income environment certainly isn't immune to the cause and effects of tariff contagion permeating in the financial markets. Bonds can serve as an ideal ballast for a portfolio in times of market uncertainty. But when it comes to maximizing income, diversification is necessary considering that rate cuts could be on the horizon. One area that could help bridge the gap — private credit.

The Federal Reserve kept rates in check at its most recent meeting. But that obviously didn't move the needle in terms of earth-shattering news. That's especially the case given that it's been five consecutive times so far this year. What did cause a stir was the dissention among Fed members.

Dueling Fed Members

Behind closed doors, two Fed members pushed for rate cuts, while the rest opted to keep them intact. As indicated by Investors Observer, this is a notable departure from the norm. In particular, economist Wolf Richter said the last time Fed members dissented on a rate cut decision was 1993.

One of the dissenters, Michelle Bowman, recently said she could foresee a scenario in which three rate cuts are necessary before year's end. In combination with the bully pulpit by President Trump, the prospect of rate cuts appears inevitable. Moreover, a data-dependent Fed is already seeing indications a rate could could be forthcoming.

“Wage growth is coming down. We've seen the jobs number and consumer spending is cooling. All of that suggests the real underlying economy is slowing,” said Minneapolis Fed President Neel Kashkari. “That means in the near term, it may become appropriate to start adjusting the federal funds rate."

Consider Private Credit as Rate Cuts Loom

While the calls for rate cuts become more audible, fixed income investors who rely solely on bonds may want to seek additional options to support income lost from falling yields. Thankfully, there's a plethora of options available to them, from dividends to mortgage-backed securities, as well as a host of others. One area that's been generating a higher degree of interest as of late is private equity.

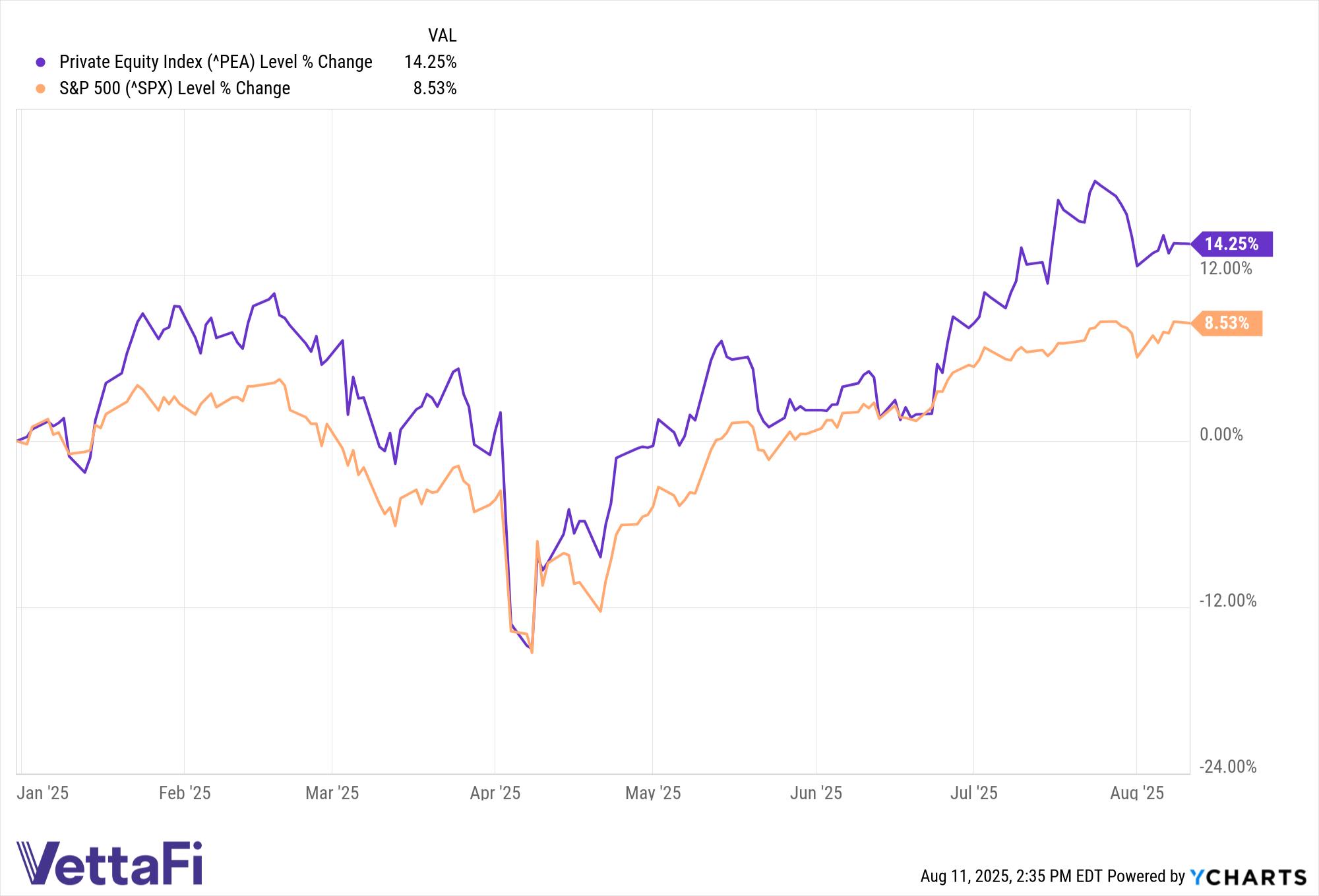

Once an arena only available to institutional and accredited investors (namely hedge funds and venture capitalists), access to private equity is becoming more public. Private equity is exactly what its name explicitly mentions — investments that don't offer publicly traded stock to investors. It opens up a realm of opportunities for retail investors. And the excitement is only amplified when looking at the side-by-side performances of the Private Equity Index and the S&P 500 this year.

^PEA data by YCharts

For fixed income investors, a derivation of private equity investing is private credit. At its most basic definition, they're essentially loans originated between a borrower and a nonbank lender. Private lenders are especially useful when borrowers are unable to obtain loans from traditional financial institutions that can carry stricter underwriting procedures.

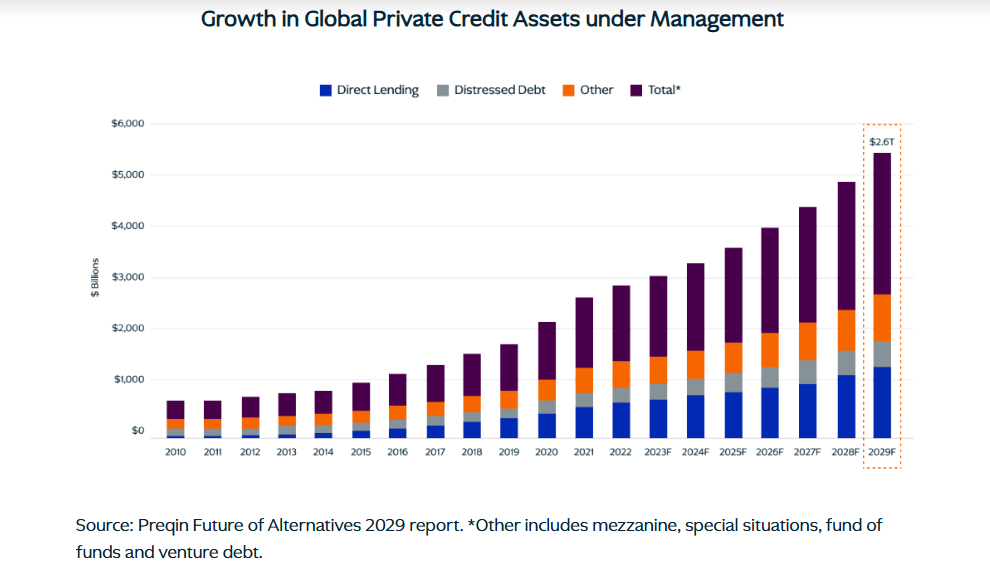

The growth of private credit is occurring at a massive scale, creating opportunities for fixed income investing. Global investment firm KKR referenced that the growth of private credit assets under management could hit $2.6 trillion by 2029 based on a Preqin Future of Alternatives 2029 report.

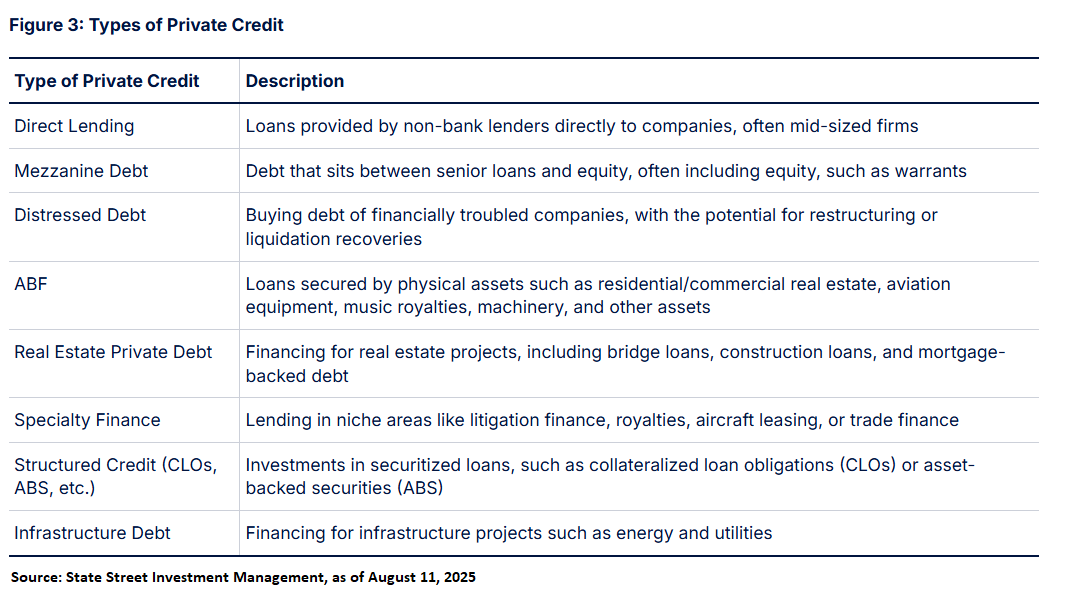

Furthermore, the options in private credit investing are seemingly endless. As seen below, State Street Investment Management outlined the variation in private credit options. That, again, speaks to the income diversification.

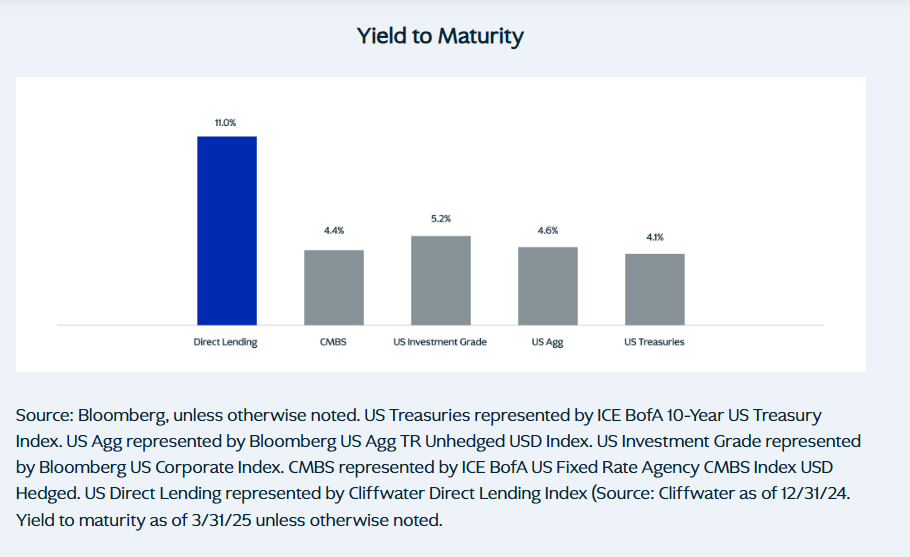

When it comes to fixed income investing, eyes will typically go to one thing — yields. Because nontraditional lenders are willing to front the money for investors who can't otherwise get a loan through traditional means, they'll want a premium. In turn, this typically translates to higher yields, as seen below.

Of course, private credit investing will carry its own nuances when compared to more traditional fixed income sources. Investors should always consult with their advisors before diving into these instruments to see how they can slot into a portfolio.

Private Credit ETFs

ETFs) have been a go-to investment vehicle when it comes to tapping into unchartered markets. That's why it's no surprise that funds have been sprouting in the ETF landscape that cater to private credit access.

Options in the burgeoning private credit ETF space include the SPDR SSGA IG Public & Private Credit ETF (PRIV). The fund is actively managed, following the trend of ETFs that are seeing a record number of active fund launches this year.

The private credit space can be a nuanced corner of the fixed income market. So this is where an actively managed fund can help. PRIV taps into the expertise of the SSGA Active Fixed Income Team that can deftly navigate the private credit market to maximize yield opportunities and mitigate risk. Because the fund includes both public and private credit of the investment-grade variety, that helps to temper credit risk. It also makes for an ideal option for those looking to dip their toes into private credit as opposed to diving in head first. With a 0.70% expense ratio, the fund's 30-day SEC yield is 4.46% as of August 13.

Another active option is the BondBloxx Private Credit CLO ETF (PCMM), which, as the fund name suggests, invests more heavily in collateralized loan obligations. It pairs a 0.68% expense ratio with a 30-day SEC yield of 7.4% as of July 31. That highlights the potential yield opportunities that private credit can bring.

For those seeking a passive ETF that tracks an index, take a look at the Virtus Private Credit Strategy ETF (VPC). By tracking the Indxx Private Credit Index, investors get exposure to myriad private credit opportunities. These include business development companies and closed-end funds. As of July 31, it comes with a hefty total expense ratio of 9.86% (0.75% management fee + 9.11% acquired fund fees and expenses). But with that, investors also get a 13.01% 30-day SEC yield.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our podcasts.

Read more commentaries by VettaFi