The July U.S. employment report included surprisingly large downward revisions to previous months' data, suggesting a downshift in economic activity during the first half of 2025. The extent to which this may lead to slower economic growth and interest rate cuts by the Federal Reserve in the months ahead remains to be seen. Meanwhile, international economic growth has remained resilient, with Europe—particularly Germany—a potential bright spot.

U.S. stocks and economy: Hitting a soft patch

No matter how one slices and dices it, U.S. economic growth slowed decisively in the first half of the year. Inflation-adjusted gross domestic product (GDP) grew at an average of 1.25%, consumer spending grew at an average of 0.95%, and private business investment grew at an average of 1.55%. All figures were notable downshifts from 2024, and while they're not yet consistent with prior recessions, they suggest that the economy has hit a soft patch—driven by policy uncertainty in both the trade and labor realms.

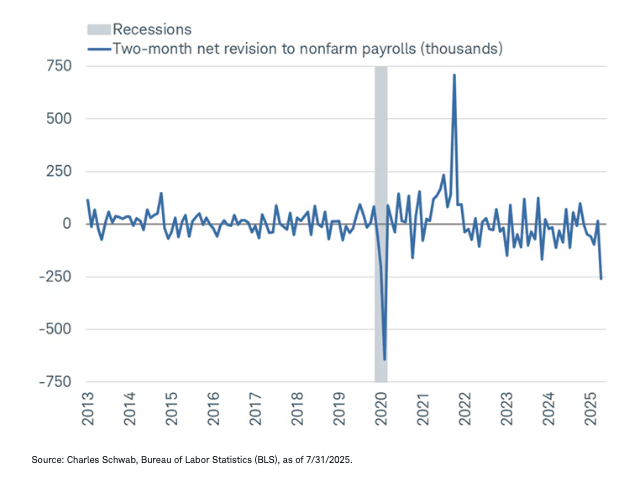

One of the most notable slowdowns has been in the labor market. July's jobs report stood out not only because of the 73,000 payrolls that were created (the consensus estimate per Bloomberg was for a gain of 100,000), but because payrolls for June and May were revised lower by a combined 258,000. As shown in the chart below, that was the largest two-month downward revision since the shutdown days of the COVID-19 pandemic.

May and June payrolls were revised sharply lower

It's important to emphasize that while the magnitude of the revisions stood out, it does not necessarily have nefarious implications. Revisions are a fact of life when it comes to data gathering and in the post-pandemic era, they have skewed larger (to the upside and downside) because of lower response rates for surveys like the BLS establishment survey, which measures nonfarm payrolls.

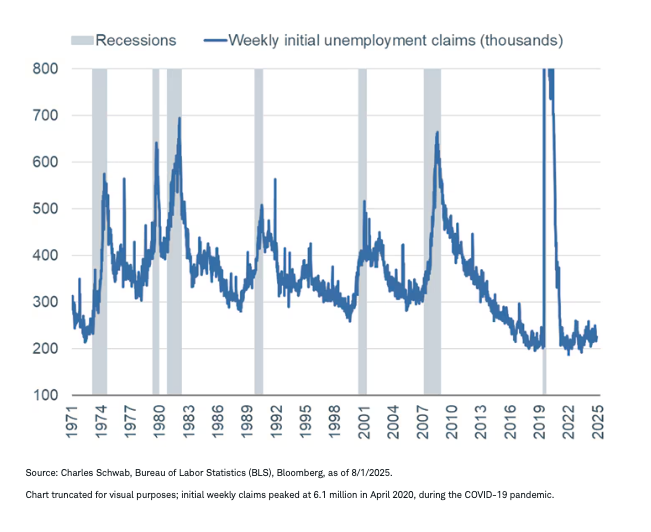

Another important factor to note is that labor supply and demand have been falling in tandem this year, which is a key reason that the economy has averaged job gains of 35,000 over the past three months while seeing a still-low unemployment rate of 4.2%. The important context is that the unemployment rate did rise to a cycle high in July, but the fact that it hasn't spiked is indicative of waning labor supply. Plus, layoff activity remains subdued, evidenced by initial jobless claims staying low relative to history.

Claims not yet suggestive of recession

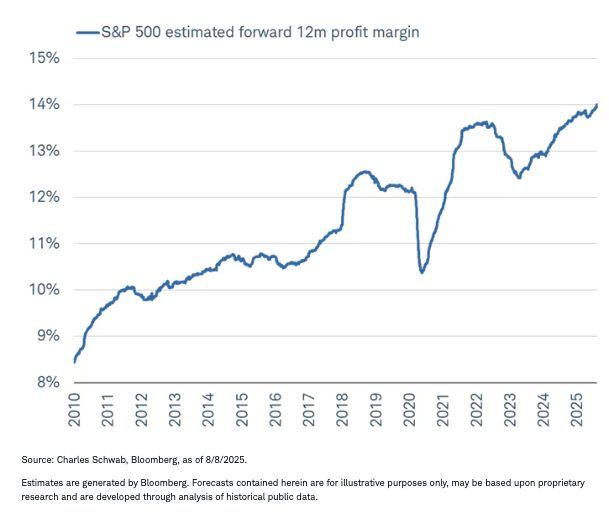

As for the stock market's response, while there was elevated volatility to the downside after the release of the July jobs report, it was relatively short-lived. The continued, sharp rebound off the early-April lows has seemed inconsistent with the fact that tariff rates have moved higher and job growth has slowed, but key to keep in mind is that corporate fundamentals have not been dented materially. In fact, the S&P 500's forward 12-month estimated profit margin has risen to a new all-time high. We think there is a bit too much optimism baked into those estimates, but for now, large companies have stomached the tariff pain and managed through higher input costs quite well.

Profit margin estimates unbothered and unscathed

Fixed income: Turning point

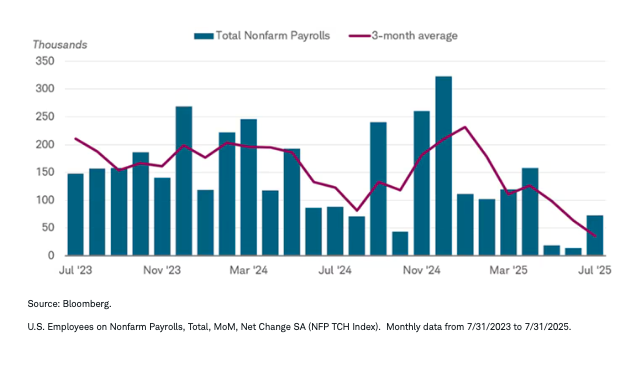

The recent July employment report marked a turning point for the fixed income markets. It signaled that the job market has stalled in recent months, raising the likelihood of slower economic growth and interest rate cuts by the Federal Reserve in the months ahead. As a result, Treasury yields have fallen for all maturities. The futures market is now discounting two to three rate cuts by the end of the year, starting with the September meeting of the Federal Reserve's Open Market Committee (FOMC).

The job market has stalled in recent months

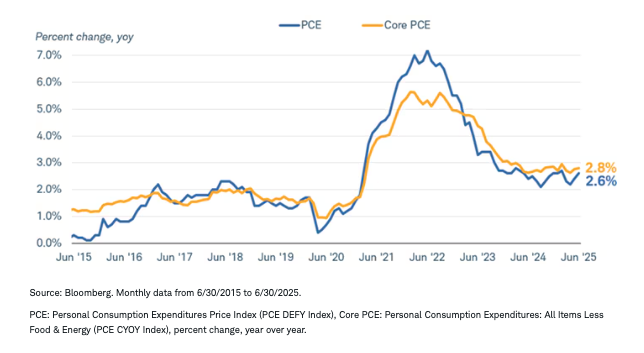

We have been looking for the Fed to begin rate cuts in September as the impact of trade policy, federal government employment cuts, and immigration restrictions begin to show up in the reported data. However, the Fed may not have as much room to lower interest rates as the market expects since inflation is proving to be persistent. High and widespread tariffs are a risk to the Fed's mandate to keep inflation anchored at the 2% level. Inflation has begun to edge higher over the past few months and is likely to continue moving up as tariffs on imported goods are rolled out.

Inflation has remained persistent

With inflation likely to remain stubborn, the Fed may need to temper the magnitude and pace of rate cuts to be sure that the expected slowdown in economic growth will actually help reduce inflation longer term. It has described its policy stance as "restrictive," meaning the federal funds rate (the rate banks charge each other for overnight loans) is high enough to slow economic activity. A move to a "neutral" stance would be warranted if the unemployment rate begins to rise. With inflation holding near 3%, the low end of the fed funds rate is likely to be in the 3.25% to 3.5% region in this cycle.

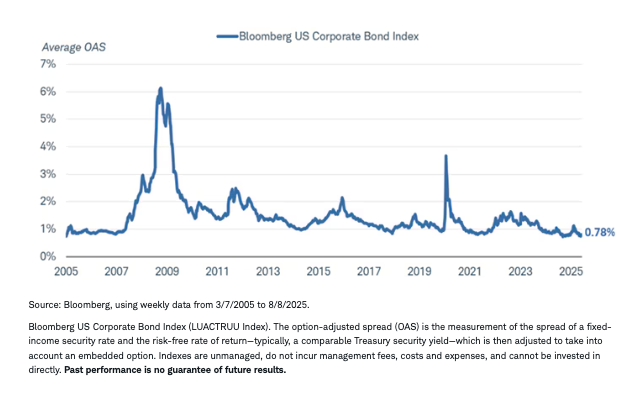

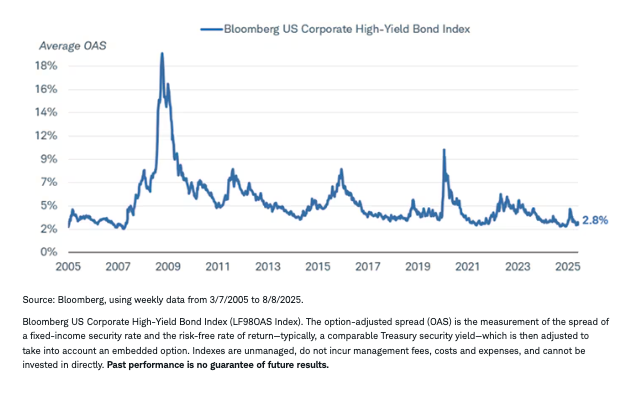

A slower and shallower rate-cutting cycle is also supported by overall easy financial conditions. Credit spreads—the difference between Treasury yields and those of corporate bonds—are very low, indicating that markets are providing ample financing for companies. The buoyance of the equity market and steadiness in consumer spending also suggest that the economy is not weighed down by the level of current interest rates.

Investment-grade credit spreads remain relatively low

High-yield credit spreads also are relatively low

For investors, the implications are that the overall trend in yields is likely to be lower, but the yield curve is likely to remain steep and possibly steepen further. Short-term interest rates are likely to fall more than intermediate- and long-term rates.

We continue to favor keeping the average duration in portfolios in the intermediate-term region of about five to 10 years, while limiting exposure to lower-credit-quality bonds due to stretched valuations. Look for bouts of volatility in the months ahead as the market navigates this tricky turning point.

International stocks and economy: Resilient economic growth

U.S. trade policy has created uncertainty and fostered hesitation by businesses globally this year. While tariff policy is still evolving, the current frameworks agreed to by several nations ahead of the August deadline seems to have bolstered investor confidence. Notably, it appears that most countries are not retaliating with additional tariffs of their own, which is keeping the worst-case scenarios of a trade war at bay.

Economic growth in the first half of 2025 benefitted from the "frontloading" of purchases by U.S. businesses and consumers to get ahead of higher proposed tariffs. This activity seems to have ended, which may create some near-term slowing in global growth for the second half of the year.

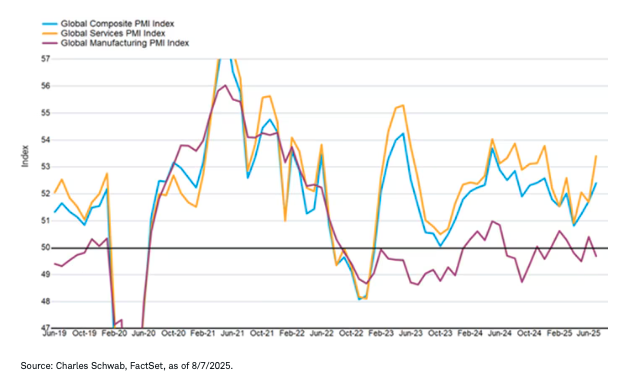

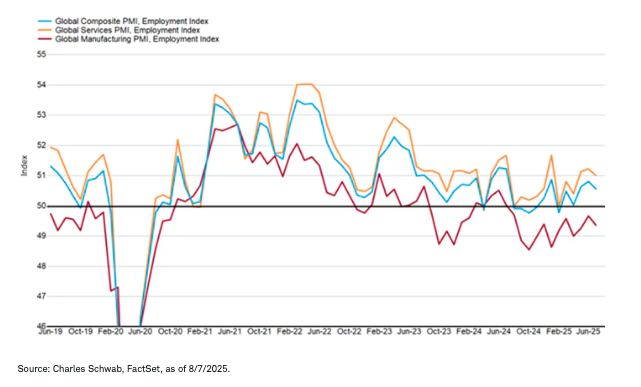

The July release of the Global Manufacturing Purchasing Manager Index (PMI) showed downturns in all sub-components—output, new orders, exports, and employment—tipping the headline index below the 50 level and into contraction territory for the month. By contrast, the Global Services PMI accelerated in July, pushing the overall composite PMI to the strongest level since December, as seen in the blue line in the chart below.

Services strength offsetting manufacturing weakness

The new orders component of the Global Manufacturing PMI dropped in July, suggesting factory output could ease in coming months as the frontloading of goods shipments is digested and newly shipped goods become subject to higher U.S. tariff rates. This could suppress both hiring and capital spending. Inflation trends may vary by country, depending on where tariffs originate, currency moves and other factors, with potential for price upside in the U.S. but price downside outside the U.S. Manufacturers have already cut jobs globally but the services sector keeps hiring, growing overall employment. Should factories continue to cut jobs and these losses spill over into services, there may be weakening growth overall.

Hiring in services offsetting manufacturing job cuts

Changes in trade policy were expected to slow global growth in 2025 compared to last year's pace, but now it seems it may do so at a more modest pace than expected several months ago. The International Monetary Fund's (IMF) July World Economic Outlook forecast GDP growth at 3.0% in 2025 and 3.1% in 2026, an upward revision from the April forecast. This is still slower than the 3.3% rate of growth in 2024 and the pre-pandemic average of 3.7%, but not at recessionary levels. The modest slowing this year is expected to be followed by a reacceleration next year. Under the surface, though, there are divergences, with the IMF expecting the U.S. to slow to 1.9% GDP growth this year from 2.8% last year, while in Germany growth is expected to gradually pick up over the course of this year and next.

Germany is key to our belief in a new growth story in Europe. Government legislation to spend $1 trillion over the next 10 years on defense and infrastructure has supported new optimism in Germany, driving the Ifo Business Climate Index to 88.6 index points in July—a two-year high. More than 60 of Germany's companies are coordinating with German Chancellor Friedrich Merz to announce 631 billion euros ($738 billion) of new projects over the next three years as part of the "Made for Germany" initiative, according to news reports.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

This material is intended for general informational and educational purposes only. This should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decisions.

All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Past performance is no guarantee of future results.

Investing involves risk, including loss of principal.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate this risk.

Currency trading is speculative, volatile and not suitable for all investors.

Forecasts contained herein are for illustrative purposes only, may be based upon proprietary research and are developed through analysis of historical public data.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly. For more information on indexes, please see schwab.com/indexdefinitions.

The Global PMI Composite Output Index, produced by S&P Global, reflects activity in more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies. Readings above 50 signify expansion, while those below 50 indicate contraction.

The Ifo Business Climate Index is based on approximately 9,000 monthly responses from businesses in manufacturing, the service sector, trade and construction. Companies are asked to give their assessments of the current business situation and their expectations for the next six months. Values are indexed to the average for the year 2015.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Investment and Insurance Products Are: Not FDIC Insured • Not Insured by Any Federal Government Agency • Not a Deposit or Other Obligation of, or Guaranteed by, the Bank or any of its Affiliates • Subject to Investment Risks, Including Possible Loss of Principal Amount Invested

The Charles Schwab Corporation provides a full range of brokerage, banking and financial advisory services through its operating subsidiaries. Its broker-dealer subsidiary, Charles Schwab & Co. Inc. (Member SIPC), and its affiliates offer investment services and products. Its banking subsidiary, Charles Schwab Bank, SSB (member FDIC and an Equal Housing Lender), provides deposit and lending services and products.

This site is designed for U.S. residents. Non-U.S. residents are subject to country-specific restrictions. Learn more about our services for non-U.S. residents, Charles Schwab Hong Kong clients, Charles Schwab U.K. clients.

© 2025 Charles Schwab & Co., Inc. All rights reserved. Member SIPC. Unauthorized access is prohibited. Usage will be monitored.

© Charles Schwab

Read more commentaries by Charles Schwab