Spirit’s Financial Troubles Overshadow Record Passenger Traffic and Travel Spending

Membership required

Membership is now required to use this feature. To learn more:

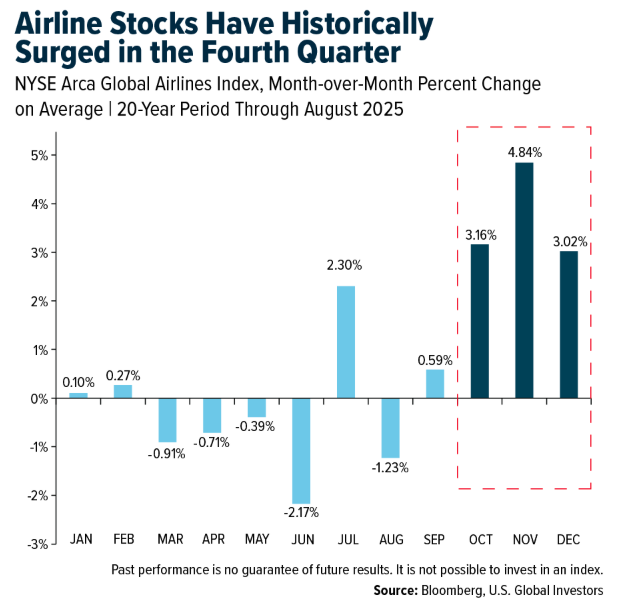

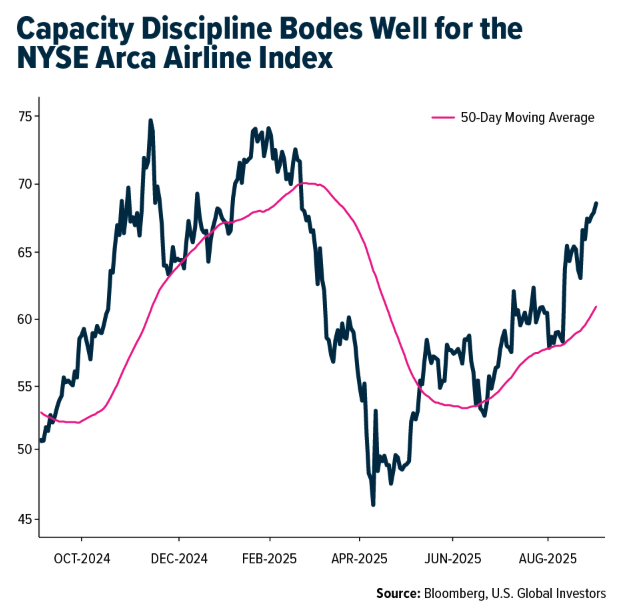

View Membership BenefitsFall isn’t in the air yet here in South Central Texas, but the season is often associated with something else: stronger performance in airline stocks.

Looking back over the past 20 years, airline equities have tended to outperform in the final three months of the year, with the NYSE Arca Global Airlines Index gaining over 3% on average in October; this is followed by an even stronger showing in November and a 3% increase in December on average. According to the Bank of America, the industry has historically outperformed the S&P 500 in three of the last six months of the year—namely September, October and November.

Knowing this, now might be an ideal time to consider increasing your exposure to the global airlines industry. To learn more, send an email to [email protected] with the subject line AIRLINES.

Restructuring and Consolidation Continue to Reshape U.S. Aviation

You might have seen the news this week that Spirit Airlines has filed for bankruptcy for the second time in less than a year.

To some, this is proof that the ultra-low-cost carrier (ULCC) model, which Spirit helped pioneer, is on its way out.

But for those of us who’ve been following the airline industry for years, this is simply the latest chapter in a familiar story of resilience and consolidation.

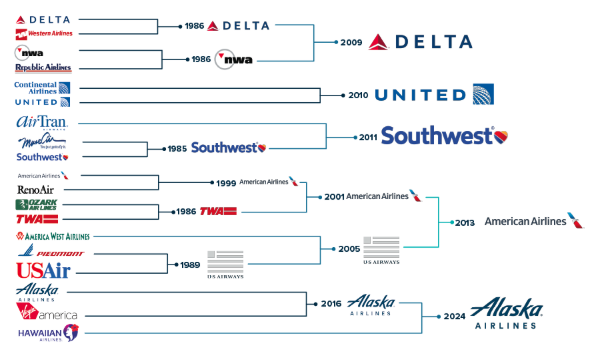

Between 2002 and 2007, several household airline names entered bankruptcy protection. Those included US Airways, which restructured twice in the span of three years; United Airlines, which spent four years reorganizing under court supervision; and Northwest Airlines and Delta Air Lines, which filed in 2005 and emerged two years later.

These restructurings were painful but necessary. Airlines shed excess debt, renegotiated labor contracts and modernized fleets.

They also introduced new revenue streams. Ancillary fees—those charges for checked bags, seat upgrades and snacks—went from being ridiculed to becoming a crucial profit center.

By the time the financial crisis hit, airlines were leaner and better equipped to withstand shocks. US Airways merged with America West in 2005, and Delta absorbed Northwest in 2008. These combinations have given rise to the competitive landscape we know today, dominated by four major carriers, hotly pursued by Alaska Airlines, which finalized its acquisition of Hawaiian Airlines last year and now controls a little over 6% of the domestic market.

Can the ULCC Model Survive?

I’m not trying to sugarcoat Spirit’s situation. The airline emerged from Chapter 11 just this past March after restructuring roughly $1.6 billion in debt, only to find itself back in court by August.

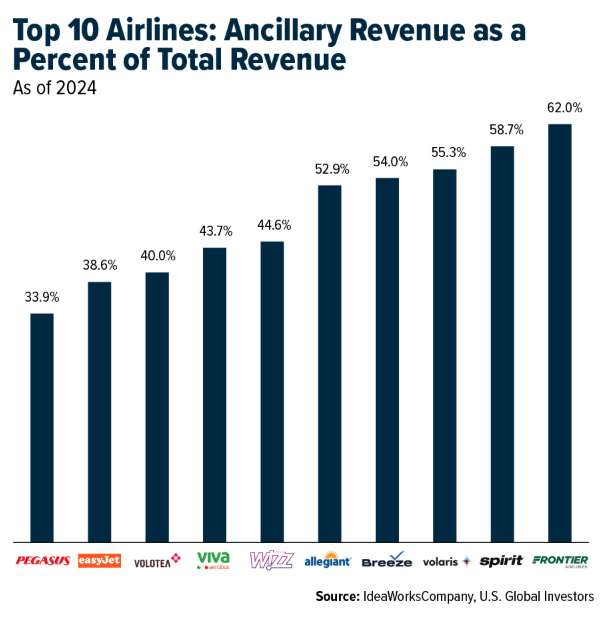

It’s worth remembering that Spirit was once the poster child for the ULCC model. Its no-frills approach—non-reclining seats, fees for carry-ons and à-la-carte pricing—allowed it to offer rock-bottom fares that attracted price-sensitive travelers. Ancillary revenue became its lifeblood, with nearly 59% of its total revenue in 2024 coming from add-ons, according to IdeaWorks data. That put Spirit near the very top of the global rankings.

The Nickel-and-Diming Backlash

But the ULCC formula has come under pressure in the U.S. Some consumers have grown weary of “nickel-and-diming,” and legacy carriers have learned to compete aggressively with their own stripped-down basic economy fares. Bill Franke, Frontier’s chairman and one of the architects of the ULCC playbook, recently admitted that “the original ultra-low-cost model is gone for good in the U.S.”

That doesn’t mean the model has no future. It still thrives in Europe, Latin America and Asia, where competitors like Ryanair, Wizz Air and Volaris are profitable and expanding. But in the U.S., where customer expectations are higher and competitors more entrenched, some ULCCs face an uphill battle.

Air Travel Demand Reaches New Heights

At the same time, it’s important not to lose sight of the fact that demand for air travel is booming.

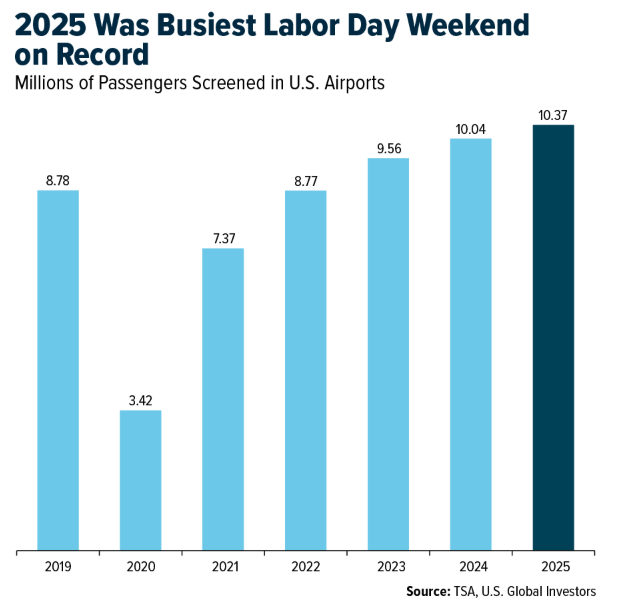

This summer, the Transportation Security Administration (TSA) screened record numbers of passengers. Over the Labor Day weekend alone, nearly 10.4 million travelers passed through airport security, a 3.3% jump from last year. Eight of the 10 busiest days in TSA’s two-decade history occurred just this summer.

Globally, passenger traffic grew 4% year-over-year in July, according to the International Air Transport Association (IATA). International routes were particularly strong, rising 5.3%. And here in the U.S., travel exports—foreign visitors spending on U.S. goods and services—hit an all-time high of $126.9 billion in the first six months of 2025.

Corporate Bankruptcies Surge to Post-Crisis Highs

Of course, we can’t ignore the macroeconomic backdrop. Spirit’s downfall is partly the result of higher interest rates. After years of cheap credit, the Federal Reserve hiked aggressively beginning in 2022, pushing borrowing costs above 5%. Corporate bankruptcies spiked, reaching their highest level since 2010.

Airlines, like other capital-intensive industries, rely heavily on debt financing. Elevated rates increase debt service costs, squeezing margins.

But remember: the majors are better positioned today than they were in the early 2000s. Balance sheets are stronger, cash reserves are larger and fleets are more efficient.

What’s more, the Fed cut its benchmark rate by a full percentage point late last year and has kept it steady in 2025. That policy shift, combined with cooling inflation, should ease some of the pressure on corporate borrowers going forward.

Airlines Add Capacity Ahead of Busy Winter Travel

I don’t believe Spirit’s bankruptcy should be taken as a bellwether for the entire industry, which is consolidating and streamlining.

The upcoming winter travel season looks set to be one of the busiest on record. United, Frontier and others are already adding capacity to key leisure markets like Orlando, Las Vegas and Fort Lauderdale.

For long-term investors, that’s an attractive setup.

Spirit is in trouble, yes, but the industry as a whole is in a far different position than it was 20 years ago. I’ve seen this movie before, and I think I know how it ends: with stronger airlines and better opportunities for investors who stay the course.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.32%. The S&P 500 Stock Index rose 0.23%, while the Nasdaq Composite climbed 1.14%. The Russell 2000 small capitalization index gained 0.97% this week.

- The Hang Seng Composite gained 1.47% this week; while Taiwan was up 1.08% and the KOSPI rose 0.60%.

- The 10-year Treasury bond yield fell 14 basis points to 4.09%.

Airlines and Shipping

Strengths

- The best-performing airline stock for the week was Embraer, up 8.4%. American Airlines has added the 1,000th aircraft to its mainline fleet. The carrier took delivery of the airplane, a Boeing 787-9, at Dallas/Fort Worth International Airport. The Dreamliner is fitted with American’s recently unveiled Flagship Suites, which are being rolled out on all of the airline’s new 787-9s.

- According to UBS, benefiting from higher prices for delivered ships and lower steel costs, CSSC’s shipbuilding and repair revenue rose 12% year-over-year in the first half of 2025, with a gross profit margin of 11.7%, an increase of 4 percentage points year-over-year.

- According to Raymond James, during mediation, AC-CUPE agreed in advance that if the tentative agreement is not ratified, the wage portion would proceed to mediation, followed by arbitration if necessary. In short, regardless of the outcome of the ratification vote on September 6, there will be no strike or lockout.

Weaknesses

- The worst-performing airline stock for the week was JetBlue, down 5.1%. According to CIBC, major U.S. airlines hired 52 pilots in July, compared to 55 in June. This is the lowest monthly hiring level recorded in the past decade. Only three airlines hired pilots in July: Hawaiian Airlines (15 pilots), UPS (15 pilots), and United Airlines (22 pilots).

- According to Goldman Sachs, the number of laden vessels traveling from China to the United States declined by 10% sequentially and was down 19% on a year-over-year basis. Data suggests that the second half of August showed mixed trends, with a potential turn more negative heading into early September, based on Port of Los Angeles data.

- According to Morgan Stanley, Volaris’ total traffic, measured in revenue passenger miles (RPM), increased by 1.9% year-over-year in August. Quarter-to-date traffic is up 1.0% year-over-year, compared to third-quarter 2025 consensus expectations of a 3.9% increase.

Opportunities

- UBS believes the aviation cycle will begin to turn once Airbus and Boeing ramp up production—well before the current replacement demand of 2,500 to 3,500 aircraft is fulfilled. They forecast that aftermarket growth rates could return to 6% by 2027–2028.

- China Merchants Energy Shipping Management remains constructive on the tanker market outlook. Management sees potential tailwinds from legitimate tankers regaining market share from the “dark fleet,” increased crude production and inventory builds, and a potential U.S.–China trade agreement, coupled with seasonal demand. According to Morgan Stanley, they also noted that elevated asset values may benefit vessel owners by enabling higher disposal gains compared to previous years.

- According to TD, legacy carriers are scheduled to grow fourth-quarter 2025 capacity by 4.8% year-over-year, with domestic up 4.0% and international up 6.1%. Notable growth includes American Airlines at Chicago O’Hare (+27%) and LaGuardia (+15%), and United Airlines at Newark (+10%).

Threats

- According to Raymond James, some portion of Spirit Airlines’ capacity is likely to be removed, which would ease pressure on the domestic market—particularly in the main cabin—at a time when domestic demand is beginning to recover from the sharp decline seen earlier in the year.

- The simple average spot freight rate for July and August 2025 was down an estimated 6% quarter-over-quarter on North America routes and up 3% on Europe routes. Morgan Stanley expects the downward trend in spot freight rates to continue due to ongoing vessel oversupply.

- Air Canada faces increased competition as WestJet has announced a new order for 60 Boeing 737-10 MAX aircraft (plus 25 options), along with seven additional Boeing 787-9 widebody jets.

Luxury Goods and International Markets

Strength

- The Labor Department reported Wednesday that U.S. job openings fell to 7.18 million in July, down from 7.4 million in June and modestly below expectations. The JOLTS survey showed significant declines in openings across healthcare and social assistance (–181,000) and retail (–110,000), while layoffs edged slightly higher.

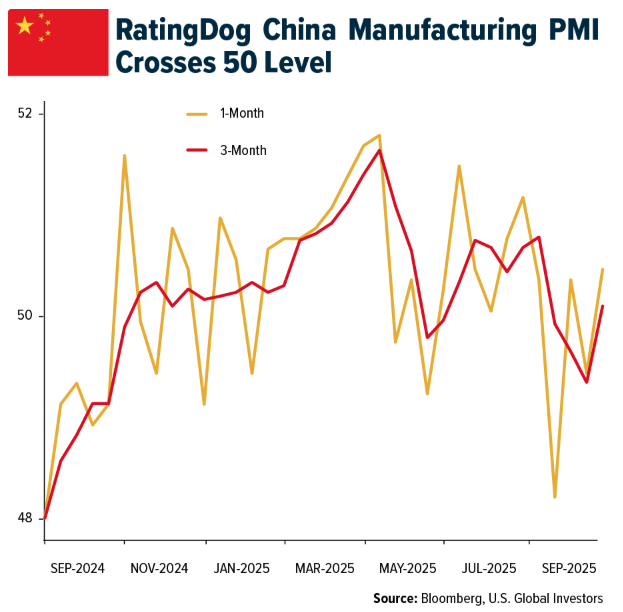

- The RatingDog China Manufacturing PMI (previously known as Caixin PMI) rose to 50.5, up from 49.5 in July—marking the first move back into expansion territory in five months. The 50-point threshold separates expansion from contraction—thus, the RatingDog reading suggests a modest recovery in private-sector manufacturing activity.

- The RealReal, an online second-hand luxury retail platform, was the top performer in the S&P Global Luxury Index, climbing 13.7%. UBS Group recently raised its price target to $8 with a Neutral rating, while B. Riley Securities lifted its target to $9 with a Buy rating.

Weaknesses

- Tesla’s sales are declining across major European electric vehicle markets, with registrations down 39% in Germany last month and 56% year-to-date. Tesla registrations fell by 39% in the past month. And, Tesla’s sales are down 56% year-to-date in Germany, highlighting persistent sales weakness in the EU region.

- Sales in the Eurozone rose by 2.2% in July, a slower pace compared to the stronger 3.1% increase recorded in June. This signals a weakness as the latest growth was softer than previously reported.

- CityChamp Watch & Jewellery, a Hong Kong–listed jewelry and watch retailer, was the worst-performing stock in the S&P Global Luxury Index, falling 9.3%. The shares declined after weak earnings and a correction revealed that one of its subsidiaries had lost money instead of making a profit.

Opportunities

- Weaker-than-expected U.S. job data is raising expectations that the Federal Reserve could cut interest rates as soon as this month. A softer labor market gives the Fed more room to shift toward easing, and many analysts believe it may also accelerate the pace of rate cuts going forward. Lower borrowing costs are aimed at stimulating economic growth, supporting hiring, and ultimately helping to improve consumer spending.

- Tesla saw encouraging momentum in Turkey, with car sales climbing as demand strengthens in the market. This growth provides a bright spot for the company, even as sales across the broader EU remain weak, highlighting Turkey’s potential as an important driver for Tesla’s regional expansion.

- China’s services activity expanded at the fastest pace in over a year in August, driven by increased tourism, Bloomberg reported. The rebound in domestic and international tourism presents a strong opportunity for increased consumer spending. Rising demand for travel, hospitality, and leisure is fueling growth across the services sector.

Threats

- MarketWatch reported this week on a Wall Street Journal–NORC poll showing that only 25% of Americans believe they have a good chance of improving their living standards—the lowest level since the survey began in 1987. More than three-quarters lack confidence that the next generation will be better off, and nearly 70% say the American Dream no longer holds true or never did, the highest share in almost 15 years.

- Macy’s shares jumped as much as 22% on Wednesday after the company raised its full-year outlook, now expecting up to $21.45 billion in sales. Last week, Kohl’s shares surged 24% in a single trading day after issuing a stronger forecast. Meanwhile, TJ Maxx owner TJX and Ross Stores indicated that U.S. shoppers are still spending but are increasingly looking for cheaper options.

- Shares of LVMH fell more than 4% on Thursday after Jefferies issued cautious commentary, questioning whether a potential third-quarter rebound would translate into stronger 2026 results, while forecasting improvement in the second half of next year. The analyst raised the price target to €470 from €450, though LVMH shares continue to trade around €499 on the Paris Stock Exchange.

Energy and Natural Resources

Strengths

- The best performing commodity for the week was natural gas, up 1.47% on weekly storage data that just met expectations. Oversupply has been a headwind but the lack of new production coming online, and the approaching winter weather season has finally seen natural gas prices catch a break. According to Morgan Stanley, iron ore prices have shown significant strength over the past quarter, holding above the $100/ton mark, supported by continued China steel exports strength and sentiment around anti-involution announcements supporting expectations of improved steel mill profitability.

- Asia’s imports of crude oil rebounded in August as heavyweight buyers China and India bought more crude oil from top exporters in the Middle East. The world’s top importing region saw arrivals of 27.18 million barrels per day in August, up from 24.91 million barrels per day in July and above 26.39 million barrels per day from the same month in 2024, according to data compiled by LSEG Oil Research.

- Aclara Resources Inc. secured funding from the U.S. government for a Brazilian rare-earth project in the latest example of Western nations attempting to reduce reliance on the dominant supplier, China. The U.S. International Development Finance Corporation will back the developer with as much as $5 million for the Carina heavy rare-earth project in mid-western Brazil, Toronto-listed Aclara said in a statement Tuesday.

Weaknesses

- The worst performing commodity for the week was sugar, down 5.01%, on what is looking to be an abundant harvest for sugar cane in Brazil. U.S. economic activity saw “little or no change” across most of the country in recent weeks, the Federal Reserve said in its Beige Book survey of regional business contacts. “Most of the twelve Federal Reserve districts reported little or no change in economic activity since the prior Beige Book period,” according to the report published Wednesday. “Across districts, contacts reported flat to declining consumer spending because, for many households, wages were failing to keep up with rising prices.”

- Oil fell after a report that the OPEC+ alliance will consider a fresh round of production increases when the group meets over the weekend. West Texas Intermediate (WTI) crude fell as much as 2.6%, extending an earlier decline after softer-than-expected US economic data dented longer-term consumption expectations. OPEC+ will consider further raising output at a meeting on Sunday, Reuters reported, citing two people familiar with the discussions.

- Teck Resources’ shares were under pressure after the miner hit pause on its major growth projects to focus on troubles at its flagship copper mine in Chile. The Canadian company launched a comprehensive review of the Quebrada Blanca operation, which includes assessments of operating plans, input from third-party experts and execution tracking. Teck said it will defer sanctioning major growth projects until the Chilean mine achieves steady-state operations and ramp-up targets, according to Dow Jones.

Opportunities

- Indian refiners boosted U.S. crude oil purchases this month, drawn by competitive prices, trade sources said, a move that could help narrow the country’s trade deficit with the United States amid tensions between the two nations. The country’s top refiner, Indian Oil Corp, has bought 5 million barrels of U.S. WTI crude for delivery in October and November via a tender, trade sources said.

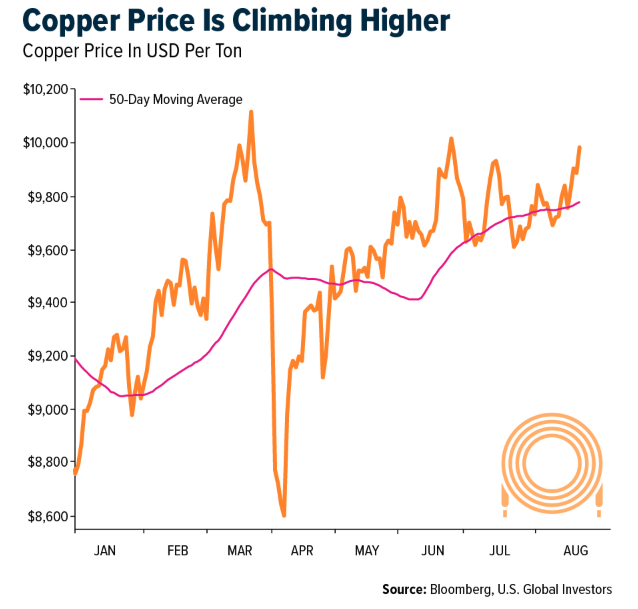

- According to Bank of America, the copper price has more than doubled since its 2020 lows and the metal is at the epicenter of the energy transition, which means that the lack of mine supply growth is being felt acutely. Indeed, tight concentrates availability is increasingly capping production at China’s smelters and refiners, potentially pushing consumers of refined metal back into international markets.

- Swelling U.S. demand for electricity has the potential to boost coal consumption as much as 57%, according to mining giant Peabody Energy Corp., in what would be a major shift for an industry that has been waning for years. With the U.S. seeking to meet skyrocketing demand and the Trump administration pushing to prop up the coal industry, Peabody expects utilities to ramp up output from coal plants that are running well below full speed, the company said in an investor presentation on Wednesday.

Threats

- Russian crude is getting even cheaper for India buyers as New Delhi faces sustained U.S. pressure to cut its oil trade with Moscow, which the Trump administration says is helping fund the war in Ukraine. The price of Urals crude has dipped to a discount of $3 to $4 a barrel to Brent on a delivered basis, according to people who received offers for the Russian grade, asking not to be identified discussing sensitive information.

- President Donald Trump’s energy chief says soaring U.S. electricity prices are his biggest concern, remarks that come as analysts warn utility bills could become a political liability for Republicans. “It’s what I worry about most seven days a week,” Energy Secretary Chris Wright told Fox Business News on Tuesday. “We want to stop the rise in electricity for Americans and reshore jobs and opportunity there.”

- According to CNN, the Trump administration is expected to implement trade measures against Brazil’s imports of diesel from Russia, like the actions previously taken with India. According to sources in Washington, the measure targeting Brazil would likely be enforced within approximately one to one and a half weeks. Notably, according to data from July 25, imports of diesel from Russia accounted for 58% of the total, followed by the US with 33%.

Bitcoin and Digital Assets

Strengths

- Tether is expanding its gold push by investing another $100 million into Canadian royalty company Elemental Altus after already building a major stake earlier this year. The move adds to its $8.7 billion stockpile of gold bars stored in Switzerland and highlights its strategy of tying stablecoin operations to hard assets.

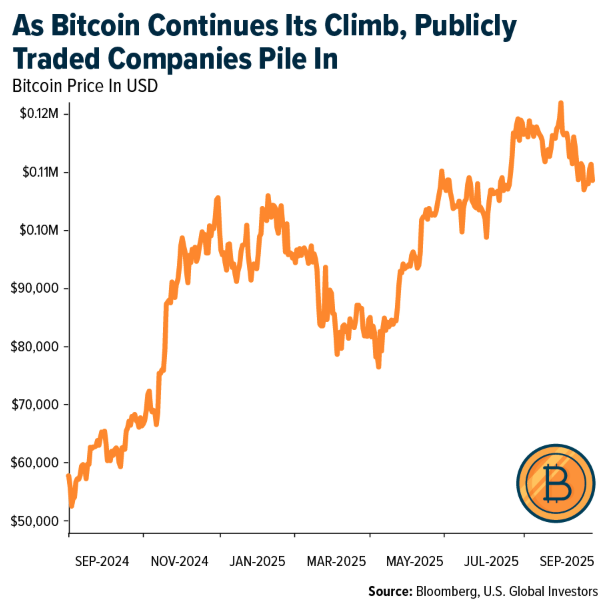

- Publicly traded companies worldwide now hold more than 1 million BTC, representing nearly 5% of the total supply. Strategy (MSTR) dominates the list with 636,505 BTC, followed by MARA Holdings with 50,639 BTC and XXI with 43,514 BTC, while dozens of other firms contribute smaller but growing allocations.

- Stablecoins could shift from niche to mainstream by 2030, powering over $50 trillion in annual payments—especially in cross-border and B2B flows—while retail adoption grows more slowly, mostly through digital wallets, e-commerce and gaming.

Weaknesses

- Nasdaq is tightening rules on companies trying to pump their stock by raising money to buy crypto, forcing some to get shareholder approval first and potentially slowing the boom of firms racing to turn themselves into crypto plays.

- Trump’s family-backed crypto project World Liberty Financial stumbled at launch after billionaire investor Justin Sun’s wallet was blacklisted, sparking a public clash, a 40% price drop and fresh doubts about the project’s credibility.

- North Korean hackers are impersonating recruiters on LinkedIn and Telegram, luring crypto workers with fake job offers. Once victims download “test assignments,” hidden malware steals access to their wallets.

Opportunities

- Polymarket says it now has the regulatory approvals it needs to launch in the U,S., after the Commodity Futures Trading Commission (CFTC) granted a no-action letter that clears costly reporting hurdles and effectively gives the crypto prediction market the green light to go live.

- Japan Post Bank plans to let its 120 million account holders swap deposits for DCJPY tokens by 2026, enabling near-instant settlement of securities and other transactions as it joins the MUFG-backed tokenized asset network.

- David Bailey, the Trump-linked crypto investor, has unveiled “MSTR Squared,” a strategy where his Bitcoin treasury company invests directly in other Bitcoin treasury firms. The goal is to expand corporate Bitcoin holdings globally and turn these treasuries into a powerful network of capital.

Threats

- An $8.5 million luxury cruise to the North Pole carrying over 150 elite Russian-speaking guests was abruptly canceled after a crypto scandal erupted, derailing what was meant to be an exclusive high-society Arctic voyage.

- Coinbase has filed a lawsuit against Dynapass, seeking a ruling that its use of two-factor authentication does not violate Dynapass’s patent. The company also argues that the patent is invalid and wants the court to declare it unenforceable.

- In India, several crypto exchanges have been flagged for secretly using client assets in trading, lending, or staking without disclosure. Users bear the risk while platforms keep the profits.

Defense and Cybersecurity

Strengths

- The U.S. approved an $8.5 billion sale of the Patriot Defense System to Denmark, involving contributions from Lockheed Martin and Northrop Grumman, to enhance Denmark’s defense capabilities and military readiness.

- The UK secured a £10 billion deal to supply warships to Norway, significantly boosting defense stocks like Rolls-Royce, BAE Systems and Babcock, with shares rising over 2%.

- The best performing stock was Karman Holdings. It rose 17.06% after Raymond James initiated coverage with a strong-buy rating and $100 target, saying its margins and growth prospects could make the defense supplier’s business triple by 2030.

Weaknesses

- A federal jury ordered Google to pay $425 million for privacy violations related to unauthorized data collection, and a U.S. court mandated Alphabet to share its search data with competitors to promote fair competition in the artificial intelligence (AI) sector.

- TSMC, the Taiwanese semiconductor maker, announced it will raise prices on its advanced chip processes by 5–10%, affecting major clients such as Nvidia and Apple, as the company seeks to offset declining profit margins and rising supply chain costs. At the same time, the U.S. government revoked TSMC’s special permit that previously allowed shipments of chipmaking tools to China without licenses, meaning all future exports to its Nanjing fab will now require explicit U.S. approval — a move that could further complicate operations as the company implements the price hikes.

- The worst performing stock this week was Redwire Corporation. It was down 6.62% as a costly integration of Edge Autonomy, contract delays, a fresh securities-fraud investigation and worsening technical momentum fueled investor sell-off.

Opportunities

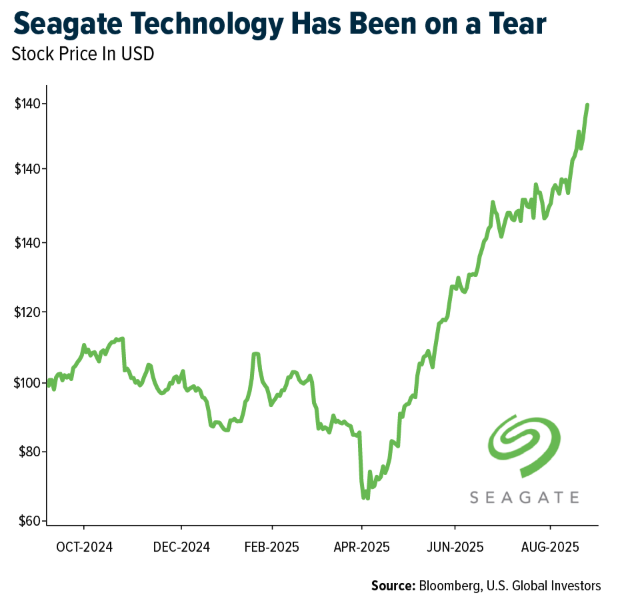

- Seagate stock has been climbing thanks to booming demand for high-capacity hard disk drives (HDDs) from AI and cloud data centers, strong quarterly results with revenue and profit growth, and investor confidence reinforced by a $5 billion buyback program. Its rollout of heat-assisted magnetic recording (HAMR) drives, future roadmap toward 100 terabyte (TB) HDDs, and positive analyst upgrades have pushed the shares to new all-time highs.

- L3Harris and Rheinmetall are joining forces to build next-gen combat vehicles by combining L3Harris’ comms and mission tech with Rheinmetall’s vehicle design, centered on a new low-profile sighting system that boosts targeting and battlefield decision-making while cutting costs and easing integration.

Threats

- A senior United Arab Emirates (UAE) envoy warned that annexing the West Bank in Israel would be a “red line” ending regional integration and the two-state solution, stressing that her statement came right after a far-right Israeli politician called for seizing the West Bank.

- Putin warned that Russia would treat any Western troops in Ukraine as legitimate targets, dismissing peace prospects while tightening ties with China and India, even as Trump’s deadlines for a deal lapse and Zelensky rejects Moscow as a venue for talks.

- Cloudflare was affected by a data breach linked to the Salesloft Drift supply-chain attack, compromising Salesforce instances and exposing customer support data, attributed to the UNC6395 threat group and impacting several major companies between August 8 and 18.

Gold Market

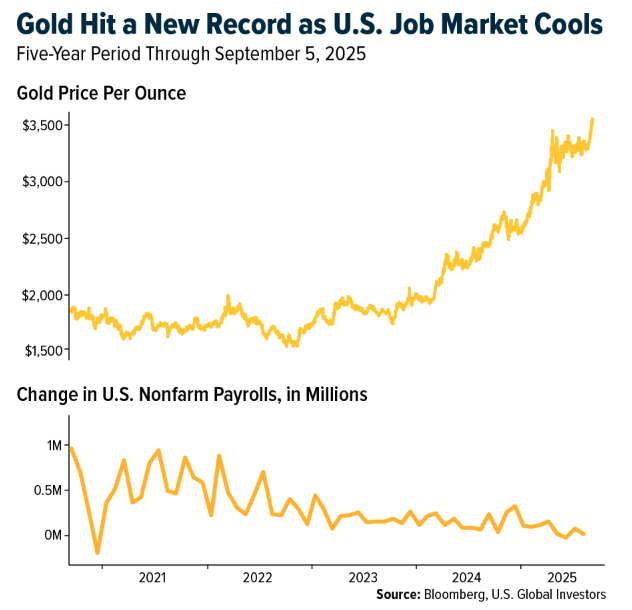

This week gold futures closed the week at $3,644.220, up $128.10 per ounce, or 3.64%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 5.27%. The S&P/TSX Venture Index came in 3.34%. The U.S. Trade-Weighted Dollar finished the week essentially unchanged.

Strengths

- The best performing precious metal for the week was gold, up 3.64% on expectations that the Federal Reserve might even cut interest rates by 50 basis points at their September 17 meeting, as a weaker-than-expected gain in Nonfarm Payrolls highlighted the lackluster in the labor market. Gold hit a new all-time on Friday with the new data point. Gold first hit a record high earlier in the week as the prospect of U.S. interest-rate cuts and growing concerns over the Federal Reserve’s future lent fresh impetus to the multiyear rally in precious metals

- The World Gold Council (WGC) is seeking to launch a new digital form of gold that would facilitate transactions in fractionalized ownership and trading of physical gold held in segregated accounts. They are looking to trial the program for the first quarter of 2026. They are trying to standardize the digital layer of gold to compete with other assets. The World Gold Council had tremendous success launching its physical gold ETF.

- Zijin Minig Group Co. Ltd., China’s largest gold producer, announced they will IPO Zijin Gold International on the Hong Kong Stock Exchange to raise at least $3 billion in what would the Exchange’s second largest IPO, rivaled only by Contemporary Amperex Technology Ltd.’s $5.3 billion raise in May, according to Bloomberg. Li Xiaofeng, a leading partner at Dentons, was quoted in ChinaDaily saying that “Zijin needs a large pool of offshore money to invest and expand production in their assets.” New money is coming to invest in potential acquisitions.

Weaknesses

- The worst performing precious metal for the week was palladium, but still up 0.40%, likely with sentiment for economic growth being chipped away by a lack of confidence by both industry and consumers. Shandong Gold Mining shares fall as much as 5% in Hong Kong, after the Chinese company raised $500 million in an upsized H-share placement at a discount, but that didn’t last long, with the share only down 1.75% by the close. The company offered up to 136.5 million shares at HK$28.58 apiece in a placement, according to a filing to HKEX, but finished the week at HKA$32.82, a new six-month high.

- According to Morgan Stanley, African Rainbow Minerals reported headline earnings per share (EPS) of R11.66 – R14.25, with the midpoint being R12.96. Visible Alpha consensus is R17.57/share. The miss was due to higher manganese costs, Bokoni costs and Two Rivers mine weakness. The tax expense was R489m higher than their estimate.

- Following the operational update in early June, Pan African reported a trading statement ahead of its detailed financial results, which are expected on September 10, 2025. Headline EPS is expected to be in the range of US¢5.68-6.10/share versus BMO’s estimate of US¢6.94/share.

Opportunities

- Bank of America calculates that the world total of central banks must purchase a little over 11,000 tons (t) of gold to attain gold holdings of 30% of total reserves. This is equivalent to approximately 10 years of purchasing at recent elevated annual levels. If they exclude central banks that already hold at least 30% of reserve assets in gold, they calculate that the remaining central banks must purchase 24,665 tons to attain gold holdings at 30%. This is equivalent to over two decades of purchases at recent elevated levels.

- Bank of America raised their long-term gold price +25% to $2500. They raised their long-term silver price +30% to $35/ounce. In their view, the conditions that have led to recent strength in gold price look likely to persist, namely: (1) U.S. structural deficit; (2) inflationary pressure from deglobalization; (3) perceived threats to the independence of the U.S. central bank; and (4) global geopolitical issues. Investors have piled into gold-backed exchange-traded funds this year, with total holdings at the start of September reaching their highest point since June 2023, according to data collected by Bloomberg.

- The quest to add real tangible value to crypto assets continues to spill over into gold and gold equities too. Stablecoin issuer Tether Holding SA has added a second time to their Elemental Altus Royalties Corp. position on Friday. Elemental Altus Royalties also announced on Friday morning they were acquiring EMX Royalty Corp in an all-stock deal. The Financial Times reported that Tether has held talks about investing in gold mining, in addition to bullion. Stablecoin buyers own a derivative that is tied to the value of the dollar and its associated credit risks.

Threats

- The market for natural diamonds is in crisis, with cut-price lab-grown equivalents hitting demand particularly hard in the U.S., the biggest market for diamonds. They accounted for almost half of engagement ring purchases last year compared with 5% in 2019, according to jewelry insurer BriteCo Inc.

- Pan African reported 196,926 ounces of gold were sold in F2025, which is slightly higher than BMO’s estimate of 194,328 ounces. Of these gold sales, 105,004 ounces were subject to hedges and therefore did not benefit from the current gold price environment. This negatively impacted profits by 23%, according to BMO.

- An outbreak of Ebola virus was declared in a remote area of the Democratic Republic of Congo (DRC). Fifteen deaths and 28 suspected cases have been reported. The last outbreak was in 2022, which took three months to control, showing this health risk is not to be taken lightly, with a 64% mortality rate. There are no reports of any mining operations being impacted at this time.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2025):

Boeing

Airbus SE

Air Canada

Delta Air Lines Inc.

Alaska Air Group Inc.

United Airlines Holdings Inc.

American Airlines Group Inc.

Southwest Airlines Co.

Frontier Group Holdings Inc.

Pegasus Hava Tasimaciliği AS

easyJet PLC

Allegiant Travel Co.

Ryanair Holdings PLC

Aclara Resources Inc.

Teck Resources Inc.

Alphabet Inc.

Seagate Technology Holdings PL

Tesla Inc.

LVMH Moet Hennessy Louis Vuitton

Pan African Resources PLC

EMX Royalty Corp.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The NYSE Arca Global Airline Index is a modified equal- dollar weighted index designed to measure the performance of highly capitalized and liquid international airline companies.

A message from Advisor Perspectives and VettaFi: Thinking about starting your own RIA, making a move to a different firm, or specializing in a new area? Read our latest articles on financial advisor transitions.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits