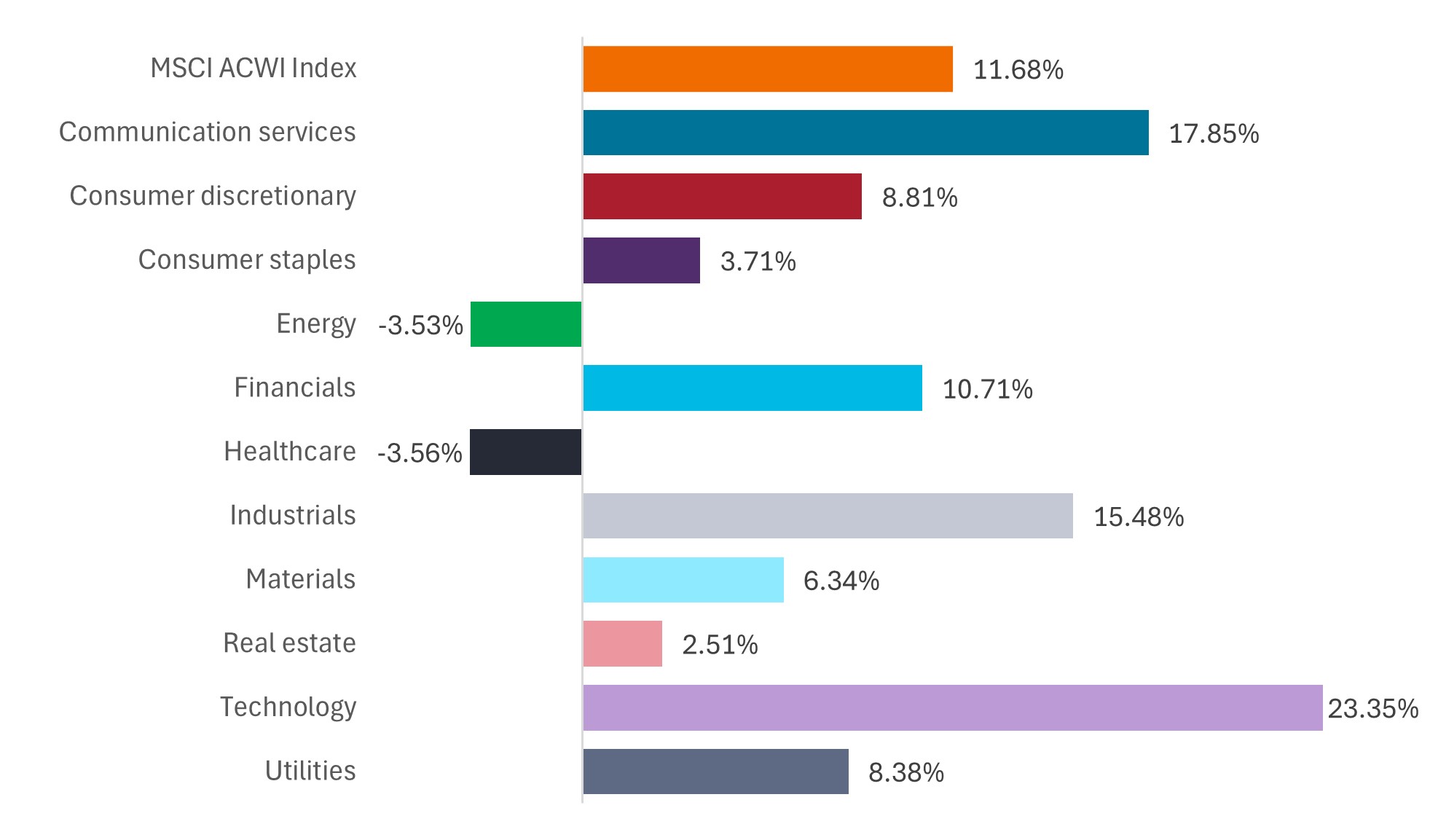

Q2 2025 Global equity performance (total return)

Risk assets such as technology and consumer discretionary stocks rebounded from their first-quarter losses.

Source: Bloomberg, data from to 31 March 2025 to 30 June 2025. Returns are for the MSCI All Country World Index (ACWI) and its 11 sectors. The MSCI ACWI Index captures large- and mid-cap representation across 23 developed markets and 24 emerging markets countries.

Technology: Prioritizing AI and digital innovation/monetization

Denny Fish and Jonathan Cofsky

What happened: The tech sector began the quarter with significant volatility, spurred by trade frictions and questions over the pace of industry spending on artificial intelligence (AI). By June, these concerns largely dissipated as tech giants such as Microsoft, Meta, Amazon, and Google confirmed that demand for AI capabilities showed no signs of abating. As a result, technology stocks, which saw losses in Q1, reversed course and delivered strong gains for the second quarter.

Looking ahead. Despite tariff-related uncertainty, we believe resilient U.S. growth and stabilizing economic trends in other regions bode well for cyclically oriented tech companies. We continue to see tremendous opportunity around secular growth trends such as AI. To that end, we expect more companies to begin integrating AI solutions into front- and back-office operations, creating an attractive flywheel if these applications improve revenue growth, increase efficiencies, and expand profit margins for customers.

To capitalize on these trends, we are focusing on leading hardware and semiconductor producers. We also see opportunity for software companies able to leverage access to client workflows and data to train and optimize AI models. Finally, we think companies developing more advanced AI platforms that handle complex tasks could be particularly well positioned, as these capabilities could lead to enhanced pricing power and durable competitive advantages.

Communication Services: AI and digital disruption open new opportunities

What happened: Communication services stocks outperformed the broader market in the second quarter, with many companies within the sector rebounding strongly from a Q1 sell-off. That includes streaming and music providers with subscription-based business models and firms on the leading edge of AI services and tools. By contrast, the sector’s traditionally more defensive companies, such as wireless and Internet providers, lagged the broader market advance, while investors weighed the potential disruption that could be caused by AI to existing revenue streams, such as Internet search.

Looking ahead: We are monitoring economic and policy developments that could impact cyclical market segments, such as the advertising ecosystem. We remain excited about long-term opportunities around secular trends such as AI, which we believe has the potential to be more pervasive and powerful than the broader market now expects. We also anticipate continued consolidation around the largest, digitally native platforms best equipped to attract both content and users.

Healthcare: Innovation rises above policy uncertainty

What happened: Healthcare stocks declined and lagged the broader market during the second quarter, pressured by policy uncertainty such as potential drug pricing reform and pharmaceutical tariffs. The appointment of Vinay Prasad to head the Food and Drug Administration’s (FDA) Center for Biologics Evaluation and Research was another source of uncertainty (Prasad is a well-known critic of the pharma industry). Healthcare services were dragged down by negative news from industry leader UnitedHealth Group following a surprise earnings miss and guidance cut. On a more positive note, the quarter saw some improvement in merger and acquisition activity. Among deals announced, Sanofi said it would acquire Blueprint Medicines for more than $9 billion, and Eli Lilly agreed to buy gene-editing firm Verve Therapeutics for up to $1.3 billion.

Looking ahead: If there’s one upside to the drumbeat of negative news, it’s that the healthcare sector now trades at a price-to-earnings ratio relative to the S&P 500® Index that is nearly two standard deviations lower than the long-term average. The FDA has also approved 26 drugs for the year through early July, ahead of the total this time last year. To us, that suggests innovation within the sector remains alive and well and may be had at a discount. As such, we remain focused on the small- and mid-cap biopharma companies driving medical advances but favor early commercial-stage companies with breakthrough products and late-stage development companies that we think are clinically derisked, given policy uncertainty. Medical device companies with new product cycles have also escaped political attention so far, while non-U.S. pharma with globally diversified revenue streams could be well positioned. Finally, we remain positive on leading health insurers and drug distributors. These companies are integral to the administration of healthcare in the U.S. and could be more insulated from recent tariff and drug pricing proposals.

Industrials: On the lookout for stable growth and self-help stories

What happened: Industrials stocks extended their strong year-to-date performance in the second quarter, outperforming the broader market. Tariff impacts were more muted than feared, due in part to the pause in levies and company cost and price management. Many firms also built up inventories in anticipation of tariffs, which may have pulled some demand forward. Companies ended the quarter with greater clarity around government tax policies, spending plans, and efforts to prioritize domestic production.

Looking ahead: We are closely following developments around tariffs, geopolitical stability, and consumer and business confidence as we look for signs of any resurgence in the broader industrial sector and in end markets such as freight. We continue to prioritize companies with exposure to strong secular themes, such as commercial aerospace and electrification. While stock multiples for such companies have seen some expansion, we remain excited about strong revenue growth potential that may flow through to higher margins and profits. Given lingering economic uncertainty, we also favor companies making operational improvements or that are exposed to unique catalysts that may drive stable profit growth even in uncertain times.

Financials: A strong setup thanks to positive cyclical and secular trends

What happened: Financials stocks rose along with broader equities, supported by relatively stable employment and consumer spending growth. Worries over tariffs and geopolitics eased, leading to improved investor sentiment. Key economic variables, such as unemployment and consumer spending growth, were relatively stable.

Looking ahead: We believe the global financial services sector offers a rich landscape in which to deploy deep fundamental research. Favorable cyclical trends, including relatively low levels of credit losses and delinquencies, exist across many areas of the global financials market. Pricing for property and casualty insurance appears attractive, in our view, and interest rates remain well above zero in most major markets. We are excited about secular trends, such as growth in electronic payments, and the advantages for companies leveraging proprietary data and advanced technological capabilities. We also continue to like the outlook for European banks, many of which, in our view, are positioned to benefit from significant capital return, an improved regulatory backdrop, and potential industry consolidation.

Consumer: Emphasizing company fundamentals amid potential macro headwinds

What happened: Consumer stocks rose in line with the broader market, as investors shook off their first-quarter caution and worst-case fears around tariffs. Consumer confidence improved, and we saw a relatively healthy pace of retail sales growth and personal consumption expenditures.

Looking ahead: While we have welcomed the resilience in consumer spending, we have seen some clouds on the horizon. These include slowing employment growth and the potential strain of tariff-related price increases. Given these risks, we continue to pay close attention to the quality and resilience of business models. That includes a mix of cyclical and defensive businesses, consistent with our philosophy of avoiding implied macroeconomic bets, as well as companies on the right side of digital disruption, a long-term theme that has shown no sign of abating. Market volatility can also create opportunities to deploy bottom-up stock and take advantage of attractive valuations.

Energy & Utilities: A defensive approach to market crosscurrents

What happened: Energy stocks materially underperformed the broader market in the second quarter, as tariff concerns increased global economic uncertainty. The weakness in energy stocks was broad-based, with the largest declines in shares of oil services companies and upstream producers with higher debt levels. The price of oil was volatile but averaged $67 per barrel for Brent crude, a level we believe supports solid returns for most energy companies.

Looking ahead: We remain defensive given our view that oil prices may continue to be volatile, if not range-bound. Despite the potential for short-term price spikes on geopolitical concerns, we see greater risk of a downward move in oil prices as a result of weaker global demand. OPEC+ countries have also announced further production increases, which could add to supply. And while at current prices we do not expect substantial increases in U.S. production, the Trump administration remains focused on lowering oil prices, either by incentivizing incremental supply or through policies to reduce demand. Longer term, we also recognize that China’s drive toward electrification and oil independence could put downward pressure on demand and pricing in the global energy market. Given market uncertainties, we think integrated oil, midstream, and large, diversified exploration and production companies could offer the most attractive balance of reward/risk.

IMPORTANT INFORMATION

Consumer discretionary industries can be significantly affected by the performance of the overall economy, interest rates, competition, consumer confidence and spending, and changes in demographics and consumer tastes.

Consumer staples industries can be significantly affected by demographics and product trends, competitive pricing, food fads, marketing campaigns, environmental factors, and government regulation, the performance of the overall economy, interest rates, and consumer confidence.

Energy industries can be significantly affected by fluctuations in energy prices and supply and demand of fuels, conservation, the success of exploration projects, and tax and other government regulations.

Financials industries can be significantly affected by extensive government regulation, subject to relatively rapid change due to increasingly blurred distinctions between service segments, and significantly affected by availability and cost of capital funds, changes in interest rates, the rate of corporate and consumer debt defaults, and price competition.

Health care industries are subject to government regulation and reimbursement rates, as well as government approval of products and services, which could have a significant effect on price and availability, and can be significantly affected by rapid obsolescence and patent expirations.

Technology industries can be significantly affected by obsolescence of existing technology, short product cycles, falling prices and profits, competition from new market entrants, and general economic conditions. A concentrated investment in a single industry could be more volatile than the performance of less concentrated investments and the market as a whole.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

The opinions and views expressed are as of the date published and are subject to change. They are for information purposes only and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. No forecasts can be guaranteed. Opinions and examples are meant as an illustration of broader themes, are not an indication of trading intent and may not reflect the views of others in the organization. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. Janus Henderson Group plc through its subsidiaries may manage investment products with a financial interest in securities mentioned herein and any comments should not be construed as a reflection on the past or future profitability. There is no guarantee that the information supplied is accurate, complete, or timely, nor are there any warranties with regards to the results obtained from its use. Past performance is no guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All