Wall Street Shrugs Off Tariff Panic as Buybacks Hit All-Time High

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits“Tariffs are back. The consumer is struggling. August is historically the worst month for stocks.”

You’ve probably seen versions of these headlines this summer. They’re all designed to grab your attention by sounding the alarm, then close with a hand-wringing quote from someone who probably missed the last bull run.

But here’s a rule I live by: Follow the trend lines, not the headlines.

Because if you look past the fearmongering and focus on the data, you’ll find that the market is humming with strength, and investors should take note.

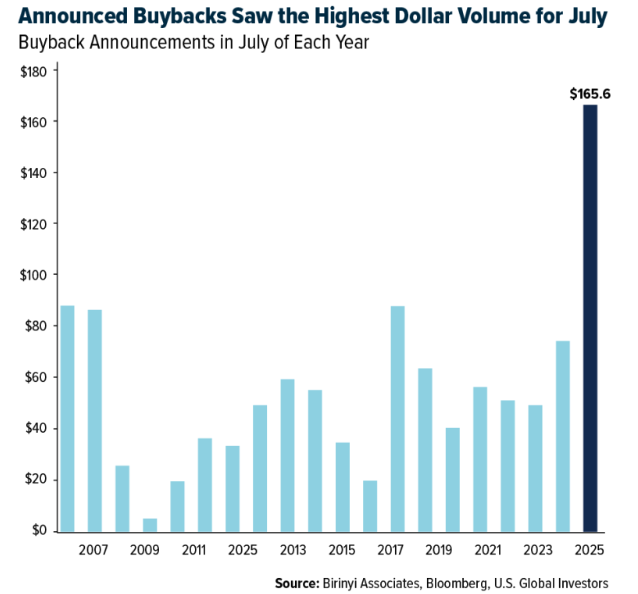

Buybacks Are Booming

Let’s start with stock buybacks. Companies don’t spend money repurchasing shares unless they believe their stock is undervalued or, at the very least, a better use of capital than sitting in the bank.

In July alone, U.S. companies announced a record $166 billion in stock buybacks. That’s the biggest amount recorded in July, more than double the previous record set in 2006.

Year-to-date, buyback announcements total nearly $926 billion, putting us well ahead of the previous record pace. Who’s leading the charge? Financial and tech giants, flush with cash and optimistic that the market will reward them long-term.

Now, some might point out that buybacks peaked earlier this year. That’s true. They’ve come down slightly from Q1 highs, but they’re still running at a historically high level, and that’s what matters.

The IPO Market Is Back

Next, let’s talk about initial public offerings (IPOs). After a few quiet years, the IPO engine looks to be roaring again, a good sign of investor demand.

As of this week, we’ve seen 204 IPOs so far in 2025, up more than 80% from this point last year. Even better, the quality of IPOs is improving. Unlike the SPAC frenzy from 2021, today’s IPOs are rooted in growth and profitability.

The second quarter alone saw $15 billion raised across 59 IPOs, a 34% increase from Q1. With global IPO activity being more mixed, the U.S. is clearly leading the pack.

If markets were truly on the verge of collapse, would we be seeing this kind of investor appetite for new equities? Would billion-dollar startups be going public?

Again, the trend line speaks volumes. Don’t let the media tell you otherwise.

The Smart Money Is Still Investing (in ETFs)

Meanwhile, retail and institutional investors alike are pouring money into ETFs. U.S. ETF assets came close to hitting $12 trillion last month, with $116 billion in inflows alone.

Active ETFs brought in a record $44.8 billion in July, the highest ever recorded. That tells me that more investors are looking for targeted, actively managed exposure to key themes, whether that’s defense, gold, energy or AI.

In fact, active ETFs now make up nearly 10% of the entire ETF market, up from less than 1% just 15 years ago, according to Morningstar.

Strong Earnings, Even Stronger Trends

Want more proof that the market isn’t buying into the doom-and-gloom narrative? Take a look at corporate earnings.

Around two-thirds of S&P 500 companies have reported Q2 earnings, and of those, more than 80% have beaten earnings expectations. That’s not just above the five-year average—it’s the highest beat rate since 2021. In the AI-fueled tech sector, over 90% of companies have posted better-than-expected results.

As for the third quarter, FactSet analysts raised their earnings per share (EPS) estimates, despite the persistent macro headwinds.

Tariffs Are a Drag, But Let’s See How They Play Out

Speaking of headwinds: Tariffs are back, and they’re not insignificant.

The average effective U.S. tariff rate has hit 18.3%, the highest level since the Great Depression. It’s already impacting prices, with economists estimating a 1.8% increase in consumer prices and a potential $2,400 annual hit to the average household, according to Yale’s Budget Lab.

But here’s the thing: Markets have a way of adjusting. Companies shift supply chains. Consumers find substitutes. Tariffs are friction, but I don’t think they have to be fatal.

In fact, some sectors could benefit from reshoring and industrial reinvestment. And let’s not forget that these tariffs were telegraphed well in advance, and markets had time to front-run the changes.

I’m not dismissing the risk. I’m reminding you to watch how markets react, not just how journalists report.

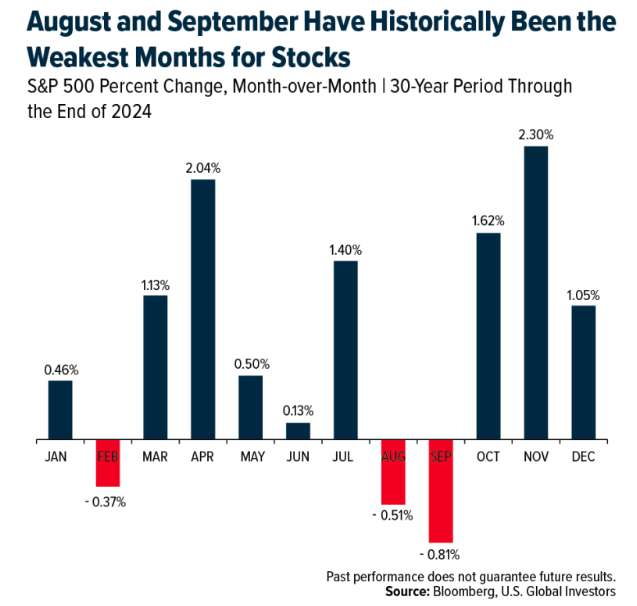

Seasonal Volatility Is Just That—Seasonal

Lastly, a word on seasonality.

Yes, August and September are historically choppy months for stocks. Average returns tend to be weaker, and lower liquidity during the summer means volatility can spike on any bad headline.

The question every long-term investor should ask is: Even if you knew the market would drop 10% next month, would you sell today?

Probably not. Because you’d risk missing the recovery, and you’d likely pay taxes to boot.

Keep in mind that the S&P 500 rose 26% in 2023, and another 25% in 2024. It’s up between 8% and 9% so far in 2025. That’s what long-term compounding looks like.

Trying to avoid every dip and pullback is a fool’s errand. Staying invested—and staying disciplined—beats timing the market almost every time.

Block Out the Noise

It’s easy to feel overwhelmed by negative headlines. That’s their job—to get clicks and sell ads.

As investors, our job is to look at the data, not the drama.

So, here’s what the data is saying:

Corporations are confident—just look at buybacks.

Capital markets are thriving—just look at IPOs.

Investors are engaged—just look at ETF flows.

Companies are executing—just look at earnings.

Yes, there are risks. There always are. But the underlying trends, as I see them, show resilience and strength.

So, ignore the headlines. Follow the trend lines.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.35%. The S&P 500 Stock Index rose 2.43%, while the Nasdaq Composite climbed 3.87%. The Russell 2000 small capitalization index gained 2.38% this week.

- The Hang Seng Composite gained 2.04% this week; while Taiwan was up 2.50% and the KOSPI rose 2.90%.

- The 10-year Treasury bond yield rose 7 basis points to 4.28%.

Airlines and Shipping

Strengths

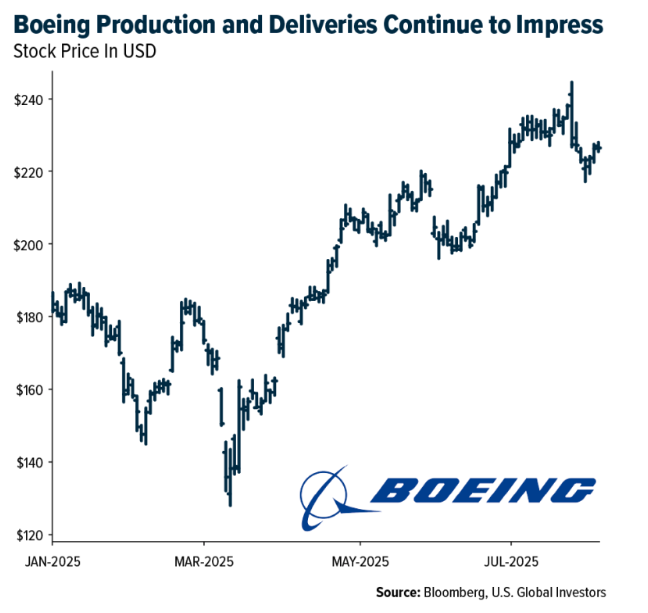

- The best performing airline stock for the week was Tripadvisor, up 10.9%. Boeing is tracking 47 deliveries for July, including 37 737 MAX and seven 787. Of the 37 MAX deliveries, Goldman estimates 32 were new production, with five being from inventory.

- Maersk released second-quarter 2025 results, with second-quarter EBITDA of $2.3 billion, ahead of Bloomberg/Visible Alpha consensus data at $2 billion, driven by higher container shipping revenues. As Goldman noted in their second-quarter preview, the company is also narrowing its full-year guidance to $8–9 billion (from $6–9 billion).

- Turkish Airlines posted solid results, exceeding consensus by 8% on EBITDA, with earnings 5% above the company-compiled consensus. The key highlight is the resilience in profitability despite weak cargo revenues and modest passenger growth, leading to a 1.2-point expansion in the EBITDAR margin to 25.4%, according to JP Morgan.

Weaknesses

- The worst-performing airline stock for the week was Sabre, down 35.7%. United’s flight attendants rejected the contract offer, with 71% voting against it. The agreement was set to offer a 40% gain in total economic improvements in its first year, according to Raymond James.

- Vessels from China to the United States dropped sequentially by 15%, marking a step-up in the rate of deceleration following the roughly four-week surge from China, according to Goldman. Container rates were flat sequentially; however, rates remain under considerable pressure on a year-over-year basis, down 66%.

- Frontier’s second-quarter 2025 earnings per share (EPS) result and third-quarter 2025 EPS guidance fell short of expectations. While the second-quarter miss was primarily driven by weaker revenue and the third-quarter guidance is below expectations, Raymond James estimates that the guide implies a year-over-year RASM inflection from (2)% to 0–2%, supported by both internal initiatives and an anticipated improvement in the domestic supply-and-demand balance.

Opportunities

- Travel categories continue to be top spending priorities, behind only essential categories (groceries and home supplies), as all travel categories have remained above auto and vehicle supply spending, according to Morgan Stanley.

- Asia to North Europe route prices began increasing sequentially at the end of fMay. Over the past four weeks, rates have remained broadly flat, with this week marking the first time quotes suggest a high single-digit decline. Historically, between 2012 and 2019, UBS notes that rates from Asia to Europe have, on average, increased sequentially in August compared to July.

- Delta management remains constructive on both the demand uptick that began about a month ago and the forward supply outlook. Regarding the latter, domestic industry capacity is currently expected to be down year-over-year through October, as previously communicated cuts have unfolded as expected, according to Goldman.

Threats

- Spirit Airlines will furlough 270 pilots and demote over 100 others as it prepares to cut flights. This follows previous pilot furlough announcements in September 2024 and January 2025, according to Raymond James.

- Deutsche Post AG maintained its full-year 2025 EBIT guidance of at least €6 billion, with the caveat that it excludes any further escalation in tariffs or trade policies. Management noted that the recently announced Trump executive order to remove the de minimis exemption for the rest of the world could have up to a €200 million impact on EBIT if implemented, according to Bank of America.

- As reported by RBC, Airbus delivered 54 A320 family aircraft (19 A320neos and 35 A321neos), 5 A220s, 2 A330s, and 6 A350s. The 373 commercial deliveries year-to-date are down 7% year-over-year, underscoring the production ramp Airbus will need for the remainder of 2025 to meet its guidance of 820 aircraft. To achieve that target, the company must deliver an average of 89 aircraft per month from August through December.

Luxury Goods and International Markets

Strengths

- Lifetime Group Holdings reported stronger-than-expected second-quarter 2025 results, with earnings per share of $0.37 surpassing the forecast of $0.32 and revenue reaching $761.5 million—a 14% year-over-year increase. This robust performance was driven by higher net income and strong operational momentum, prompting the company to raise its full-year outlook.

- Hugo Boss reported a second-quarter earnings beat, with operating profit (EBIT) rising 15% to €81 million, exceeding the consensus estimate of €77 million. The company confirmed and maintained its full-year 2025 outlook without any changes.

- The RealReal, an online retail platform, was the top performer in the S&P Global Luxury Index, surging 27.7% after reporting better-than-expected results.

Weaknesses

- Ralph Lauren’s (RL) share price fell sharply by about 7.4% on August 7, 2025, dropping around $22.52 to close near $280, down from the previous close of $303. This decline occurred despite the company reporting a strong quarter in which sales exceeded Wall Street expectations and raising its full-year revenue outlook. The main driver of the share price drop was the company’s cautious outlook for the second half of 2025.

- Last Friday, U.S. employment data indicated a slowdown in hiring, signaling potential softening in the broader economy. This week, the ISM Services Index fell to 50.1 in July, down from 50.8 in June and below Bloomberg’s forecast of 51.5.

- Lucid Group, the electric vehicle manufacturer, was the worst-performing stock in the S&P Global Luxury Index, falling 12.0% after reporting weaker financial results.

Opportunities

- As of August 7, the U.S. raised tariffs on luxury goods to 15%, but luxury brands like LVMH, Hermès, and Kering still saw their stocks rise. These companies have strong brand equity and can pass on some of the tariff costs to wealthy customers through modest price increases—about 2% on average. Additionally, Hermès and LVMH reported strong revenue growth this quarter and undertook share buybacks, signaling confidence in their businesses.

- Tesla is expanding its Robotaxi program to New York, initially focusing on Brooklyn. The company is actively hiring drivers and operators in the area as part of a broader plan to roll out its autonomous ride-hailing service to multiple new cities across the U.S. This expansion reflects Tesla’s rapid scaling ambitions following successful launches in Austin and the San Francisco Bay Area.

- The Wine Union (WU) in the Eurozone is actively working to negotiate with the U.S. government for an exemption from the recently imposed 15% tariffs on European wine and spirit exports. Despite the new trade deal that introduced these tariffs, negotiations are ongoing to reduce or eliminate them, as the wine and spirits sectors face significant economic pressure. Both European and American industry groups are advocating for a “zero-for-zero” tariff agreement to protect jobs and maintain competitiveness in the U.S. market.

Threats

- Lucid Motors and Rivian both missed second-quarter 2025 earnings expectations. Lucid reported a loss of $0.24 per share vs. the expected $0.22 loss, with revenue of $259.4 million also falling short. Despite higher vehicle production and deliveries year-over-year, Lucid’s gross margin remained deeply negative due to cost pressures. Rivian’s weak results reflected ongoing challenges from policy shifts, trade tensions, and a difficult EV market.

- Next week, several key economic data releases will draw attention, including the U.S. Consumer Price Index (CPI), Producer Price Index (PPI), and Retail Sales, as well as GDP figures from the European Union and Japan—critical markets for luxury spending. The Empire State Manufacturing Index is also due. With ongoing trade tensions, inflation remains in focus, as higher prices could reduce consumer purchasing power.

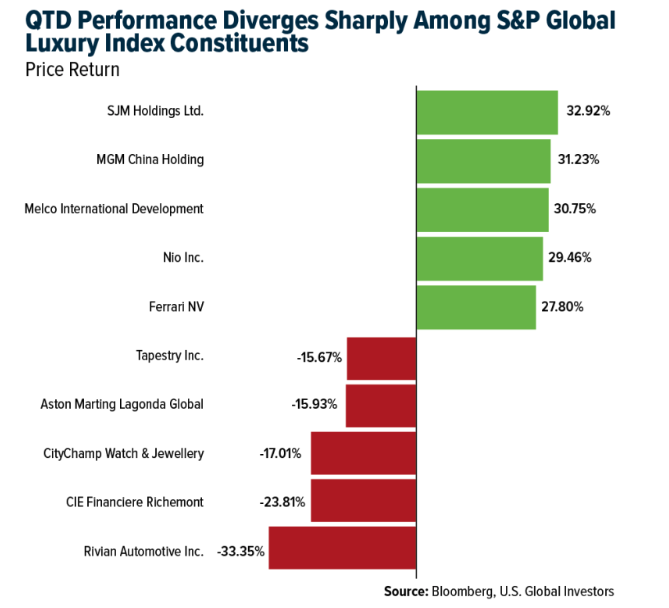

- Quarter-to-date in Switzerland, luxury stocks (members of the S&P Global Luxury Index) have shown significant volatility due to macroeconomic pressures and tariff concerns, creating clear winners and losers within the sector. Some investors are concerned about limited visibility for recovery, with stocks likely to continue trading with elevated volatility.

Energy and Natural Resources

Strengths

- The best-performing commodity for the week was coffee, rising 8.97%. Coffee futures rallied as hedgers and traders responded to a weakening supply chain pressured by tariffs. Brazilian producers have also been reluctant to sell beans and have increased their activity in the futures market to hedge against tariff uncertainty, Bloomberg reports.

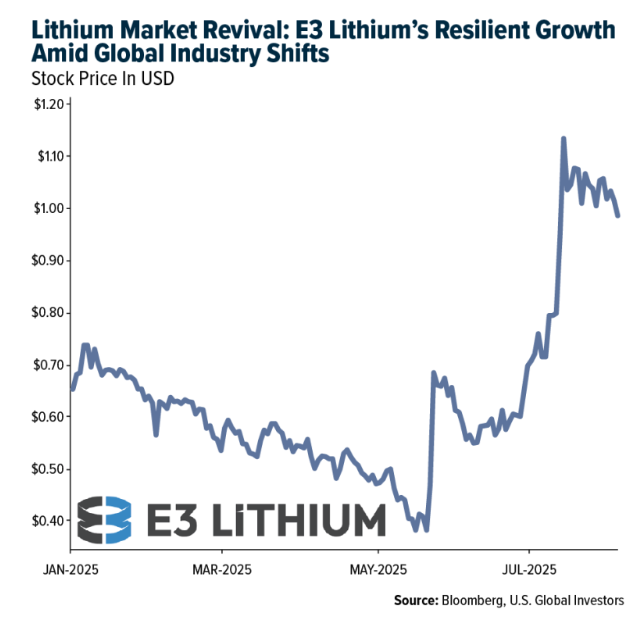

- The lithium market is rebounding, driven by rising EV demand, tighter supply expectations, and renewed investor interest. E3 Lithium, with its direct extraction technology and large Alberta resource, is well-positioned as it advances toward commercial production and continues successful drilling.

- The stark divergence between NuScale’s post-earnings sell-off and GE Vernova’s rally highlights that, within the bullish nuclear theme, tangible results matter more than hype. While NuScale remains in a high-cost, pre-revenue phase and saw its valuation decline after missing expectations, GE Vernova continues to deliver solid earnings, reinforcing investor confidence through execution rather than speculation.

Weaknesses

- The worst-performing commodity for the week was crude oil, falling 5.53%. Prices declined on expectations of an economic hit from new tariffs and concerns over a looming supply surplus, which could be worsened if OPEC+ proceeds with another outsized output hike in September.

- Saudi Aramco’s second-quarter net income fell 19% to $22.8 billion, missing analyst estimates. Free cash flow of $15.2 billion was insufficient to cover the dividend, while net debt rose to $30.8 billion. The company also guided for continued pressure from weaker prices and lower production volumes. The quarterly dividend totaled $21.36 billion—down from $31 billion a year earlier—as the performance-linked portion was reduced amid oil prices averaging nearly $20 per barrel lower.

- Resolution Copper, a Rio Tinto–BHP joint venture with reserves sufficient to meet a quarter of U.S. copper demand, has spent over two decades and $2 billion without producing due to permitting, legal, and tribal disputes. Despite some recent regulatory progress, production isn’t expected until the 2030s—highlighting the long timelines and high costs facing major U.S. mining projects.

Opportunities

- BP’s largest oil and gas discovery in 25 years—a 500-meter column off Brazil’s Santos Basin—could boost its exploration portfolio and extend upstream production into the 2030s. However, high CO₂ levels pose development challenges, and investor concerns over recent underperformance and strategic shifts led to a muted market reaction.

- Nutrien is facing rising unit costs and weaker crop prices, with shares trading at a 17% discount to Morningstar’s $70 fair value estimate. While near-term earnings are pressured, Morningstar expects modest revenue and profit growth through 2029 as fertilizer markets stabilize.

- Resolution Copper, a Rio Tinto–BHP joint venture, holds an estimated 28 million metric tons of copper—enough to meet a quarter of U.S. demand. After 20 years and $2 billion spent, the project is gaining momentum as the Trump administration aims to fast-track permitting by 2026, potentially enabling production in the 2030s and strengthening the U.S. industrial base amid rising global copper demand.

Threats

- Despite U.S. pressure and threats of sanctions, Indian refineries continue to receive Russian crude, with several tankers unloading millions of barrels of Urals and other grades over the weekend. India’s ongoing purchases—backed by long-term agreements and made despite geopolitical scrutiny—underscore its role as the largest importer of Russian seaborne oil, even as U.S. efforts to curb these supplies escalate.

- China defended its rising imports of Russian oil, which reached $10.06 billion in July, calling them “legitimate and lawful” despite U.S. threats of new tariffs. The comments come as President Trump signaled that additional duties “may happen,” with negotiations to extend the current U.S.-China tariff truce approaching a critical deadline.

- Glencore has scrapped plans to move its primary listing from London, citing the challenges of entering the S&P 500 and weak sector valuations. The company continues to face falling coal and copper prices, reporting a 14% drop in core earnings and implementing $1 billion in cost cuts amid broader industry headwinds.

Bitcoin and Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Mantle, rising 53.02%.

- Fundstrat co-founder Tom Lee predicts that Ethereum may eventually overtake Bitcoin due to its broader use cases, particularly on Wall Street. In an appearance on the Bankless podcast on August 6, Lee suggested Ethereum could deliver a 100x return and potentially surpass Bitcoin’s market cap, driven by accelerating institutional adoption and Ethereum’s central role in blockchain infrastructure, according to Bloomberg.

- President Donald Trump is expected to sign an executive order allowing private equity, real estate, cryptocurrency, and other alternative assets to be included in 401(k) retirement plans. The order will direct the Labor Department to reevaluate current guidance on alternative investments and clarify the government’s stance on fiduciary responsibilities, Bloomberg reports.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Monero, down 9.92%.

- China has instructed local brokers and other organizations to stop publishing research or holding seminars that promote stablecoins, in an effort to rein in the asset class and prevent financial instability. Regulators are concerned that stablecoins could be exploited as a tool for fraudulent activity in mainland China, according to Bloomberg.

- Michael Novogratz believes the rush to create companies that hold cryptocurrencies on their balance sheets has likely peaked. He expects existing crypto treasury companies—such as those holding Ethereum—to continue expanding, while new entrants may face greater difficulty gaining traction, Bloomberg reports.

Opportunities

- The Winklevoss twins have invested in American Bitcoin Corp, a crypto-mining venture linked to Eric Trump and Donald Trump Jr. The investment was made through a private placement described as “oversubscribed” by Asher Genoot, and the twins used Bitcoin to fund their investment, Bloomberg reports.

- Nomura’s crypto division has received regulatory approval in Dubai to offer institutional over-the-counter crypto options, expanding the UAE’s presence in global digital derivatives. Laser Digital, the digital asset subsidiary of Japan’s investment bank Nomura, has become the first company licensed under Dubai’s Virtual Asset Regulatory Authority, according to Bloomberg.

- WhiteFiber, an AI infrastructure firm, raised $159.4 million in its IPO, pricing shares at the top of the marketed range. The subsidiary of crypto treasury firm Bit Digital sold 9.4 million shares on Wednesday at $17 each, after marketing them between $15 and $17, Bloomberg writes.

Threats

- Roman Storm has been convicted. The U.S. Department of Justice stated he knowingly operated a crypto mixer that moved over $1 billion in criminal funds, including money from cyberattacks linked to North Korea, according to Bloomberg.

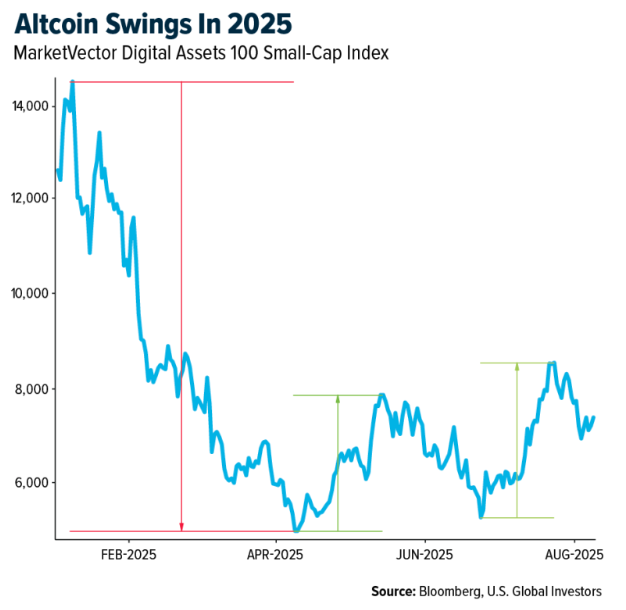

- Altcoins are notoriously volatile, increasing the risk of a vicious cycle of forced selling and plunging prices. An index of smaller tokens has already experienced three cycles of rising or falling more than 55% this year and is down about 15% since hitting a five-month high on July 22, Bloomberg reports.

- CZ asked a bankruptcy court to dismiss claims against him from an FTX trust seeking to claw back $1.76 billion. CZ argued that the trust and FTX Digital Markets cannot allege facts placing him “at home” under Delaware’s jurisdiction because he is a resident of the UAE. Zhao stated that the trust and FTX Digital Markets nonsensically blame him and Binance for SBF’s pervasive malfeasance and the collapse of the crypto exchange, according to Bloomberg.

Defense and Cybersecurity

Strengths

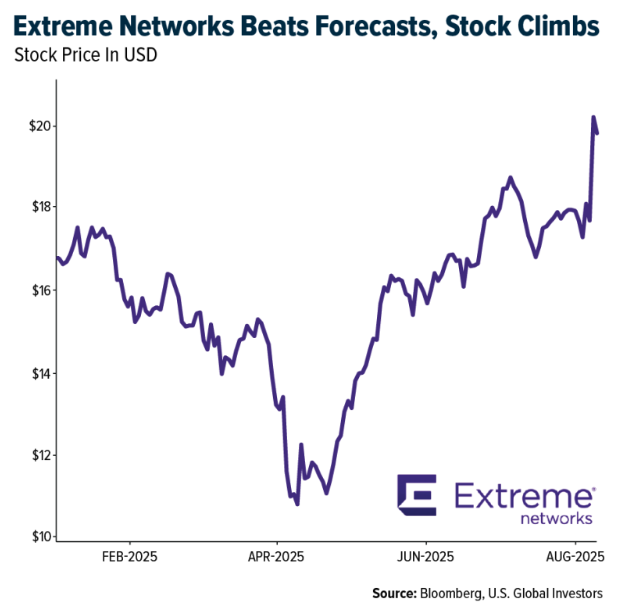

- Extreme Networks (EXTR) reported strong fourth-quarter fiscal year 2025 results, with earnings per share up 83 percent year-over-year to $0.25, revenue rising 19.6 percent to $307 million, and net income increasing 85.6 percent. Growth was driven by strong demand in cloud and enterprise segments. The company also noted continued momentum in its SaaS business, with annual recurring revenue up 24 percent year-over-year.

- Palantir delivered a strong quarter with 48 percent revenue growth year-over-year, driven by surging U.S. government and commercial AI demand, and raised its full-year outlook. Shares hit a new all-time high as adjusted earnings per share jumped 78 percent year-over-year, cementing Palantir’s position as a leading AI-enabled analytics provider in defense and enterprise markets.

- The best performing stock in the XAR ETF this week was BWX Technologies, climbing 19.86%, after raising its full-year revenue, adjusted EBITDA, and EPS guidance above estimates on strong second quarter results, prompting Truist to boost its price target.

Weaknesses

- Tokyo Electron reported first-quarter fiscal year 2026 revenue down 16.1 percent quarter-over-quarter and 1 percent year-over-year, with net income declining 17.6 percent quarter-over-quarter amid thinner margins and higher research and development costs. Sluggish semiconductor capital expenditures, especially in China’s logic chip segment, are pressuring short-term growth despite resilient demand for advanced AI tools.

- Fortinet plunged 23.2 percent, its worst drop since August 2023, after management revealed that the firewall refresh cycle is already 40 to 50 percent complete, undercutting a key growth narrative. While second-quarter earnings per share and billings beat estimates, investors reacted sharply to the reduced runway for product replacement-driven revenue gains.

- The worst performing stock in the XAR ETF this week was Redwire Corp, which declined 35.18%. The company posted a wider-than-expected second quarter loss, missing revenue estimates, and cutting its full-year sales guidance due to ongoing U.S. government budget approval delays.

Opportunities

- Onsemi’s EliteSiC technology was adopted in Xiaomi’s new YU7 EVs, enabling faster acceleration, longer range, and higher efficiency. This expands Onsemi’s electric vehicle footprint in China’s competitive market and showcases its leadership in power electronics.

- Broadcom launched its Jericho 4 chip, capable of linking over a million processors in AI data centers, completing its next-generation networking lineup. This move strengthens its position in high-bandwidth, low-latency infrastructure as AI workloads scale.

- Australia signed its largest-ever defense deal with Japan to purchase 11 Mogami-class stealth frigates for $6 billion, boosting its long-range naval firepower. The agreement deepens AUKUS and Quad security cooperation, creating opportunities for allied defense contractors.

Threats

- China blocked exports of critical rare earth minerals to Western defense contractors, threatening to disrupt U.S. defense production. Over 80,000 Pentagon parts depend on these materials, highlighting severe supply chain vulnerabilities.

- President Trump announced a 100% tariff on imported computer chips, exempting U.S. producers. This move could significantly disrupt global semiconductor supply chains, risking retaliatory measures and cost inflation for non-U.S. chipmakers serving the American market.

- China and Russia began joint naval drills near Vladivostok, practicing submarine rescue, air defense, and combat operations. The exercises signal a tightening military alignment between the two powers, directly opposing U.S. strategic interests.

Gold Market

This week gold futures closed at $3,456.10, up $56.30 per ounce, or 1.66%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 11.44%. The S&P/TSX Venture Index came in up 3.42%. The U.S. Trade-Weighted Dollar fell 0.89%.

Strengths

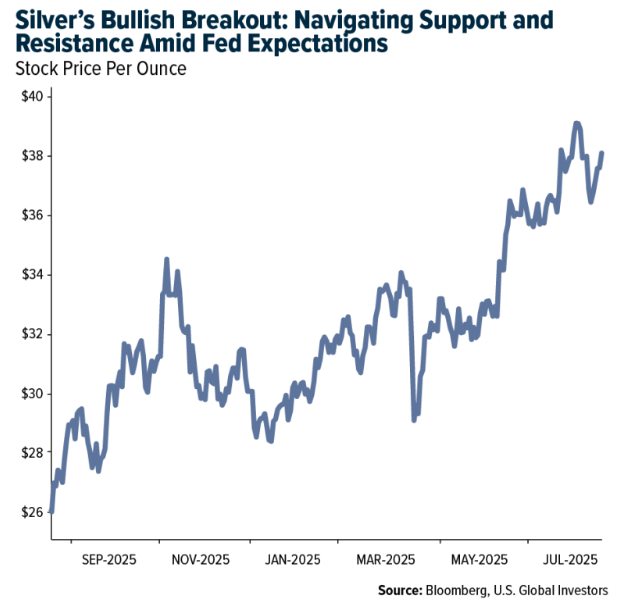

- The best performing precious metal for the week was silver, up 4.34%, snapping a three-week losing streak with six consecutive days of gains. The People’s Bank of China increased its gold reserve in July, marking nine straight months of purchases that are helping it diversify its holdings away from US dollars. Gold held by the central bank increased by 60,000 troy ounces to 73.96 million troy ounces last month, according to data released on Thursday.

- SSR Mining reported second-quarter 2025 results with adjusted earnings per share of $0.51, beating the consensus estimate of $0.23, according to Scotiabank. The company produced 120,200 ounces of gold at an all-in sustaining cost of $2,068 per ounce. The stock surged 17.32% on the earnings beat.

- OceanaGold reported second-quarter 2025 adjusted earnings per share of $0.51, beating both BMO’s and the consensus estimate of $0.41. The share price rose 10.23 percent on the day of the announcement. Gold production totaled 119,500 ounces, surpassing both BMO’s and the consensus estimate of 108,000 ounces. The all-in sustaining cost of $2,027 per ounce also beat expectations, which had been $2,380 per ounce.

Weaknesses

- The worst-performing precious metal for the week was palladium, down 6.74%. Precious metals refiner Heraeus noted that “China joins India in reducing gold jewelry consumption as prices remain high.” The Chinese Gold Association reported that total gold consumption declined 3.5% year-over-year in the first half of the year, to 505 tons. The largest drop was in the jewelry sector, which contracted 26% year-over-year to just under 200 tons.

- A gold miner with operations in Peru and Mongolia had to offer a higher yield and a considerably smaller bond than expected to complete its debut deal—signaling how selective investors have become in the sector. After a two-week marketing process, Singapore-registered Boroo Investments Pte. raised $300 million from its seven-year bond offering, well below the anticipated $500 million to $600 million, according to Bloomberg.

- Allied Gold reported adjusted earnings per share of $0.14, missing CIBC’s estimate of $0.24 and the consensus estimate of $0.29. The shortfall was driven by the timing of gold sales, higher operating costs, and a $17.2 million share-based expense. Allied Gold’s share price fell 11.91 percent on the news.

Opportunities

- Minera Alamos announced it is acquiring Calibre USA Holdings from Equinox Gold for total consideration of US$115 million, subject to adjustment. Calibre USA holds the Pan Gold Mine, Gold Rock Project, and Illipah Project, all located in Nevada, United States, according to Canaccord. The transaction is expected to be funded through a Subscription Receipt, which will convert upon closing into a share and a full share warrant to help sweeten the deal.

- Royal Gold announced that it has entered into a streaming agreement on First Quantum’s Kansanshi copper-gold mine in Zambia for an advance payment of $1.0 billion. Royal Gold expects to receive 12,500 ounces of gold in 2025, averaging 35,000 to 45,000 ounces annually over the next 10 years, with the mine life projected through 2049. This deal follows closely on the heels of Royal Gold’s recently announced acquisition of Sandstorm Gold Ltd. just a month ago.

- A years-long supply crunch in platinum has come to a head, with banks scrambling for dwindling stocks in London as buyers in China and the United States scoop up much of the available metal. The market tightness has made platinum one of the best-performing commodities this year and has fueled sky-high borrowing costs for the precious metal, according to Bloomberg.

Threats

- Royal Gold reported production 4% below consensus expectations, despite previously releasing stream production figures. According to RBC, the operator has revised 2025 targets for the Mt. Milligan mine lower due to ongoing grade challenges.

- The trade imbalances that prompted President Donald Trump to impose significant tariffs on Swiss imports are largely driven by a small but crucial industry at the heart of the global gold market. Switzerland is the world’s largest gold-refining hub, renowned for its quality and discretion. Billions of dollars’ worth of gold flows into and out of the country—from mines in South America and Africa to banks in London and New York—according to Bloomberg. There was initial confusion over whether imported physical gold bars would be subject to the new tariffs, but it now appears they are exempt.

- Following a reported pit wall failure at its Camino Rojo mine on July 23, Orla Mining has revised its 2025 guidance for the site to 95,000–105,000 ounces of gold production (down from 110,000–120,000 ounces) and raised the all-in sustaining cost (AISC) to $850–$950 per ounce from $700–$800. According to Scotiabank, this brings Orla’s full-year 2025 consolidated guidance to 265,000–285,000 ounces of production at an AISC of $1,350–$1,550 per ounce.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2025):

Boeing

AP Moller Maersk

United Airlines

Delta Air Lines

Airbus SE

Life Time Group Holdings

Hugo Boss

LVMH

Hermes

Kering

Tesla

E3 Lithium

BP PLC

Nutrien

Glencore

OceanaGold

Allied Gold

Calibre

Royal Gold

Orla Mining Ltd

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits