AI Data Center Building Spree Hits $40 Billion in a Single Month

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsOne of the most critical resources in 2025 is compute power. Chips and the data centers that house them have become the 21st-century equivalent of refineries and power plants, and governments are increasingly treating them as such.

Policymakers around the globe, from Washington to London to Beijing, are pouring billions into semiconductors and cloud infrastructure, not only to gain an economic edge but also to lead in artificial intelligence (AI).

Just look at OpenAI. Earlier this month, the company signed one of the largest cloud contracts in history with Oracle—$300 billion worth of computing power spread across roughly five years. The deal will require 4.5 gigawatts of power capacity, or the equivalent of more than two Hoover Dams, if you can believe it.

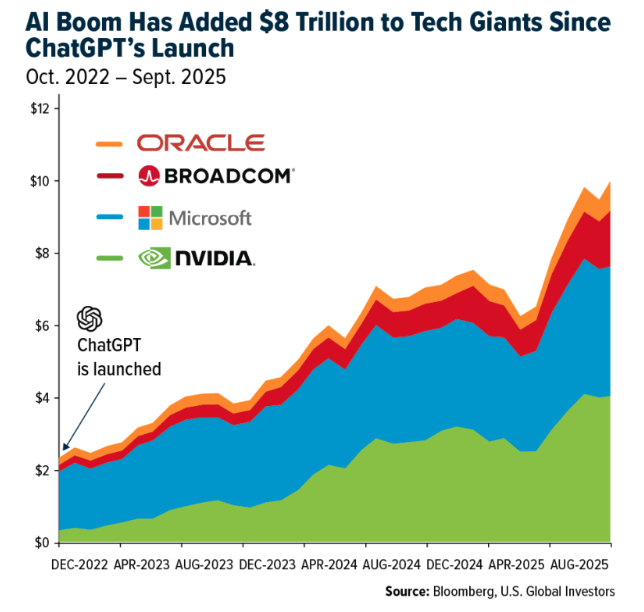

OpenAI’s spending spree has been the rising tide that’s lifted all boats in tech. Since ChatGPT burst onto the scene in late 2022, the market caps of Nvidia, Microsoft, Oracle and Broadcom have swelled by a staggering $8 trillion. That, of course, is a big reason why the Nasdaq and S&P 500 have continued to hit record highs this year.

Billions Flowing into Data Centers

The AI revolution has ignited an unprecedented building spree in U.S. data centers. According to Bank of America, construction spending hit an all-time high of $40 billion in June alone, representing a 30% increase from the year before. That’s on top of a 50% surge in 2024.

Washington isn’t sitting on the sidelines. Just ask BAE Systems. With funding from the CHIPS Act, the London-based defense contractor is currently modernizing its 110,000-square-foot Microelectronics Center in New Hampshire. The facility is one of the few domestic foundries specializing in military-grade semiconductors, producing specialized chips for applications ranging from secure communications to next-generation fighter jets.

By investing in fabricators, the U.S. is strengthening its supply chain and ensuring that the military gets the technology it needs to fight 21st-century wars.

Governments Supporting AI Technology

Last month, Intel made a historic deal with the Trump administration. The government announced it would take an $8.9 billion equity stake in Intel, in addition to billions in CHIPS Act grants. (And just this week, Nvidia said it would be investing $5 billion in the struggling tech firm.)

I believe the message is loud and clear: Semiconductors are strategic assets like oil and critical metals, and Washington is willing to invest taxpayer money to support them.

Across the pond, the UK is also ramping up AI investment. Microsoft announced plans to invest $30 billion by 2028 to build the country’s largest supercomputer, equipped with more than 23,000 Nvidia GPUs. Google, Nvidia, OpenAI and Salesforce are also pledging billions. All combined, tech giants are pouring more than $40 billion into the UK’s AI infrastructure.

Nvidia, Broadcom and AMD Fight for Industry Dominance

So who’s making the chips behind the revolution?

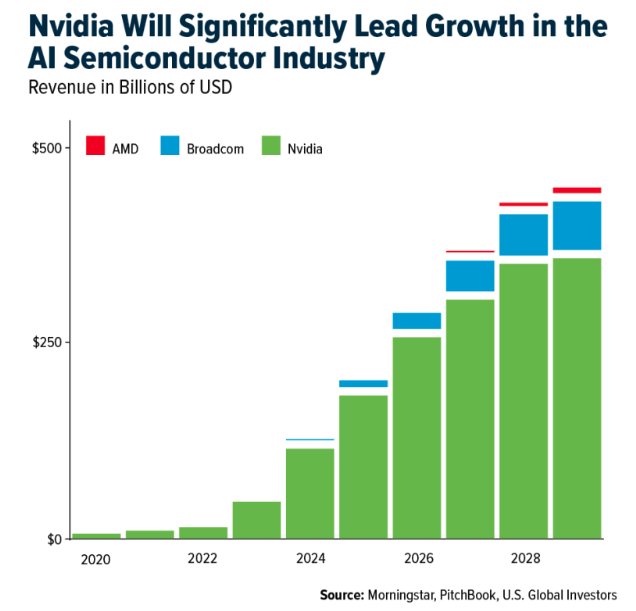

Nvidia remains the undisputed king, according to Morningstar. The financial services firm projects that AI chip revenue will quadruple over the next several years, with Nvidia leading the way.

But they’re not alone. Broadcom is carving out a strong second position, while AMD is battling for share in general-purpose GPUs.

Biblical Amounts of Energy Will Be Needed

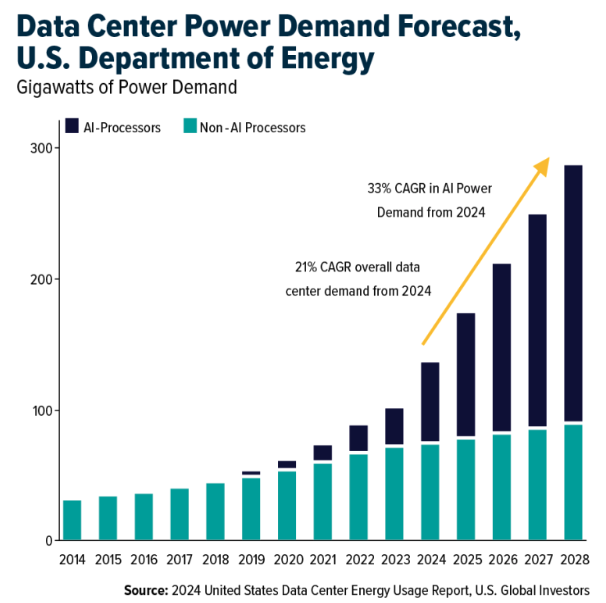

As impressive as these chips are, they demand enormous amounts of energy. The Department of Energy predicts AI-specific electricity use will grow at a mind-boggling 33% each year, far exceeding past norms.

The entire AI ecosystem relies on whether we can build and deliver enough electricity to feed it, which is why I think investors should be paying as much attention to power grids and cooling systems as they are to chip stocks. I said as much in an article last month.

High-Tech Military Applications

The connection between semiconductors and defense is only increasing. As I’ve been writing about recently, global defense budgets are expanding rapidly. PwC estimates that military spending will grow from just under $3 trillion in 2024 to potentially $4 trillion by 2030, with an increasing portion of that allocated to high-tech systems like drones, satellites, autonomous ships and AI-enabled fighter jets.

Is AI Contributing to the Labor Market Slowdown?

Overlay all of this with the macro picture. The labor market appears to be softening. Job openings are declining, and small businesses are cutting back on wage hikes. CEOs across industries are talking about white-collar automation.

In my mind, this creates a paradox: AI is being sold as a productivity booster at a time when the economy is moderating. Historically, periods of weak labor demand have often coincided with waves of automation. It’s no coincidence that businesses are investing so heavily in AI just as hiring slows.

That said, I would urge investors to recognize that compute is the new energy. Nations are stockpiling it, and companies are monetizing it. Just as oil defined the 20th century, I believe compute will define the 21st. The question isn’t whether to get exposure, but how.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.05%. The S&P 500 Stock Index rose 1.31%, while the Nasdaq Composite climbed 2.21%. The Russell 2000 small capitalization index gained 2.20% this week.

- The Hang Seng Composite gained 0.43% this week; while Taiwan was up 0.41% and the KOSPI rose 1.46%.

- The 10-year Treasury bond yield rose 5 basis points to 4.126%.

Airlines and Shipping

Strengths

- The best-performing airline stock for the week was Bombardier, up 14.3%. In the Australian domestic market, fares are currently up 8% year-over-year (Qantas +8%, Virgin +6%), while market capacity is up 3% year-over-year (Qantas +2%, Virgin +3%), according to UBS.

- According to Morgan Stanley, U.S. trade lanes were up 8% week-over-week and have increased for three consecutive weeks. U.S. lanes are up 28% month-over-month, indicating that trade volumes are starting to improve.

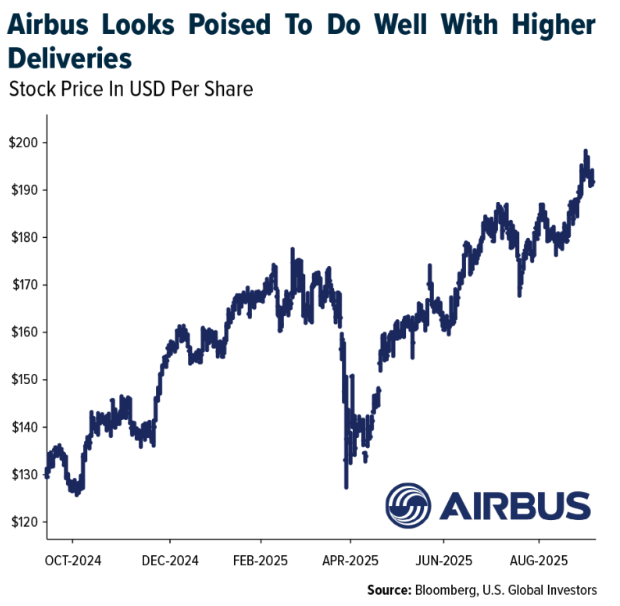

- Airbus deliveries appear to be sharply improving. Cirium reports 22 deliveries month-to-date for Airbus, which, assuming normal seasonality, suggests 86 deliveries this month compared to 50 in 2024. Intra-month seasonality has been stronger this year, with 61 deliveries recorded in July versus 47 in July 2024.

Weaknesses

- The worst-performing airline stock for the week was Alaska Air, down 9.7%. In China, domestic demand during August remained soft despite aggressive year-over-year pricing cuts by airlines. Load factors continued to rise year-over-year for China Eastern, Spring Airlines, and Air China, but this failed to translate into higher margins, according to Morgan Stanley.

- A Nikkei report on September 13 indicated that Nippon Express expects to book losses of about ¥9 billion for fiscal year 2024/25 in connection with a voluntary retirement program that has reportedly attracted over 300 applicants. There has been no official statement from the company yet.

- Azul has requested approval from the New York court to return three additional aircraft and one engine as part of its Chapter 11 restructuring, bringing the total to 12 aircraft and seven engines returned so far. The airline aims to reduce its future fleet by 35%, focusing on phasing out older Embraer models and renewing its fleet with E2 aircraft to improve operational efficiency, according to JP Morgan.

Opportunities

- Over 25% of Southwest Airlines’ cabins will be sold as extra legroom seating starting January 27, 2026. The airline currently holds about 18% of domestic capacity, so transitioning one-quarter of their supply to a higher fare category will reduce main cabin supply by 4.5 percentage points. According to TD, this offers attractive potential for rising main cabin unit revenues in 2026.

- Ocean container rates rose 7% sequentially following last week’s sharper increase. This two-week uptick comes after a consistent decline over the previous 11 weeks, according to Goldman Sachs.

- According to UBS, fare growth for bookings in August accelerated compared to July. Alaska Airlines saw the strongest acceleration in global fares, increasing by 880 basis points in August relative to July, followed by JetBlue with a 610-basis point increase. Five of the eight airlines UBS covers experienced a sequential increase in unique visitors to their apps in August versus July. Delta, United, Allegiant, and JetBlue showed the most significant acceleration in app usage.

Threats

- The ultra-low-cost carriers are aggressively adjusting capacity plans. Spirit is making the largest cuts at Boston (minus 52%), Philadelphia (minus 47%), and Atlanta (minus 44%). Frontier plans the most growth at Los Angeles (plus 138%), JFK (plus 73%), and Atlanta (plus 62%), while cutting capacity at San Jose (minus 28%), San Francisco (minus 21%), and Denver (minus 11%), according to TD.

- The Shanghai Containerized Freight Index (SCFI) fell 3.2% week-over-week for the latest week after remaining flat the previous week. The SCFI is a leading indicator of actual shipping rates, which impact carriers’ revenues and profits, according to Morgan Stanley.

- According to Morgan Stanley, street expectations for Spanish capital expenditure from 2027 to 2031 were €10.5 billion versus €12.9 billion announced by Aena. The bigger surprise is the €2.9 billion increase in ‘unregulated’ capital expenditure (retail, car parks, etc.). There will be questions about whether this can earn a 5% rate of return.

Luxury Goods and International Markets

Strengths

- Retail sales in the U.S. showed improvement in August, rising by 60 basis points. This uptick signals stronger consumer spending and suggests steady momentum in the retail sector, an encouraging sign for overall economic activity.

- The global personal luxury goods market has shown strong long-term growth, rising from €76 billion in 1996 to an estimated €369 billion in 2025, with projections reaching €480 billion by 2030. This steady expansion highlights a clear opportunity for investors and brands to benefit from sustained demand and resilience in the luxury sector.

- Cettire, an Australian online marketplace for luxury goods, led the S&P Global Luxury Index with a 32.9% gain. The stock rallied for the second week in a row without a clear news catalyst.

Weaknesses

- China released weaker economic data over the weekend, highlighting ongoing challenges in growth and demand. The softer figures have raised concerns about the strength of the country’s recovery, weighing on investor sentiment and increasing pressure on policymakers to consider additional stimulus measures.

- U.S. consumer sentiment declined for the second consecutive month in September, falling to 55.4 from 58.2 in August, according to the University of Michigan survey. This marks the lowest level since May.

- CityChamp Watch & Jewellery, a Hong Kong–listed jewelry and watch retailer, was the worst-performing stock in the S&P Global Luxury Index, dropping 11.9%. The stock corrected without a clear news catalyst.

Opportunities

- Tesla shares rose this week after Elon Musk purchased $1 billion worth of stock. Meanwhile, Tesla critic Gary Black pointed to two short-term catalysts that could further boost the stock: stronger Q3 deliveries driven by the expiring tax credit at the end of September, and the potential removal of safety monitoring requirements for robotaxis later this year.

- Marriott and Lufthansa have formed a joint venture that allows Marriott guests to earn Lufthansa Miles & More points when staying at Marriott hotels. This partnership makes it easier for travelers to collect airline miles through hotel bookings, adding extra value and rewards for frequent flyers and hotel guests.

- The Fed’s 25 basis point rate cut creates an opportunity for equities to move higher as borrowing costs ease and liquidity improves. Lower mortgage rates also support stronger consumer sentiment, boosting spending and housing demand, which could further fuel market momentum.

Threats

- The U.S. economy is increasingly reliant on the top 20% of earners, as the bottom 80% have only increased spending in line with inflation since the pandemic. This makes affluent households the key driver of demand, particularly in discretionary sectors. There is evidence that consumer sentiment among high-income Americans declined in August—for example, the University of Michigan’s survey showed the overall sentiment index dropped from 61.7 in July to 58.6 in August.

- RH CEO Gary Friedman warned that luxury furniture retailers must offer steep discounts to survive in today’s weak housing market, which he described as “the worst in my 38 years in this industry.” He noted that many upscale furniture makers are relying on 30–40% promotions and emphasized that “furniture… does not sell at full price” without risking bankruptcy. The company also cut its full-year sales outlook due to tariffs, and RH’s stock has fallen 42% year-to-date.

- Short sellers are mounting heavy bets against French luxury group Kering—short interest has reached approximately 10.7% of its publicly traded shares. This comes as Kering enters a leadership transition, with Luca de Meo beginning his role as CEO, amid concerns over high debt levels and declining sales at its flagship brands, Gucci and Saint Laurent.

Energy and Natural Resources

Strengths

- The best-performing commodity for the week was China Lithium Carbonate 99.5%, up 3.18%. Lithium prices in mainland China surged in August, with hydroxide jumping 26% month-over-month to exceed $11,000 per metric ton for the first time in over a year. However, BNEF expects these gains to fade in September as CATL’s mine restarts early and oversupply pressures return.

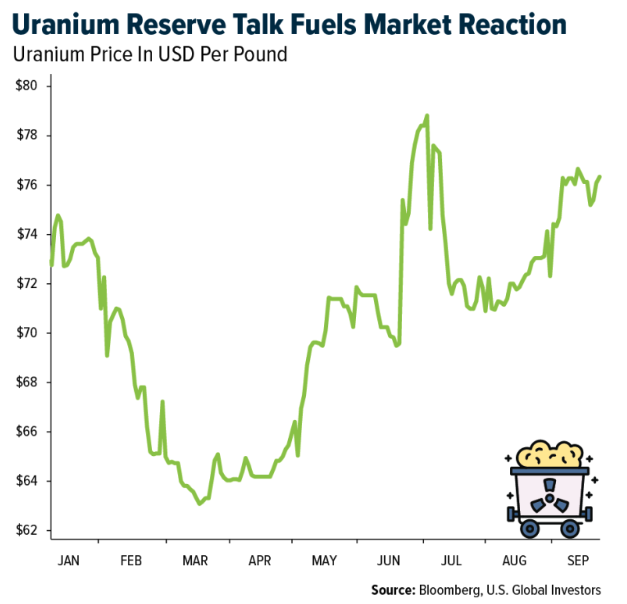

- The uranium story is gaining momentum as geopolitical tensions and clean energy investments renew interest in nuclear power, positioning uranium as a key element in future energy security. This momentum is supported by rising demand from utilities and strategic stockpiling worldwide, which could drive prices higher.

- Pakistan’s Economic Coordination Committee has approved final agreements and allocated $390 million in financing to fast-track the Reko Diq copper-gold project and a supporting railway. The move marks a major milestone in regional resource development and is expected to boost local employment while strengthening Pakistan’s role as a key supplier of critical base metals by the 2030s.

Weaknesses

- The worst-performing commodity for the week was coffee, down 7.65%. Coffee futures fell in both New York and London as expectations of a record Vietnamese crop and possible U.S. tariff exemptions on Brazilian imports eased supply concerns. Arabica dropped nearly 4%, while robusta fell almost 7%, with traders betting that renewed Brazil-U.S. trade flows could further loosen tight stockpiles.

- BHP announced plans to shut down the Saraji South coal mine in Queensland and cut approximately 750 jobs, citing high state royalties and unfavorable market conditions that make low-margin operations unsustainable. The move underscores ongoing challenges in the coal industry, despite efforts to shift toward energy-transition metals, and highlights the structural decline of thermal coal.

- The U.S. solar industry is facing major setbacks due to recent political and regulatory headwinds, resulting in project delays and an expected 20% decline in residential sector growth. These challenges are weakening investor confidence and slowing expansion at a critical time for renewables in the U.S. energy mix.

Opportunities

- Oilfield service companies are increasingly pivoting toward offering off-grid power solutions, especially for data centers supporting AI growth, as oil activity declines in mature fields. These modular systems can be rapidly deployed, providing a solution that bypasses traditional grid infrastructure but face risks such as fluctuating costs and long-term dependency on fossil fuels.

- Global investors are aggressively hedging against dollar weakness by purchasing derivatives, with estimates suggesting up to $1 trillion in dollar-hedged investments could be in place, exerting downward pressure on the U.S. dollar. This shift indicates a potential prolonged period of dollar depreciation, which could lead to increased capital flows into hard assets like commodities and gold, supporting prices.

- Ivanhoe Mines announced a $500 million strategic private placement with the Qatar Investment Authority (QIA), significantly bolstering its financial resources to advance large-scale mineral projects in Africa and beyond. This move demonstrates confidence in the mining sector’s growth prospects amid a challenging geopolitical and market environment.

Threats

- Rising U.S. dollar hedging activity, fueled by investor fears of potential policy shifts, may extend the dollar’s decline, adversely affecting U.S. assets, exports, and global trade balances. This dynamic could contribute to heightened currency market volatility and increased costs for dollar-based commodities.

- France is set to add only about 500 megawatts of wind power capacity this year, the smallest increase in 20 years, due to political opposition led by the anti-immigration National Rally party, which hampers renewable energy permits. This political climate risks stalling France’s renewable targets and impeding progress toward its climate commitments.

- A BHP Group joint venture in Argentina is investing over $400 million to prepare for permit approvals for a multibillion-dollar copper project, amid hopes of making the Vicuña deposit a major regional hub. Political uncertainties, regulatory hurdles, and policy shifts, despite incentives like Argentina’s Rigi program, pose risks to project development and the country’s attractiveness as a resource destination.

Bitcoin and Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Aster, rising 857%.

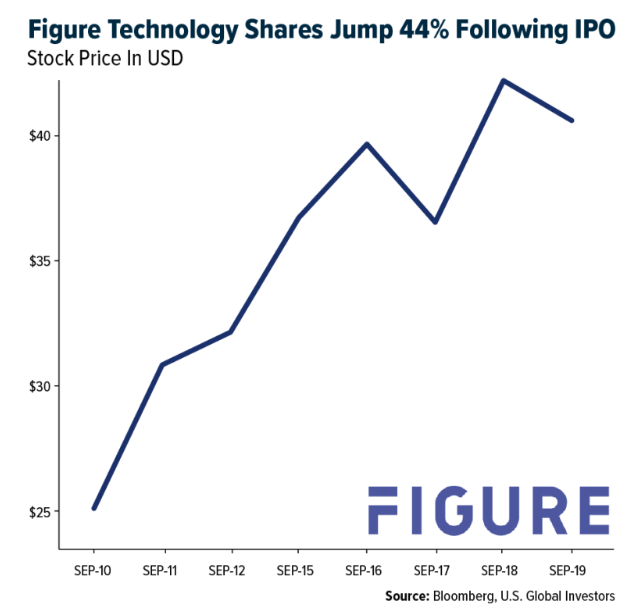

- Figure Technology Solutions shares opened 44% above their IPO price after raising $785.5 million in its listing. The opening price gives the company a market value of approximately $7.6 billion based on outstanding shares. It develops blockchain technology to facilitate loans, according to Bloomberg.

- Tether Holdings SA is reentering the U.S. market with ambitions to become the leading stablecoin issuer in the country. Its goal is to replicate its overseas success in the U.S., where it has been largely absent for years after paying a fine to settle allegations of misrepresenting its reserves, according to Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was MYX Finance, down 27.55%.

- The trustee-controlled bankruptcy estate for SafeMoon US LLC has agreed to pay an estimated $12 million to a class of investors who allege they were defrauded through the sale of the company’s crypto token, according to Bloomberg.

- Jim Chanos criticized Michael Saylor for what he called “financial gibberish,” following reports that Saylor may sell Bitcoin or Bitcoin options to fund dividend payments for securities issued to acquire the cryptocurrency, according to Bloomberg.

Opportunities

- Banco Santander SA’s online bank, Openbank, has launched retail cryptocurrency trading, marking the latest move by a major European financial institution into digital assets. The service will roll out to Openbank customers in Spain in the coming weeks, according to Bloomberg.

- Thai authorities plan to move forward with easing restrictions that would allow foreign tourists to convert digital assets into baht to cover travel expenses—regardless of any changes in government leadership, according to the Thai SEC and Bloomberg.

- Binance Holdings is nearing a potential agreement with the U.S. Justice Department that could remove a key oversight requirement from its settlement over allegations it failed to adequately prevent money laundering, Bloomberg reports.

Threats

- Memecoin traders are trying to profit from the shooting of Charlie Kirk. Evan Rademaker, a 30-year-old executive, checked the memecoin market after hearing about the incident and noticed tokens associated with Kirk appearing on PumpFun. He invested $30,000 in one such token, but it quickly plummeted, resulting in a $17,000 loss.

- The European Union is preparing to block Russian crypto transactions, marking the first time sanctions have directly targeted cryptocurrency platforms. Digital asset services will be included in the EU’s latest round of financial sanctions against Russia, according to Bloomberg.

- Canadian authorities have seized more than 56 million Canadian dollars in cryptocurrency from the Trade Ogre exchange, marking the country’s largest crypto confiscation and the first complete takedown of a digital asset platform. Working with blockchain analytics firm Arkham Intelligence, investigators traced illicit transactions linked to the exchange, according to CoinPedia.

Defense and Cybersecurity

Strengths

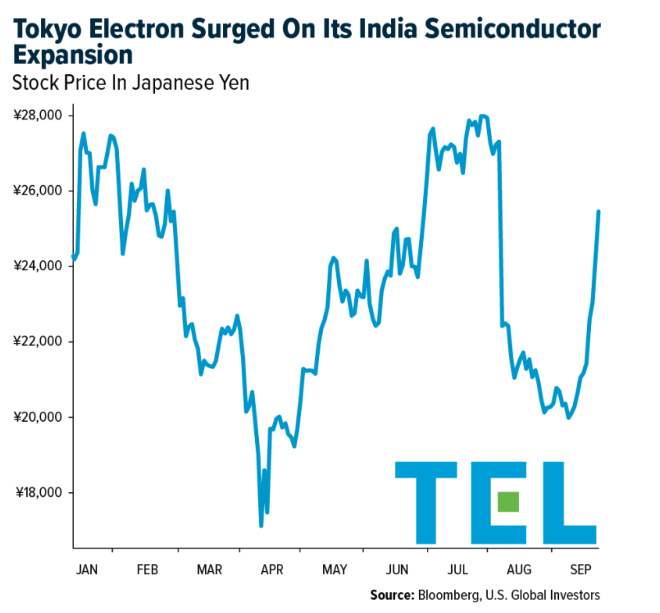

- Tokyo Electron jumped this week as investors cheered its expansion into India’s fast-growing semiconductor ecosystem and its role in new chipmaking initiatives like JOINT3. This highlights the company’s strategic importance in the global supply chain. The rally was further supported by easing concerns over a trade-secret case, plus broader optimism in semiconductor equipment demand from AI and advanced chip investment.

- Nvidia is investing $5 billion in Intel, acquiring about a 4% stake at $23.28 per share. The partnership will see Intel develop custom CPUs and SoCs for Nvidia’s AI infrastructure and PC chips that integrate Nvidia’s RTX GPU technology.

- The best-performing stock in the XAR ETF this week was Kratos Defense, up 16.59%, after unveiling the Mighty Hornet IV attack drone in partnership with Taiwan’s National Chung-Shan Institute of Science and Technology at the Taipei Aerospace & Defense Technology Exhibition. The drone showcases cost-efficient, high-performance capabilities for global defense markets.

Weaknesses

- China’s competition regulator has launched an antitrust probe into Nvidia, saying the company violated conditions tied to its 2020 Mellanox acquisition. The move highlights Beijing’s growing scrutiny of foreign chipmakers amid escalating U.S.–China tech tensions.

- Germany has enough arsenal for only four weeks to fend off attacks by Russian drones, the CEO of Quantum Systems said. The head of one of Europe’s largest unmanned systems manufacturers called for the urgent ramp-up of serial drone production in Germany.

- The worst performing stock in the XAR ETF this week was Rocket Lab, declining 10.42%, after an SEC filing revealed that an insider sold 1,873,097 shares worth about $90.3 million, leaving 173,920 shares under indirect control.

Opportunities

- Australia is investing A$12 billion over the next decade to upgrade Perth’s Henderson Defence Precinct in support of nuclear-powered submarines under AUKUS, expand its shipbuilding capacity, and strengthen long-range strike capabilities in response to China’s growing presence in the Pacific.

- Palantir Technologies has achieved CMMC Level 2 certification, affirming its ability to manage Controlled Unclassified Information for the U.S. Department of Defense and other federal programs.

- CrowdStrike is significantly enhancing its AI security capabilities through strategic partnerships with NVIDIA and Salesforce, as well as the acquisition of Pangea to bolster its Falcon platform with advanced AI-powered detection and response features.

Threats

- Germany’s Green Party is urging the government to block a planned French-Russian nuclear project in Lingen, warning it could give Moscow access to sensitive facilities and create new dependencies—despite Germany’s recent exit from nuclear power.

- Tensions between the U.S. and China are escalating as Representative John Moolenaar has called for restrictions on Chinese airlines’ landing rights in response to China’s limitations on rare earths and magnets, potentially impacting international trade and relations.

- Russia and Belarus have launched the large-scale “Zapad-2025” military drills, involving about 100,000 troops and nuclear-capable systems. The show of force is raising tensions with NATO and highlighting growing risks along Europe’s eastern borders.

Gold Market

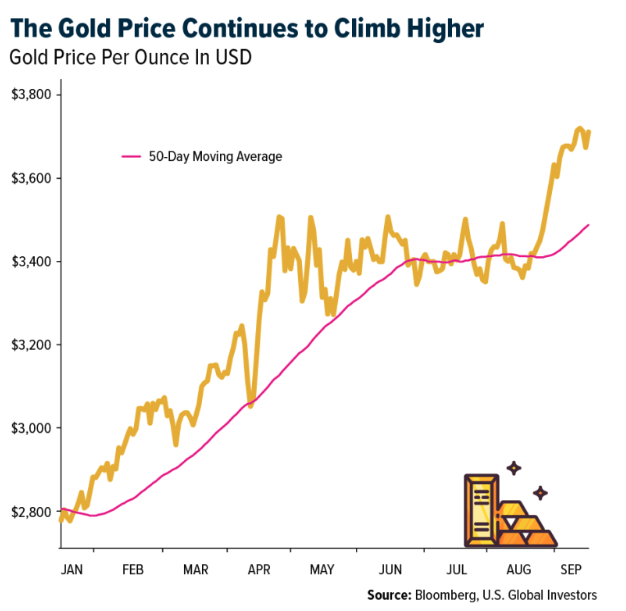

This week gold futures closed at $3,711.40, up $25.00 per ounce, or 0.68% and Bitcoin was down 0.56%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher/lower by 2.53%. The S&P/TSX Venture Index came in up 2.26%.

Strengths

- The best-performing precious metal for the week was silver, up 0.70%, with Friday’s gains nearly three times those of gold. Investors are starting to notice silver’s historic 3-to-1 beta relative to gold. Gold inched higher as traders weighed the Fed’s rate-cut outlook, with bullion hovering just below recent record highs at week’s end. While lower rates support the metal, a stronger dollar following Powell’s cautious remarks limited further gains.

- According to a Bank of America analyst, gold broke out from a triangle consolidation and reached a new all-time high of $3,674 on September 8. Further declines in yields and/or the dollar could push prices toward upside targets of $3,735, $3,790, $3,935, and $4,000. In recent years, price leadership has gradually shifted from the futures market to physically backed ETFs, which have seen steady inflows lately.

- Zijin Gold Int. Co. Ltd. is raising HK$25 billion ($3.2 billion USD) in a Hong Kong IPO, the largest globally since May, with trading set to begin Sept. 29. Strong demand saw the share sales quickly covered, backed by cornerstone investors including GIC, BlackRock, and Fidelity.

Weaknesses

- The worst-performing precious metal for the week was palladium, down 6.13%. The USITC has launched the final phase of its investigation into Russian palladium imports, ruling that U.S. producers were materially harmed by subsidized and unfairly priced shipments. The case, initiated by Stillwater Mining and the United Steelworkers Union, could lead to antidumping and countervailing duties if confirmed by the Commerce Department.

- According to Stifel, B2Gold’s 2025 production guidance has been lowered to 80,000–110,000 ounces (from 120,000–150,000 ounces) due to a crushing capacity shortfall at the processing plant, along with challenges commissioning a new mine. This represents a 30% reduction from the mine’s original guidance.

- Bank of America, speaking at the Mining Forum Americas, indicates producers are showing modest cost discipline slippage as cut-off grades are lowered to increase metal production. They also note that intense competition for royalty and streaming deals is driving down returns, making more transactions dependent on higher gold prices.

Opportunities

- Equinox Gold Corp. announced the first gold pour at its Valentine Gold Project, located in Newfoundland and Labrador, Canada. Management also noted that commissioning is progressing well, with throughput averaging 47% of nameplate capacity for the first 15 days of operation, positioning the project to ramp up to its nameplate capacity of 2.5 million tons per year, according to Canaccord.

- According to Raymond James, Barrick Mining Corp. has announced an updated Preliminary Economic Assessment (PEA) on Fourmile. The PEA indicated Fourmile could have average annual gold production of 600,000 to 750,000 ounces per year at mining rates of 1.5 to 1.8 million tons of ore per year, with over 25 years of mine life. The PEA estimates project capital at $1.5 to $1.7 billion, cost of sales at $850 to $900 per ounce, and all-in sustaining costs (AISC) of $650 to $750 per ounce.

- RBC is encouraged by Artemis Gold Inc.’s announcement of a planned 33% increase in Phase 1 processing capacity at Blackwater to 8 million tons per year by Q4 2026, along with long-lead orders placed ahead of the Phase 2 expansion. In their view, this outlines a near-term accretive catalyst through a low-capital optimization, providing an incremental benefit to project economics ahead of the now further de-risked Phase 2 expansion decision.

Threats

- Canaccord believes consensus already expected Gold Road Resources Ltd. to miss guidance for calendar year 2025. They still see some risk to production in the second half of 2025, given the implied grades required to hit the bottom end of guidance.

- With the recent rally in gold, gold equities have experienced significant buying pressure, pushing up valuations. As a group, the intermediate gold producers in Scotia’s precious metals coverage universe are now trading at a spot price-to-net asset value (P/NAV) of 0.82x, above the long-term average of 0.81x for the first time since February 2021.

- Global gold ETF inflows slowed from recent weeks but remained strong at $2.01 billion. Notably, China returned to net inflows for the first time in six weeks. Silver ETFs saw net outflows of 7.6 million ounces last week, led by Europe, according to BMO.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2025):

Qantas Airways Ltd.

Airbus SE

Air China Ltd.

Nippon Express Holdings

Embraer SA

Southwest Airlines

JetBlue Airways Corp.

Delta Air Lines

United Airlines

Allegiant Travel Co.

Tesla

Kering

Ivanhoe Mines

Alphabet Inc.

B2Gold

Barrick Mining Corp.

Artemis Gold

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The Shanghai Containerized Freight Index (SCFI) is a weekly index that tracks spot freight rates for container shipping from Shanghai to various global destinations, serving as a key indicator of shipping market conditions.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits