Margins, Mid-Caps and Market Resilience

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Takeaways

- In a 2025 market dominated by tariff and inflation concerns, mid-caps have preserved profit margins near 30-year medians, highlighting their operational adaptability.

- While AI headlines center on large-cap growth, mid-sized companies are leveraging it as a margin defense tool, offsetting wage and input cost pressures through faster tech integration.

- Despite their resilience and balanced growth potential, mid-caps remain underrepresented in most portfolios, offering advisors a compelling opportunity to enhance diversification and valuation efficiency.

In a recent LinkedIn newsletter, we highlighted how mid-caps have historically delivered a compelling mix of growth and resilience, the "sweet spot" between innovation and maturity. They've graduated from the start-up phase, proven profitability and often trade at more reasonable valuations than their large-cap peers, while still delivering stronger earnings growth than small caps.

In this follow-up, we want to take that conversation a step further. Beyond the long-term track record of mid-caps, today's environment adds another reason for advisors to revisit the segment: their resilience in navigating policy shocks, cost pressures and market uncertainty.

Resilience under Tariff and Inflation Pressures

Much of the conversation around equity markets in 2025 has focused on tariffs and inflation. Headlines warn of margin erosion, yet mid-caps are holding up surprisingly well.

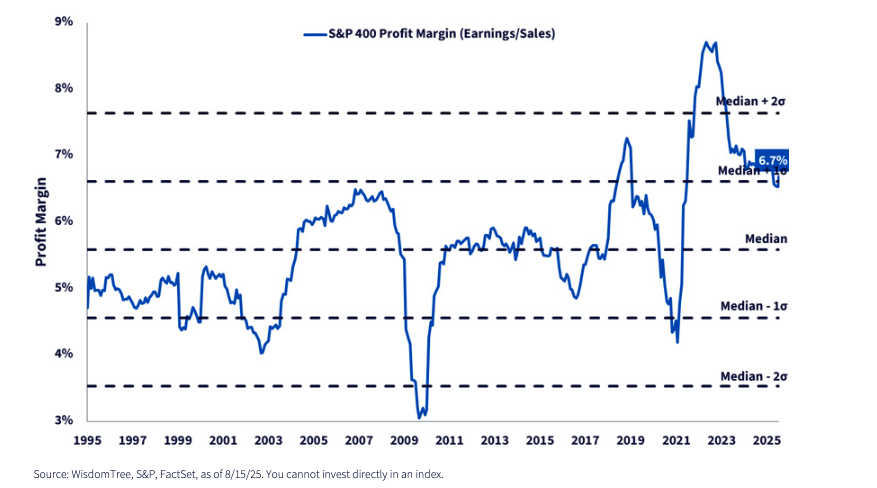

The S&P MidCap 400 Index currently shows a profit margin of about 6.7%, essentially unchanged from 2024 and comfortably above its 30-year median. This is a reminder of mid-caps' ability to adapt. They may lack the scale of mega-caps, but they often run leaner, more flexible operations that can adjust pricing, shift supply chains and preserve profitability in difficult environments.

No Sign of Tariffs Eroding Mid-Cap Margins

AI beyond Growth: A Cost-Defense Tool

AI has become synonymous with large-cap technology growth stories. But its real potential may be in cost containment across traditional industries.

As WisdomTree Senior Economist Professor Jeremy Siegel has noted, productivity gains from AI are not confined to Silicon Valley. Mid-sized companies, with leaner structures and fewer legacy systems, can often integrate new technologies faster, helping offset wage pressures, tariffs and other input costs.

For advisors, this reframes AI as more than a growth catalyst. In the mid-cap space, it can also serve as a margin defense mechanism, a distinct advantage in today's inflationary environment.

The Advisor Blind Spot

Despite this resilience, mid-caps remain underrepresented in many advisor portfolios. In consultations, we often find they make up less than 5% of total equity exposure, typically buried in broad blend sleeves.

This is usually unintentional, driven by the gravitational pull of large-cap benchmarks like the S&P 500. But under-weighting to mid-caps leaves portfolios overly concentrated at the top of the market and missing out on a segment that combines profitability, adaptability and more attractive valuations.

A Streamlined Approach to Mid-Cap Allocation

For advisors looking to restore balance, the path doesn't need to be complicated:

- Carve out a sleeve for mid-caps rather than letting them get lost inside blend funds.

- Rebalance over-weights to large caps to create more even exposure across the size spectrum.

- Consider valuation and style balance to ensure mid-caps play their full role between growth-heavy large caps and more volatile small caps.

For example, funds that emphasize shareholder yield and quality screens, like the WisdomTree U.S. Value Fund (WTV), offer one way to reintroduce mid-caps thoughtfully. But more important than any single vehicle is the principle of giving mid-caps deliberate space in a portfolio, rather than letting them remain an afterthought.

The Case for Mid-Caps in 2025

Mid-caps aren't just a bridge between large and small. They are a distinct asset class with unique advantages. Their ability to maintain profitability under tariff and inflation pressures, coupled with the potential to harness AI as both a growth engine and a cost-defense tool, makes them well-suited for today's market environment.

After years of being overlooked, mid-caps may be ready to re-enter the spotlight. For advisors seeking resilience, diversification and balance, this is a segment worth revisiting.

For those interested in more insights like this on asset allocation and practice management, make sure to register for the Modern Advisor Playbook LinkedIn Newsletter, authored by Ryan and rotating guest WisdomTree thought leaders.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Funds focusing their investments on certain sectors increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility. While the Fund is actively managed, the Fund’s investment process is expected to be heavily dependent on quantitative models and the models may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All