July 2025 Monthly Market Update

-

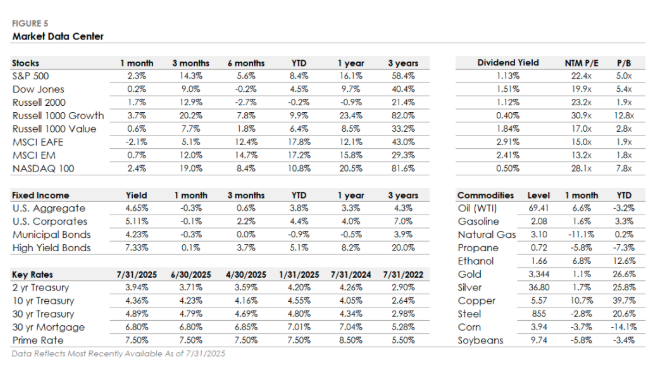

Stocks: Markets powered higher in July, with the S&P 500 rising 2.3% in July and pushing its year-to-date growth to 8.4%.

-

Mega-cap tech earnings, trade deals, and low volatility fueled the stock market surge. The Nasdaq and S&P both hit six straight record closes at month-end as growth continued to outperform value.

-

International Stocks: International equities underperformed the S&P 500 as the U.S. dollar strengthened. Developed Markets fell 2.1%, while Emerging Markets increased by 0.7%.

-

Bonds: Bonds remained under pressure and ended the month with a slight loss as Treasury yields rose. The US Bond Aggregate posted a decline of 0.3%.

Tech Leads, Again (With Some Help from Trade Agreements)

A familiar narrative returned in July – large-cap tech driving stock markets to new all-time highs. The S&P 500 and Nasdaq both logged six consecutive record closes late in the month. The “Magnificent 7” drove most of the returns in July (again), surging more than 5% as major AI-related companies reported strong results. Smaller companies briefly outperformed early in the month, but that reversed quickly by month-end.

In addition, markets responded positively to new trade agreements with Japan and the European Union. While the tariffs were less aggressive than anticipated, the effective U.S. tariff rate is still rising, putting long-term pressure on input costs, margins, and potentially inflation. For now, optimism from deal announcements continues to outweigh the risks, but the market may be underestimating the long-run economic effects of more protectionist policy. In addition, stagflationary concerns loom as the full impact of tariffs remains to be seen.

Market Valuations Back in Focus

This top-heavy dynamic continues to stretch market valuations. The S&P 500 now trades at over 22x forward earnings, well above the 16.8x long-term average and up sharply from 18x in April. With multiples elevated, future returns will depend more heavily on continued earnings growth.

Interest Rate Cuts on Hold, Again

After cutting interest rates by a full percentage point in late 2024, the Fed has held interest rates steady for five consecutive meetings. The reason? In our view it’s twofold:

- Core inflation has stalled around 3%, and

- The labor market remains resilient with unemployment near 4%.

While the market once expected rate cuts as early as March, those expectations have been continually pushed forward – first to May, then June, and now (maybe) September. Following the July Fed meeting, the probability of a September cut fell below 50%. Current consensus now calls for a single cut in October, followed by another in January 2026.

In our view, as long as inflation progress remains sticky and tariffs introduce new risks, the Fed will remain cautious. Policymakers have consistently emphasized the need for patience while they wait for more clarity in the data, and we have no reason to think different (at while Powell is in charge).

At Defiant Capital Group, we remain focused on positioning portfolios for resilience. Extended markets, unclear policy, and top-heavy leadership all demand caution and discipline.

This is not the time to chase headlines. It’s the time to sharpen focus.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Disclosures

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

The views and opinions expressed are for informational and educational purposes only as of the date of production/writing and may change without notice at any time based on numerous factors, such as market or other conditions, legal and regulatory developments, additional risks and uncertainties and may not come to pass. This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of market returns, and proposed or expected portfolio composition. Any changes to assumptions that may have been made in preparing this material could have a material impact on the information presented herein by way of example. Past performance is no guarantee of future results. Investing involves risk; principal loss is possible.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

A word on risk

All investments carry a certain degree of risk, including possible loss of principal, and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non-U.S. investments involve risks such as currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. This report should not be regarded by the recipients as a substitute for the exercise of their own judgment. It is important to review your investment objectives, risk tolerance and liquidity needs before choosing an investment style or manager.

Case Studies

Case studies and examples are hypothetical and do not involve any actual Defiant Capital Group clients.

© Defiant Capital Group

Read more commentaries by Defiant Capital Group