As we mentioned in our recent Midyear 2025 Outlook: Pragmatic Optimism, Measured Expectations, we expect bond market action to continue to swing between concerns over slowing economic data (lower yields) and larger debt/deficit dynamics (higher yields). But according to recent analysis from the Congressional Budget Office (CBO), tariff revenue could meaningfully impact both sides of the bond market pendulum, which on net, could be beneficial to the Treasury market.

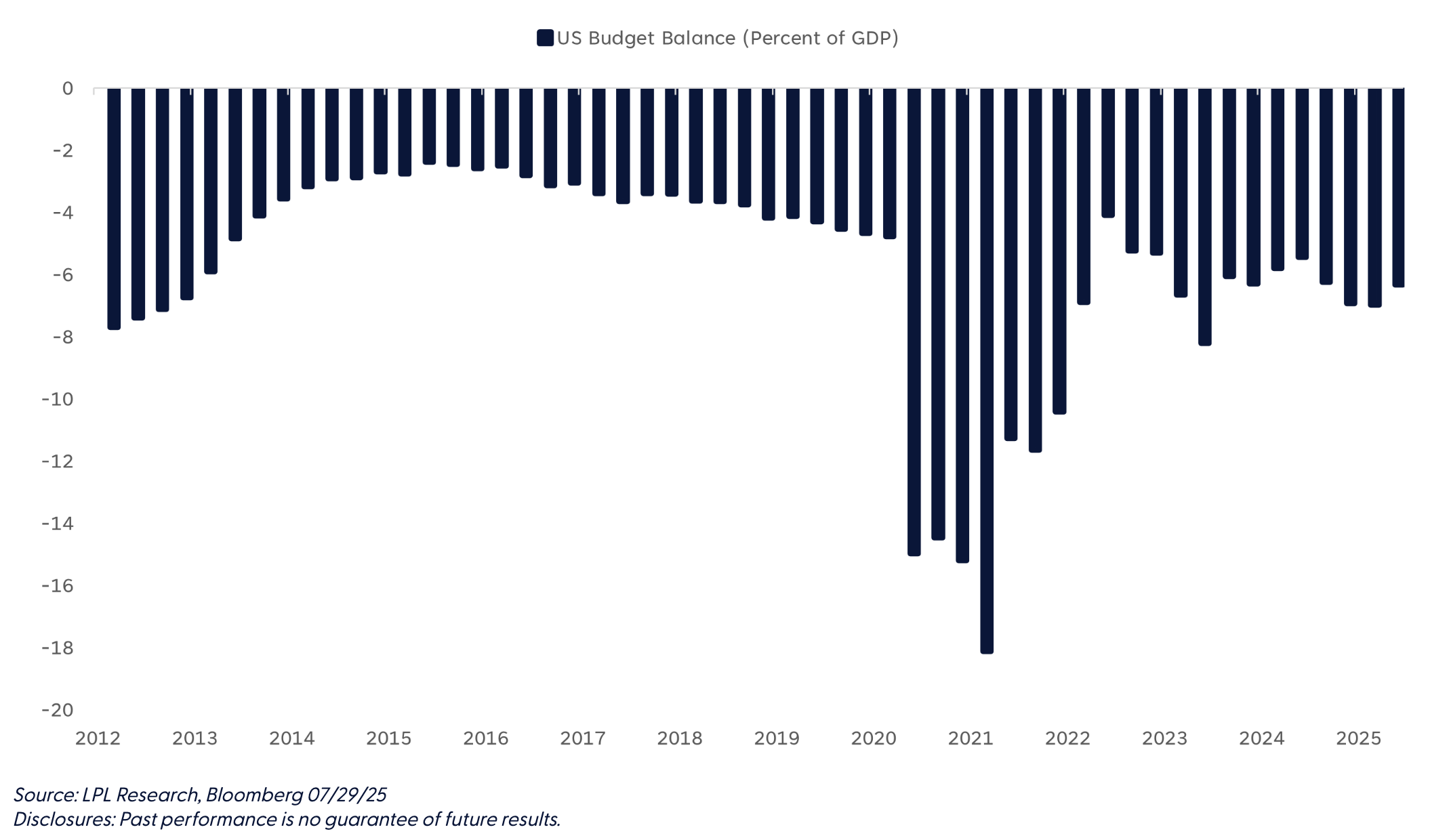

As noted by the CBO, total government outlays for 2025 are roughly $7 trillion, with 2025 revenue equal to around $5.2 trillion, resulting in a budget deficit of nearly $2 trillion per year (or over 6% of gross domestic product (GDP)). With the recent signing into law of the Republican’s One Big, Beautiful Bill Act, initial estimates suggest, in a best-case scenario, that deficits will continue to run in the 6%-7% range of GDP, suggesting Treasury issuance will need to remain elevated to fill the budget gap. The U.S. government has $37 trillion in total debt outstanding, and that number grows by $1 trillion every six months or so. Bigger budget deficits equal more Treasury issuance, all else equal.

Budget Deficits Are Expected to Remain/Worsen Over Time

But tariffs generate direct revenue for the federal government, creating an alternative income stream to traditional taxation. This additional revenue can reduce the Treasury’s borrowing needs. With tariff collection expected to increase revenues/decrease deficits by $4 trillion over 10 years, the Treasury Department can scale back its bond issuance accordingly. This reduced supply of new Treasuries, all else equal, tends to support bond prices and can help contain yields. For a government managing substantial debt levels, this revenue diversification provides fiscal flexibility that markets generally view favorably.

The mechanical relationship is straightforward: every dollar collected through tariffs is potentially one less dollar the government needs to borrow. During periods of significant tariff implementation, Treasury auction sizes may decrease, particularly in shorter-duration bills and notes where adjustments can be made more dynamically.

Rating agency S&P Global Ratings, which recently affirmed its AA+ rating, acknowledged tariffs as credit-positive and highlighted how rating agencies weigh these competing factors. S&P’s analysis suggests that the revenue generation aspect of tariffs, combined with their potential to reduce trade deficits, outweighs near-term growth concerns from a creditworthiness perspective.

Moreover, from a pure market dynamics perspective, tariff implementation creates what could be considered an ideal scenario for existing Treasury holders. On the supply side, revenue generated from tariffs directly reduces the Treasury’s funding needs. But simultaneously, tariffs increase costs somewhere along the manufacturing/distribution/consumption process. So, as tariffs increase business costs and consumer prices, economic growth is set to slow, which has historically benefited Treasuries.

Of course, it isn’t all positive for fixed income markets as tariffs increase price pressures. And, as Fed Chair Jerome Powell noted recently, tariff effects will be short-lived but not necessarily felt all at the same time. It will likely take time for tariff increases to work their way through supply chains and distribution networks, prolonging a return to the Fed’s 2% inflation target. Moreover, tariff income is still expected to be only a drop in the bucket compared to the amount of debt outstanding and is unlikely to replace the need for income taxes. But, it helps.

Love them or hate them, it sounds like tariffs are here to stay (in one way, shape, or form) and that, on balance, could be good for Treasury markets. The combination of technical factors (less supply) and fundamental factors (slowing growth, potential Fed accommodation) creates multiple pathways for Treasury market tailwinds. Even if tariff revenue disappoints or growth impacts prove milder than expected, reduced issuance alone could provide a supportive floor for prices.

While risks certainly exist — particularly if tariffs spark significant inflation requiring monetary tightening — the near-to-medium term setup appears more favorable for Treasury investors now than it did without tariff revenue.

Lawrence Gillum, CFA, guides the fixed income view for LPL Financial Research and has over 20 years of investing experience.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #788440

Read more commentaries by LPL Financial