Executive summary

In this paper, we:

- Revisit our 2024 research paper on asset performance in interest-rate-cutting cycles to compare our outlook to how equity and fixed income markets actually performed

- Give an update on the current global rate-cutting cycle, as many central banks have continued cutting rates during the Federal Reserve’s pause

- Review the performance of equities in the eight previous historical periods when the Fed paused in the middle of a rate-cutting cycle and later resumed cutting

- Review the performance of fixed-income assets in the same eight periods of a Fed pause

- Review the macro backdrop of the eight periods to consider GDP growth, earnings growth and equity valuations

- Offer conclusions

Revisiting our 2024 analysis

Almost one year ago, we published “How Equities and Treasuries Performed in Rate-Cutting Cycles.”

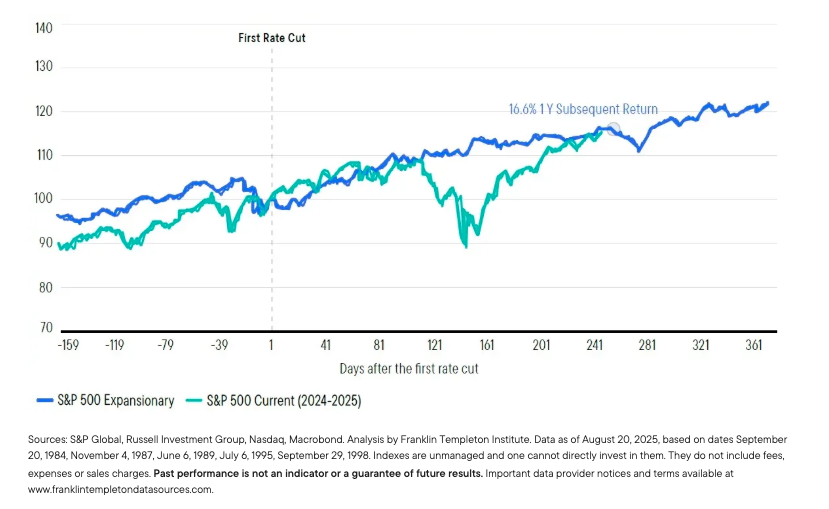

At the time, our analysis showed that during expansionary easing phases—periods when the Federal Reserve (Fed) cut rates while gross domestic product (GDP) growth was positive—equities have historically delivered strong returns. The past year has confirmed that pattern once again: Since the first rate cut of this cycle in August of 2024, the S&P 500 has risen by roughly 16%, broadly in line with historical performance during prior expansionary easing episodes.

Exhibit 1: This Year, S&P 500 Performance Matched the Historical Average for First Rate Cuts during Expansions

Growth of US$100 Invested at the First Rate Cut

With this backdrop, the logical next question to ask is, “What comes next?”. Having paused after cutting interest rates in September, November and December 2024, the Fed is once again approaching a potential policy inflection point to resume cuts, and investors are increasingly focused on the timing and consequences of additional policy easing in the second half of 2025. Recent market pricing reflects that anticipation—fed funds futures currently imply more than two full cuts of 25 basis points (bps) by year-end and that they will most likely happen in September and December.1

In this paper, we examine how financial markets and the broader macroeconomic backdrop evolve when the Fed resumes cutting rates after a pause. Following an update |on global central bank easing over the past year, we turn to past rate cuts after a pause, structuring our analysis in three parts:

- Equity performance following an interest-rate cut after a pause

- Fixed income performance following a rate cut after a pause

- Macro backdrop: GDP, earnings, valuations

Conclusions

- Equities appear likely to grind higher amid rising volatility. Not all cuts are the same. Early cuts in a cycle historically have been bullish and come with relatively low volatility. Interest-rate cuts after a pause, by contrast, have been typically associated with higher short-term volatility, but they have nonetheless averaged strong one-year returns across equity styles. On average, the Russell 2000 Index small caps gained about 20% and the Nasdaq Composite technology stocks gained about 25% one year after such cuts

- Fixed income also benefits. Fixed income has historically participated in these rallies as well, with US Treasuries returning around 6% and corporate bonds around 8% in the year following a pause-cut

- GDP growth has typically continued, and although corporate earnings have made only minor progress, price multiples have expanded significantly. Post-pause cuts have often coincided with P/E multiples expanding by over 20% within the first year, underscoring the powerful role of monetary easing in driving equity prices higher despite economic challenges.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Endnotes

1Source: Bloomberg. August 29, 2025.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

The allocation of assets among different strategies, asset classes and investments may not prove beneficial or produce the desired results.

Equity securities are subject to price fluctuation and possible loss of principal.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls. Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default.

Performance of the fund may vary significantly from the performance of an index, as a result of transaction costs, expenses and other factors.

Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges.

Large-capitalization companies may fall out of favor with investors based on market and economic conditions.

Small- and mid-cap stocks involve greater risks and volatility than large-cap stocks.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

© Franklin Templeton

Read more commentaries by Franklin Templeton