I Called for $4,000 Gold. Now I See It Going (Much) Higher

Membership required

Membership is now required to use this feature. To learn more:

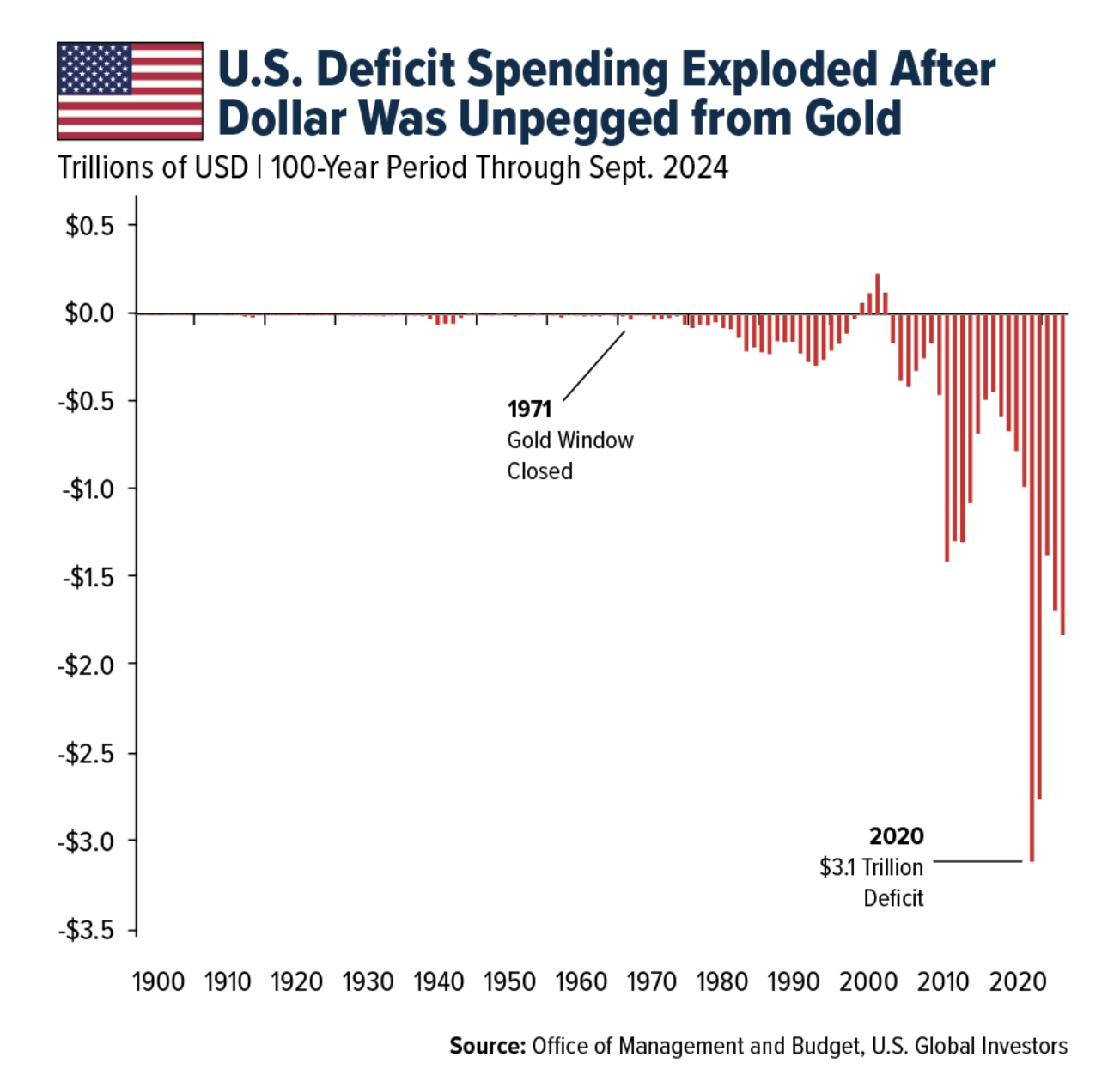

View Membership BenefitsIt was a sleepy Sunday in the middle of summer. Most Americans were tuned in to Bonanza when President Richard Nixon interrupted the broadcast to announce that he was suspending the U.S. dollar’s convertibility into gold

At the time, the “Nixon Shock,” as it came to be known, may have looked like a simple adjustment to the global monetary order.

In reality, it was the day the U.S. traded fiscal discipline for a floating exchange rate.

Before 1971, every dollar in circulation was ultimately tied to something real and tangible. Thirty-five dollars could be exchanged for one ounce of gold. After 1971, “printed paper currency really had no value of its own. It was artificial, and anything that’s artificial is temporary.”

That’s from 1971: How All of America’s Problems Can Be Traced to a Singular Day in History, a new book on the subject that I strongly recommend readers pick up. Its authors, Paul Stone and Dave Erickson, argue that the unraveling of the dollar’s link to gold is at the root of America’s inflation and exploding debt, not to mention “unfettered moral decay, racism, rampant drugs, the destruction of the family, war and famine,” and more.

The Law of Intended Consequences

You’d be forgiven for challenging some of Stone and Erickson’s conclusions. There’s one thing, though, that we should all be able to agree on: Once the dollar was unpegged from gold, governments began to spend without limit. Politicians no longer had to make hard choices. Instead of cutting spending or raising taxes, they could simply run deficits and let the Federal Reserve finance the shortfall.

That may have been the point all along! Stone and Erickson write that Nixon and his advisors believed the gold standard was hamstringing U.S. power, and that by severing ties with gold, they could outspend the Soviet Union, dominate the world and, I quote, “control everybody.”

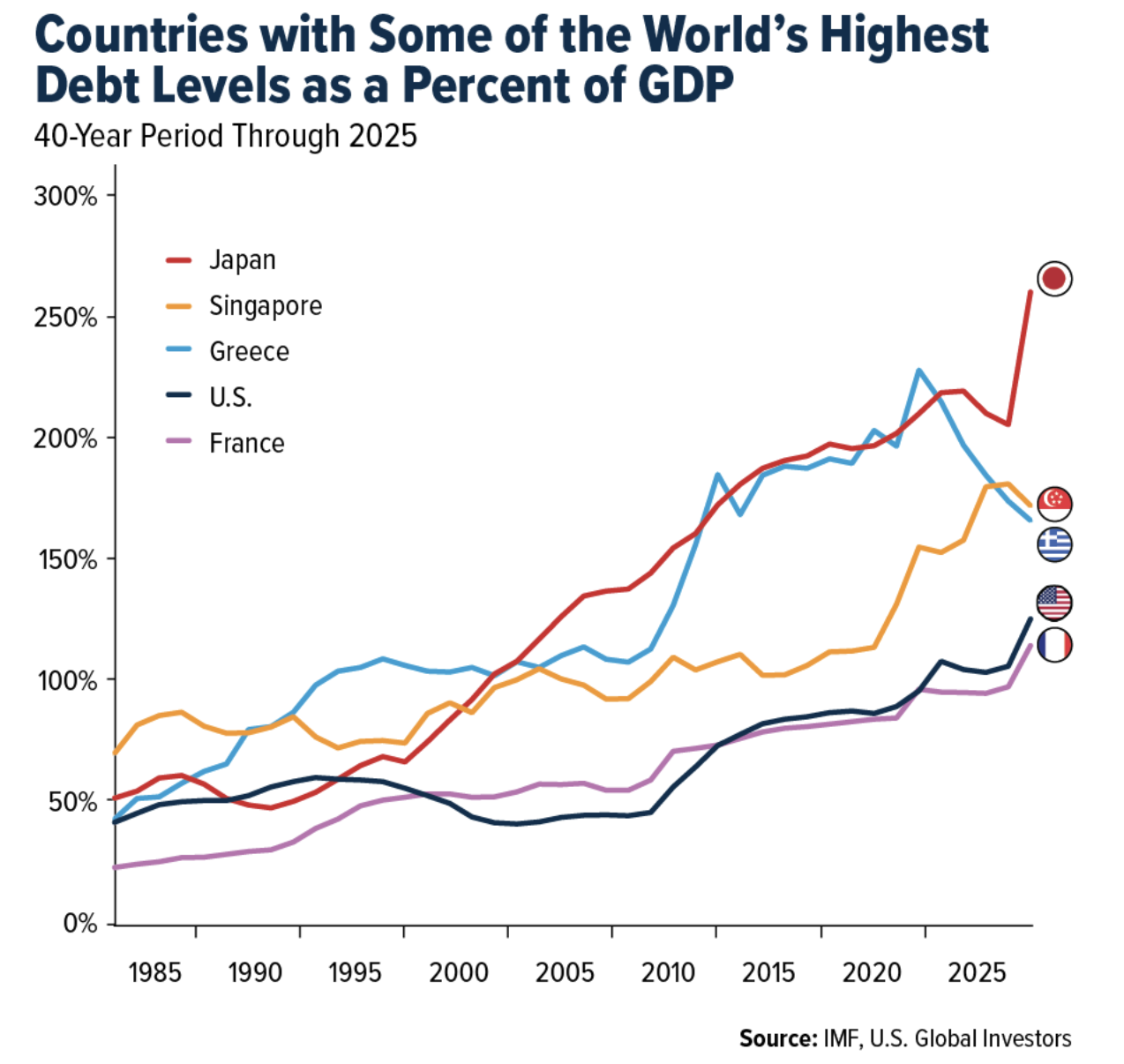

Fast forward 55 years, and U.S. government debt now stands at a jaw-dropping $37.5 trillion, equal to roughly 124% of GDP. Globally, debt has ballooned to $324 trillion, more than 235% of world GDP, according to the Institute of International Finance (IFF). For comparison’s sake, when Nixon closed the gold window, U.S. debt was around $400 billion, not even 40% of GDP.

Meaning that in just over five decades, we’ve gone from a system of fiscal restraint to a free-for-all.

Real Money Is Finite

For years (decades?), I’ve argued that gold is the ultimate hedge against runaway debt and monetary mismanagement. Back in 2020, I went on CNBC Asia and called for $4,000 gold, a target that’s now within reach.

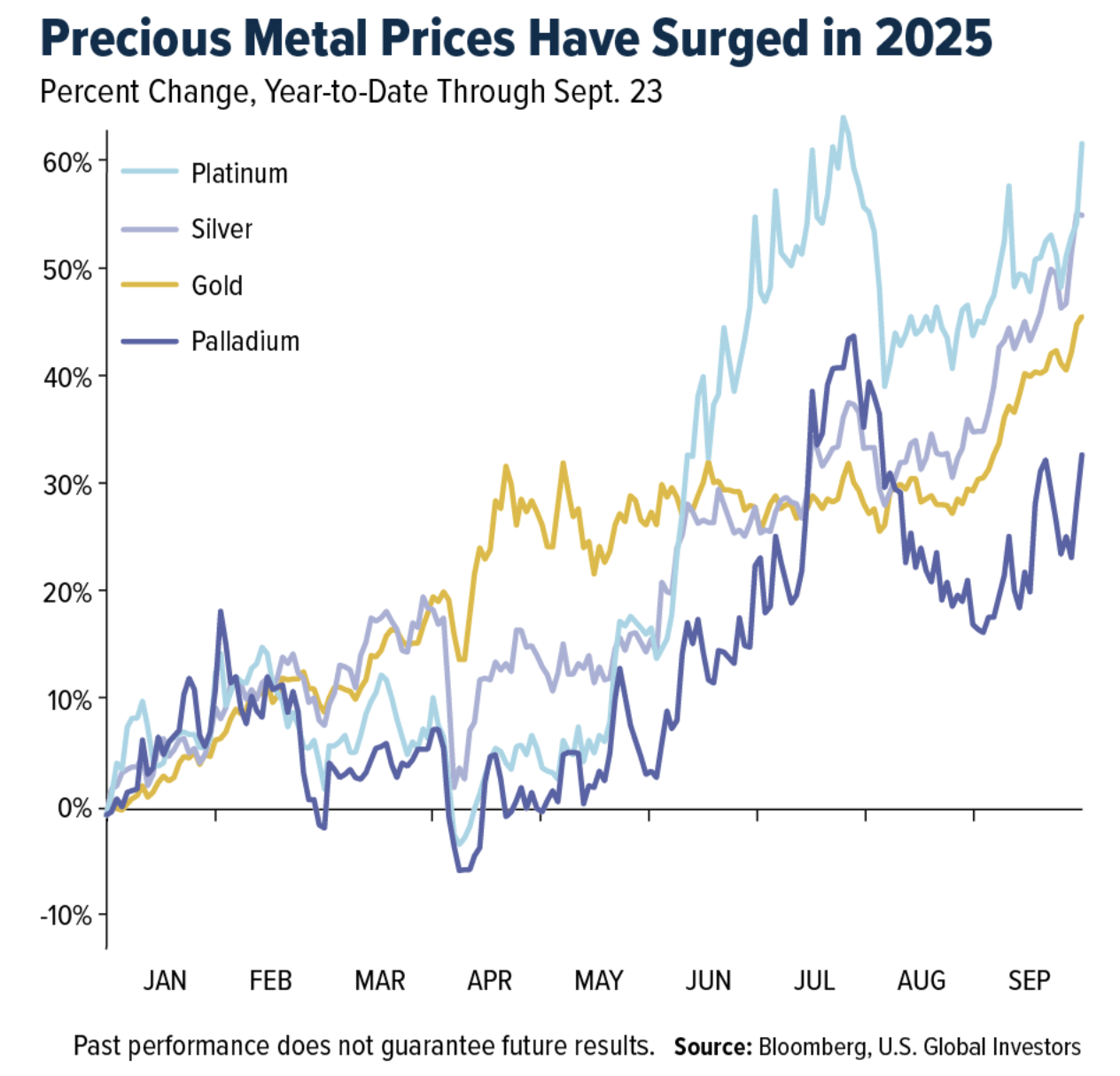

This year, the metal has surged past $3,700 an ounce, hitting all-time highs as the dollar has suffered its steepest decline in two decades. Traders are now pricing in multiple rate cuts from the Fed.

Meanwhile, central banks continue to trip over themselves to add bullion to their reserves, purchasing a net 200 metric tons in the first seven months of the year. That represents a modest 4% increase over the amount purchased during the same period the previous year, according to World Gold Council (WGC) data. Bank governors understand that fiat money can be printed at will, but real money—gold—is finite. You can’t print it, and you can’t sanction it.

I believe this is why gold is now the second-largest reserve asset in the world, behind only the dollar. But unlike the dollar, gold has no counterparty risk.

Don’t Sleep on the Other Precious Metals

It’s not just gold. Silver, platinum and palladium have also been on a tear this year. Silver is up more than 50%, platinum 65%, palladium 35%. Barron’s recently noted that palladium, still trading at a steep discount to gold and platinum, could be in the early stages of another run higher, with Bloomberg’s Mike McGlone forecasting a move back toward its all-time high above $3,400.

The Era of Record Debt Levels

Contrast that with today’s overextended stock market. Margin debt, or money investors borrow from their brokers to speculate, has soared to a record $1.06 trillion, up nearly 33% from a year ago. As you can see in the chart below, spikes in margin debt have often preceded major market corrections. I’m not suggesting we’ll see a similar crash this cycle, but it’s worth keeping in mind.

Governments are overleveraged, households are stretched and now investors are taking on an inadvisable amount of debt just to keep the party going. When the margin calls come, you don’t want to be the one left holding the bag. As I see it, you want to be holding gold.

My New Projection: $7,000 Gold

So where does the yellow metal go from here?

My new projection is $7,000 per ounce gold, potentially by the end of President Trump’s second term.

My reasons are simple. The debt pile is unfathomably massive, and it’s accelerating. Fiscal imbalances are widening, and monetary policy is being constrained. The Fed can’t raise rates aggressively without bankrupting the government, but it also can’t make deep cuts without tanking the dollar.

Both options support higher gold prices, in my opinion.

Meanwhile, central banks continue to buy record amounts of bullion. Net inflows into North American gold-backed ETFs are having their second strongest year on record, according to the WGC. And retail demand in countries like India and China remains robust, driven by the Love Trade, which accounts for an estimated 60% of all gold purchases.

The 10% Golden Rule

As investors, we don’t have the luxury that Washington does. We can’t run endless deficits or print our own cash. (Life would be so much easier if we could!) On the contrary, we have to live within our means and balance our checkbooks.

That’s why I’ve always viewed gold as real money. It’s an anchor that has helped preserve purchasing power across every empire, every currency regime and every political cycle in history. Like Ray Dalio, I recommend a 10% weighting in gold, with half in physical bullion (coins, bars, jewelry, gold-backed ETFs) and the other half in high-quality gold mining equities. Remember to rebalance on a regular basis.

I called for $4,000 gold, and we’re nearly there. Looking ahead, I now see $7,000 gold on the horizon. That may sound bold, but in today’s high-debt environment, I believe the bold call might also be the prudent one.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.15%. The S&P 500 Stock Index fell 0.31%, while the Nasdaq Composite fell 0.65%. The Russell 2000 small capitalization index lost 0.59% this week.

- The Hang Seng Composite lost 1.21% this week; while Taiwan was up slightly 0.01% and the KOSPI fell 1.72%.

- The 10-year Treasury bond yield rose 4 basis points to 4.176%.

Airlines and Shipping

Strengths

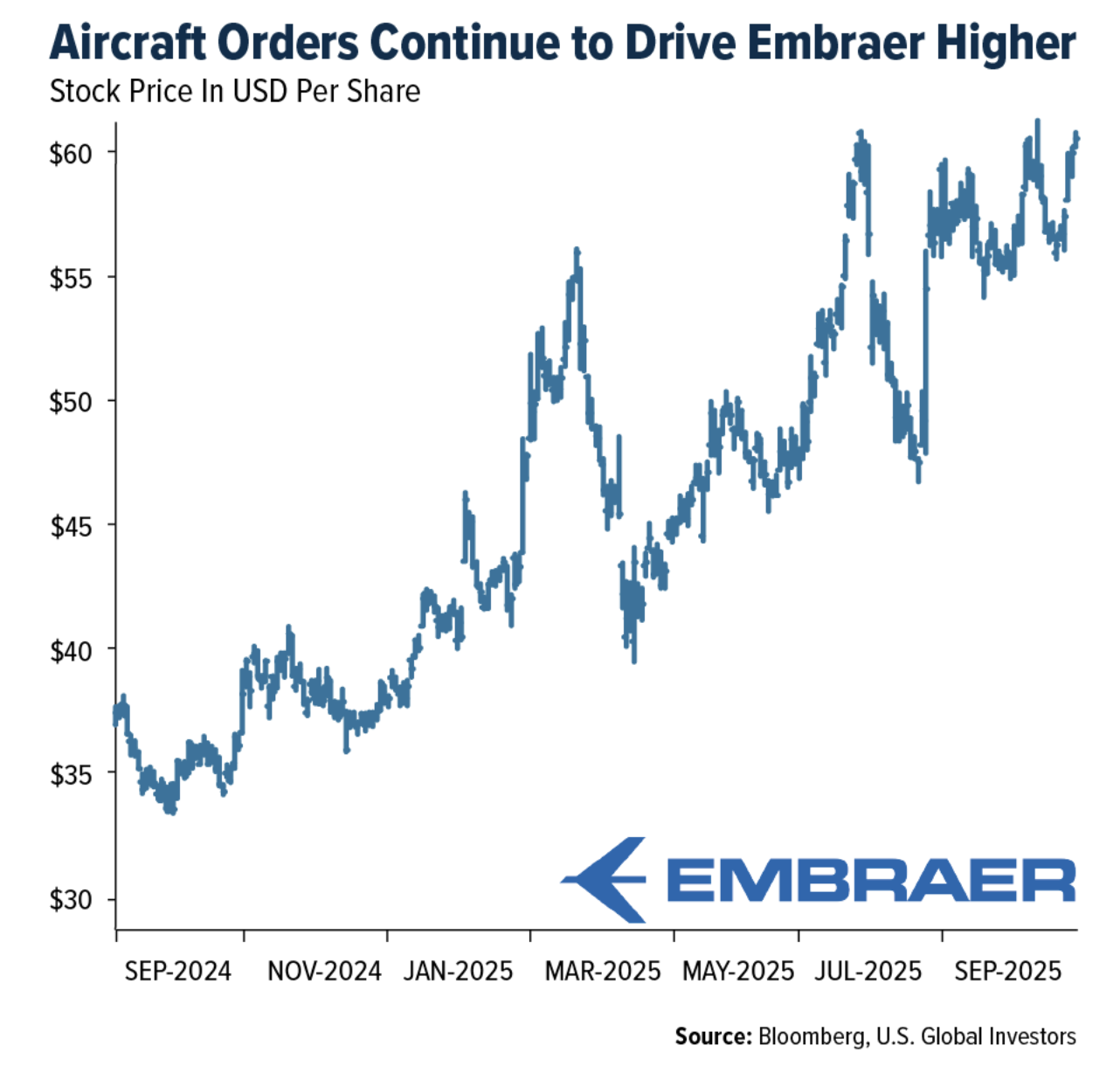

- The best-performing airline stock for the week was Embraer, up 4.6%. Cathay Pacific reported operational data for August 2025. Strength in passenger demand continued during the month, with group traffic up 35% year-over-year, outpacing the capacity expansion rate of 33%, according to UBS.

- Global new ship contract volume declined 18% month-over-month in August. The order book and newbuild prices remained largely flat. Profitability in the tanker and bulker segments is improving, with returns on investment now exceeding the threshold needed to trigger additional new ship orders, according to Goldman Sachs.

- August airfares experienced the strongest sequential increase since February 2023. According to the U.S. Bureau of Labor Statistics, airline fares rose 5.9% month-over-month in August, marking only the second increase in fares since the beginning of the year. This is also the first time a month-over-month increase has exceeded 5% since February 2023, according to Morgan Stanley.

Weaknesses

- The worst-performing airline stock for the week was Alaska Air, down 11.1%. Chinese airlines experienced a disappointing summer peak, with passenger traffic rising only 3.4% year-over-year. However, modest capacity growth of just 1% year-over-year helped boost the load factor to a new high of 87%. Despite this, domestic yield and unit revenue remained weak, down 9% and 8% year-over-year, respectively. According to Bank of America, the underperformance is largely due to high-speed rail diversion and sluggish business travel demand.

- China freight flows showed a sequential decline in laden vessels traveling from China to the U.S., down 7%. However, the year-over-year drop moderated slightly compared to the prior week (13% versus 21%), according to Goldman Sachs.

- Spirit Airlines restructured its lease agreement with AerCap. According to Goldman Sachs, Spirit will reject some aircraft while affirming others, will not take delivery of all 36 aircraft tied to 2024 sale-leaseback deals (with those slots now at AerCap’s discretion), will receive an undisclosed liquidity infusion, and AerCap will file a $696 million unsecured claim.

Opportunities

- Gatwick’s £2.2 billion airport expansion project will allocate £1 billion to runway improvements, with the remainder going toward terminal expansion, according to Morgan Stanley. London’s airspace has been slot-constrained for many years, making this a welcome development.

- UPS has announced its 2025 peak season surcharges. On average, surcharges will increase by 7% for large packages, 7% for packages requiring additional handling, 9% for those exceeding maximum size limits, and 4% to 9% based on how much a package exceeds baseline thresholds compared to last year, according to Morgan Stanley.

- Embraer announced a firm order of 24 E195-E2 aircraft from LATAM, adding $2.1 billion to its backlog at list prices. The order also includes options for an additional 50 E195-E2 aircraft, valued at $4.4 billion, according to J.P. Morgan.

Threats

- The UK government has approved the use of a second runway at London Gatwick, which could nearly double passenger capacity at the airport by the late 2030s. While the expansion presents potential growth opportunities for airlines, it also introduces the risk of increased competition for existing carriers, potentially reducing market share and scale advantages, which could put long-term pressure on fares, according to J.P. Morgan.

- The Shanghai Containerized Freight Index (SCFI) fell 14.3% this week, compared to a 3.2% decline the previous week. The SCFI is a leading indicator of actual shipping rates, which directly impact revenues and profits. Ocean container rates were down 7% week-over-week and remain under significant year-over-year pressure, down 69%, according to Morgan Stanley.

- Europeans are booking fewer trips to the U.S. this fall, with planned transatlantic travel down 11%, according to a major data provider, as concerns persist over President Donald Trump’s immigration and tariff policies. Air travel from Germany is expected to decline 13% year-over-year, followed by Spain at 9% and Italy at 7.6%. Bookings from the UK are down 4.9%, while France declined 2.9%, based on data from Cirium, an aviation analytics company.

Luxury Goods and International Markets

Strengths

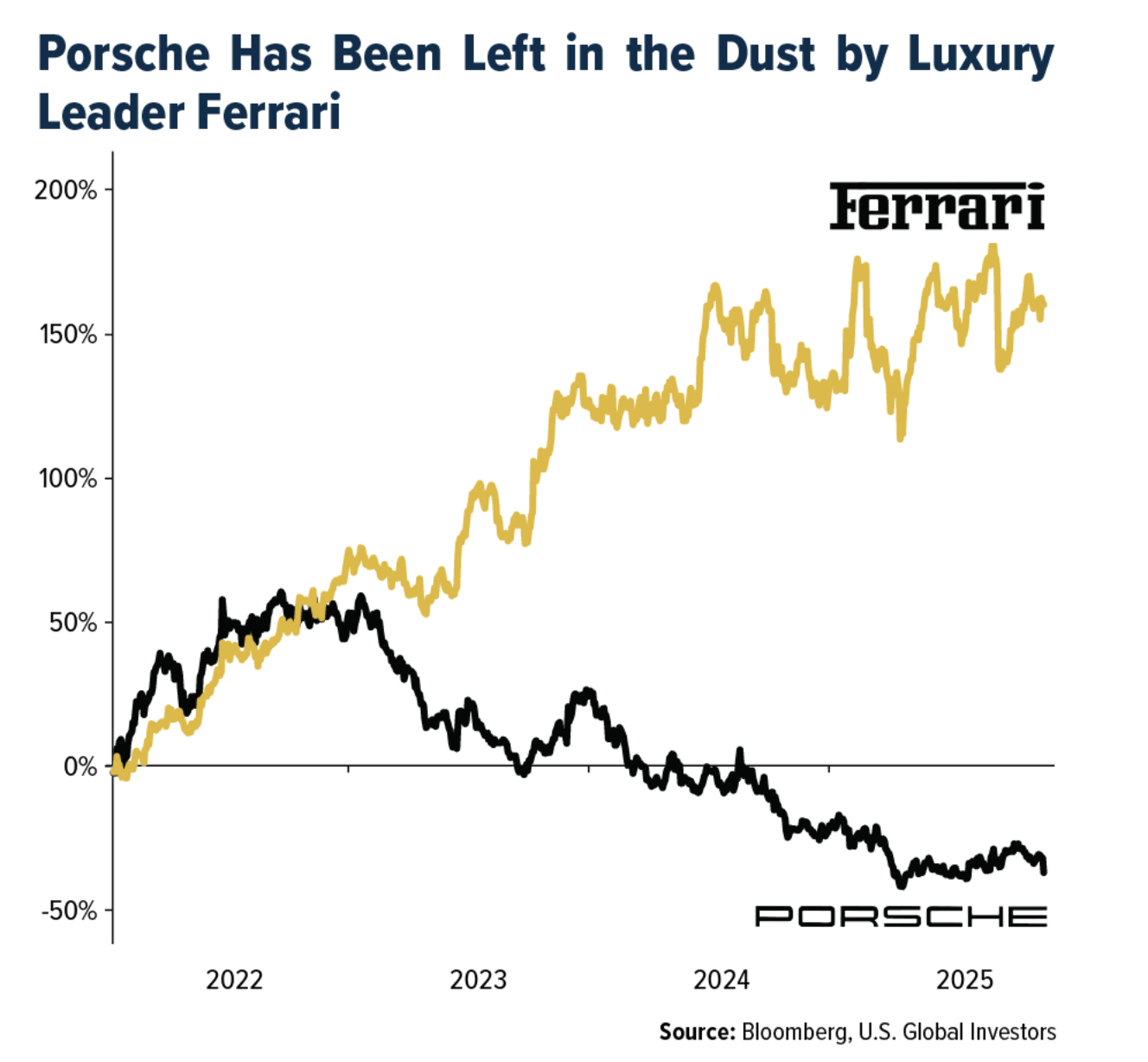

- Ferrari, the ultra-luxury carmaker, has significantly outperformed Porsche, whose shares are down 30% since its initial public offering (IPO) in September 2022. Ferrari’s consistent financial performance, strong brand equity, and ability to maintain high demand even in challenging market conditions, highlight its resilience and competitive edge in the luxury automotive sector.

- Moody’s has affirmed LVMH’s Aa3 long-term credit rating with a stable outlook, highlighting the company’s strong financial position and consistent operating performance. The affirmation reflects confidence in LVMH’s ability to manage debt, sustain cash flow, and navigate volatility in the luxury goods sector.

- Cettire, an Australian online luxury marketplace, led the S&P Global Luxury Index with a 35.8% gain. Shares surged after CEO Dean Mintz purchased over 10 million shares on the open market, signaling strong insider confidence and sparking investor optimism, momentum trading, and short covering.

Weaknesses

- Porsche announced it will slow down electric vehicle production due to weaker demand, particularly in key markets such as China and the United States. The automaker also lowered its profitability forecast for the current year to a maximum of 2%, down from the previously projected target of 5–7%.

- The Eurozone’s preliminary September Manufacturing PMI, released on September 23, declined to 49.5 from 50.7 in August, falling below the 50 threshold and indicating a contraction in the sector.

- Brunello Cucinelli, the Italian luxury fashion house, was the worst-performing stock in the S&P Global Luxury Index, falling 19.8%. Shares tumbled Thursday after short-seller Morpheus Research alleged the company continues to sell products in Russia despite EU sanctions, offers steep discounts, and has merchandise appearing in discount chains like TJ Maxx.

Opportunities

- RBC has projected 10% revenue growth for Hermès, highlighting the brand’s strong momentum in the luxury sector. The forecast reflects Hermès’ enduring appeal, resilient demand for its iconic products, and its ability to consistently deliver solid performance even in a challenging global market.

- According to September filings, Elon Musk could receive a record $1 trillion payout if Tesla’s market capitalization reaches $8.5 trillion. With Tesla currently valued at about $1.43 trillion, the company would need to grow nearly eightfold for Musk to unlock the award, underscoring both the ambitious growth expectations tied to Tesla and the extraordinary scale of his performance-based compensation plan.

- Milan Fashion Week (September 23–29) offers luxury companies a major opportunity to showcase new collections, attract global media attention, and engage with buyers and high-net-worth clients. Featuring 55 physical runway shows and several digital presentations, the event draws a global audience of media, influencers, and industry leaders, boosting brand visibility and supporting future sales and partnerships.

Threats

- Stellantis will temporarily pause production at several European plants due to weak demand. Shutdowns include Italy’s Pomigliano plant, idling Fiat Panda and Alfa Romeo Tonale lines from September 29, and multi-week pauses at France’s Poissy plant in October. The company is also delaying some model launches and adjusting output to market conditions.

- Poland’s closure of its border with Belarus is set to disrupt a key trade route for goods entering the EU from China. This could slow shipments of high-end products like luxury fashion and electronics, forcing companies to use longer, costlier routes and adding strain to EU supply chains.

- Cartier announced a U.S. price increase on September 25, 2025, raising jewelry prices by up to 13% and watches by nearly 10%. While reinforcing Cartier’s luxury status, the hike risks pushing customers toward competitors, the secondary market, or reducing repeat purchases, potentially weakening long-term demand.

Energy and Natural Resources

Strengths

- The best performing commodity for the week was uranium, up 7.95%. Fortune Bay and Aero Energy have begun drilling at the Murmac uranium project in Saskatchewan, with Aero funding the program under its option agreement. Meanwhile, Centrus Energy is planning a multibillion-dollar expansion of its uranium enrichment facility in Ohio to reduce U.S. reliance on Russian imports. Both initiatives highlight how uranium projects advance only when economically viable—Murmac through cost-saving partnerships that avoid shareholder dilution, and Centrus with Department of Energy-backed funding aimed at accelerating domestic nuclear fuel production.

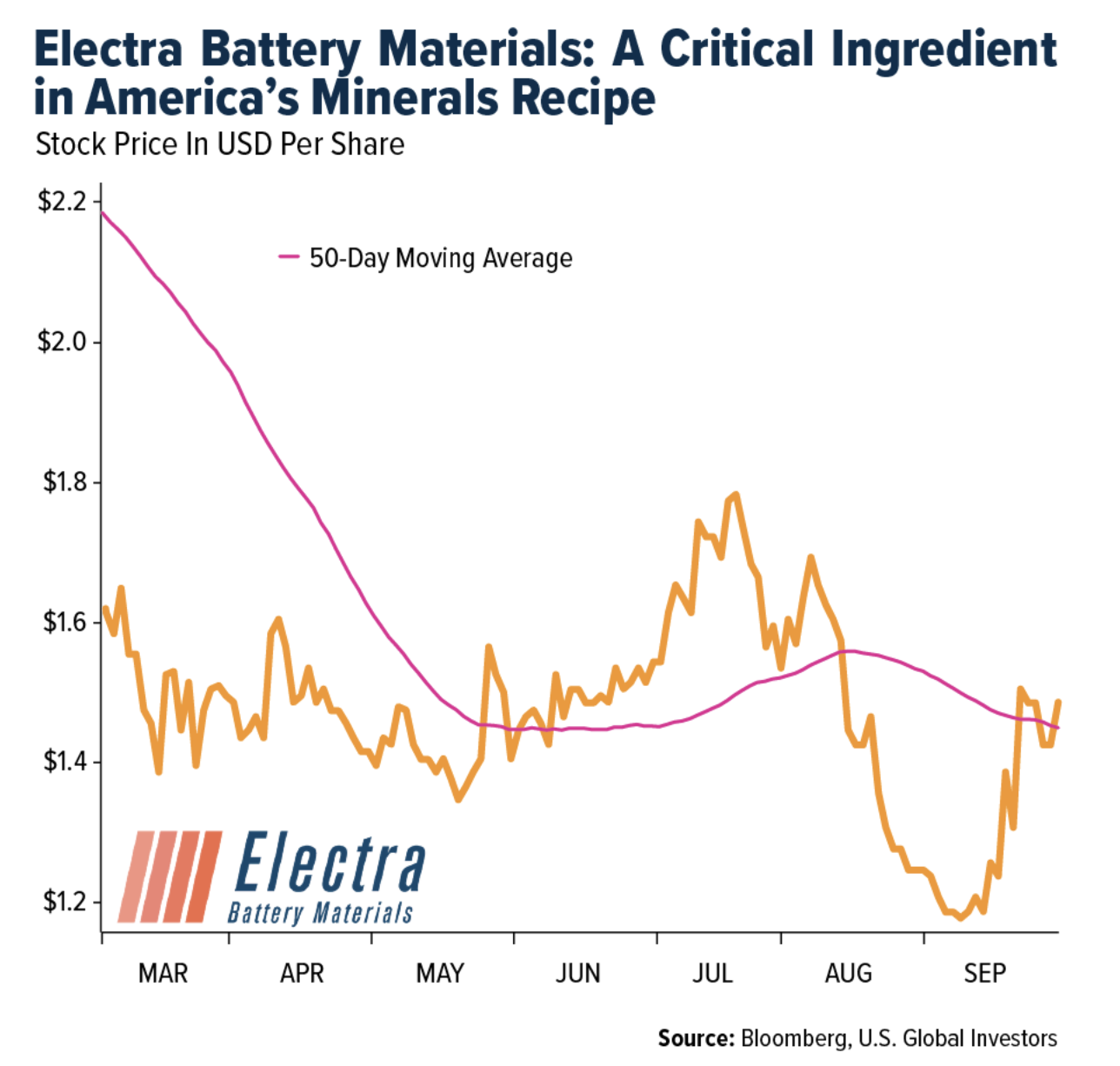

- Electra Battery Materials is increasingly seen as a strategic player following prior Department of Defense funding, raising the possibility of additional support similar to deals struck with Lithium Americas and MP Materials. Supporting this bullish outlook, HC Wainwright & Co. recently reiterated a Buy rating with a $2.20 price target, reflecting confidence in Electra’s central role in U.S. critical minerals policy and its strong market positioning.

- Ørsted’s shares surged after a U.S. judge ruled that construction on a nearly completed Rhode Island wind farm could resume, countering efforts by the Trump administration to halt the project. The ruling allows Ørsted to continue work during ongoing legal challenges and offers reassurance to investors amid a broader push to stabilize its U.S. offshore wind ventures.

Weaknesses

- The worst performing commodity for the week was natural gas, down 1.84%. Natural gas prices weakened as sanctioned Russian Arctic LNG 2 shipments continued despite U.S. restrictions, highlighting ongoing geopolitical risks in global supply chains. Additionally, winter ice conditions are expected to limit exports from the project in the coming months, adding uncertainty and potential volatility to LNG flows.

- Pennsylvania Governor Josh Shapiro has threatened to secede from the PJM power grid if it fails to implement reforms to lower soaring energy costs, which have reached a record $16.1 billion this year—despite a price cap negotiated after previous hikes. The summit highlighted rising demand from data centers, clean energy mandates, and infrastructure growth, with states considering leaving PJM or forming alternative systems if they are not granted more influence.

- U.S. electricity prices have surged at more than twice the rate of overall inflation, driven by rising demand from sectors such as artificial intelligence, manufacturing, and electric vehicles. This has sparked political concern as affordability becomes a key issue, prompting calls for reforms to networks like PJM Interconnection. Leaders, including Pennsylvania Governor Josh Shapiro, are exploring measures to cut costs amid ongoing debates about the impact of renewable energy policies on pricing.

Opportunities

- Botswana’s President Duma Boko aims to finalize a deal by the end of October 2025 to acquire a majority stake in De Beers from Anglo American Plc, which is selling its 85% stake amid a diamond market slump. Botswana, already owning 15%, is negotiating with financing partners, including Oman’s sovereign wealth fund, to boost its stake above 50% and gain greater control of the diamond supply chain.

- Quant firm Squarepoint has rapidly expanded into physical commodities trading, becoming a major player in cobalt and actively trading aluminum, copper, and other metals through its offshoot, STG. The firm uses advanced algorithms, proprietary data, and in-house financing to execute multi-year supply deals involving transportation, storage, and global delivery.

- Global energy storage demand is expected to more than double to 360.2 GWh by 2027, driven by growing adoption in China, the U.S., Europe, and emerging markets aiming to improve grid flexibility. Citi analysts have raised earnings forecasts and target prices for Chinese ESS producers Ningbo Deye and Sungrow, citing rising regional demand and market expansion.

Threats

- Alcoa’s CEO warns that the 50% import tariffs on aluminum could hurt demand for U.S.-produced metal, as higher prices are passed on to domestic buyers and consumers. Despite solid order books, the tariffs are driving up costs and weighing on demand, with Alcoa’s shares down over 17% this year.

- The Democratic Republic of Congo may raise its cobalt export quotas if foreign companies—such as CMOC—agree to increase local processing. The country’s mines minister outlined plans to lift a recent export ban and introduce a quota system aimed at strengthening resource control and supporting domestic industry development.

- Oil prices have fallen for five straight days, with Brent nearing $66 per barrel and WTI around $62, due to rising global supply. Expectations of resumed Iraqi exports via Kurdistan and increased output from OPEC+ and other producers have raised concerns of a surplus, outweighing geopolitical risks.

Bitcoin and Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Aster, rising 193%.

- A tight circle of crypto power players, including Mike Novogratz and Dan Morehead, are shaping the digital-asset treasury boom, with around 85 public companies raising billions from investors, writes Bloomberg.

- Theta Capital Management is seeking to raise $200 million for its latest blockchain fund-of-funds. The fund will allocate capital to 10 to 15 venture firms specializing in digital assets and is targeting a net internal rate of return of 25%, writes Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was 0G, down 28%.

- Much of this year’s price buildup was fueled by crypto treasury firms—public companies that raised money to accumulate assets. Token purchases by these companies have slowed as falling share prices limited their ability to raise capital for new buying. The pullback has weakened demand and added to the pressure behind the latest plunge in digital assets, writes Bloomberg.

- An Ether whale took a multimillion-dollar loss on its bullish bet Thursday after the cryptocurrency’s price dipped below $4,000 for the first time since August 8. The whale, identified by the address Oxa523, had its leveraged bullish position worth 9,152 forcibly liquidated by the decentralized exchange Hyperliquid, according to blockchain analyst Lookonchain, writes Bloomberg.

Opportunities

- Tether Holdings SA is raising up to $20 billion in a private placement that could value the company at around $500 billion, making it one of the most highly valued private firms globally. The stablecoin issuer is leveraging its early lead to build a strong competitive advantage and amass a multibillion-dollar fund to invest across sectors like AI, crypto mining, and commodities, according to Bloomberg.

- Crypto market-maker GSR has filed to launch a fund called the GSR Digital Asset Treasury Companies ETF, which will bundle companies holding digital assets in their corporate treasuries into a single investment. The fund will also seek private investments in public equity, writes Bloomberg.

- SoftBank Group and Ark Investment Management are potential investors in a major funding round for Tether Holdings SA. The company is seeking $15 to $20 billion for about a 3% stake, which could value Tether at up to $500 billion, writes Bloomberg.

Threats

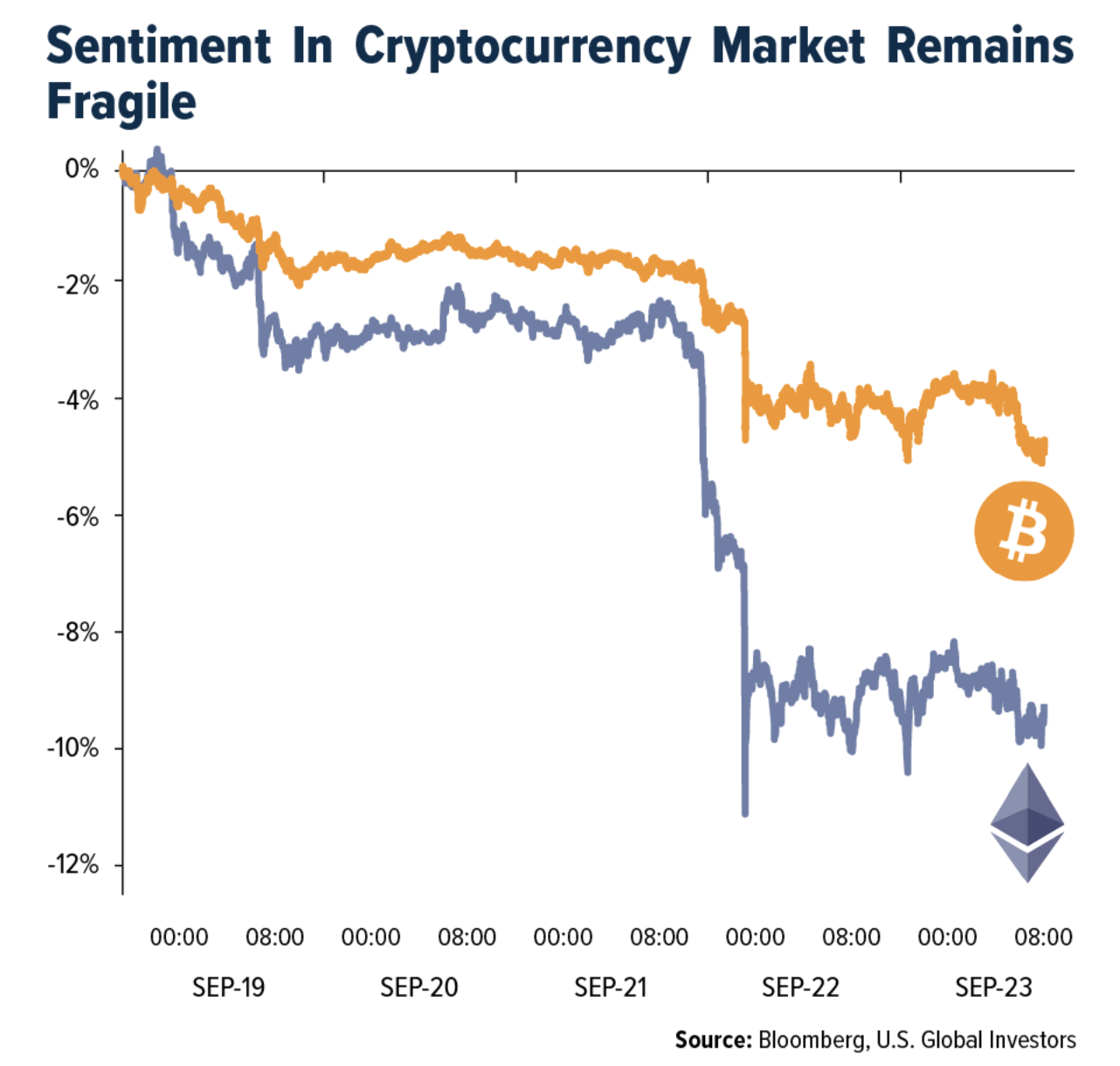

- Cryptocurrency traders saw more than $1.5 billion in bullish wagers liquidated on Monday, triggering a sharp selloff that sent Ether and other tokens plunging. This was the largest wave of liquidations across cryptocurrencies since at least March 27, according to Coinglass data reported by Bloomberg.

- Purchases by publicly traded digital-asset treasuries dropped from 64,000 Bitcoin in July to 12,600 in August, and 15,500 so far in September, according to CryptoQuant. Regulators are investigating unusual trading activity in digital-asset treasury shares, with some treasuries that raised money through PIPE deals seeing their shares fall as much as 97% below issue price, writes Bloomberg.

- Bitcoin and Ether extended losses amid a broader decline in risk sentiment, erasing over $140 billion in market value. Ether fell as much as 8.2% to below $4,000, its weakest level in nearly seven weeks, while Bitcoin slipped below $110,000 for the first time in four weeks, writes Bloomberg.

Defense and Cybersecurity

Strengths

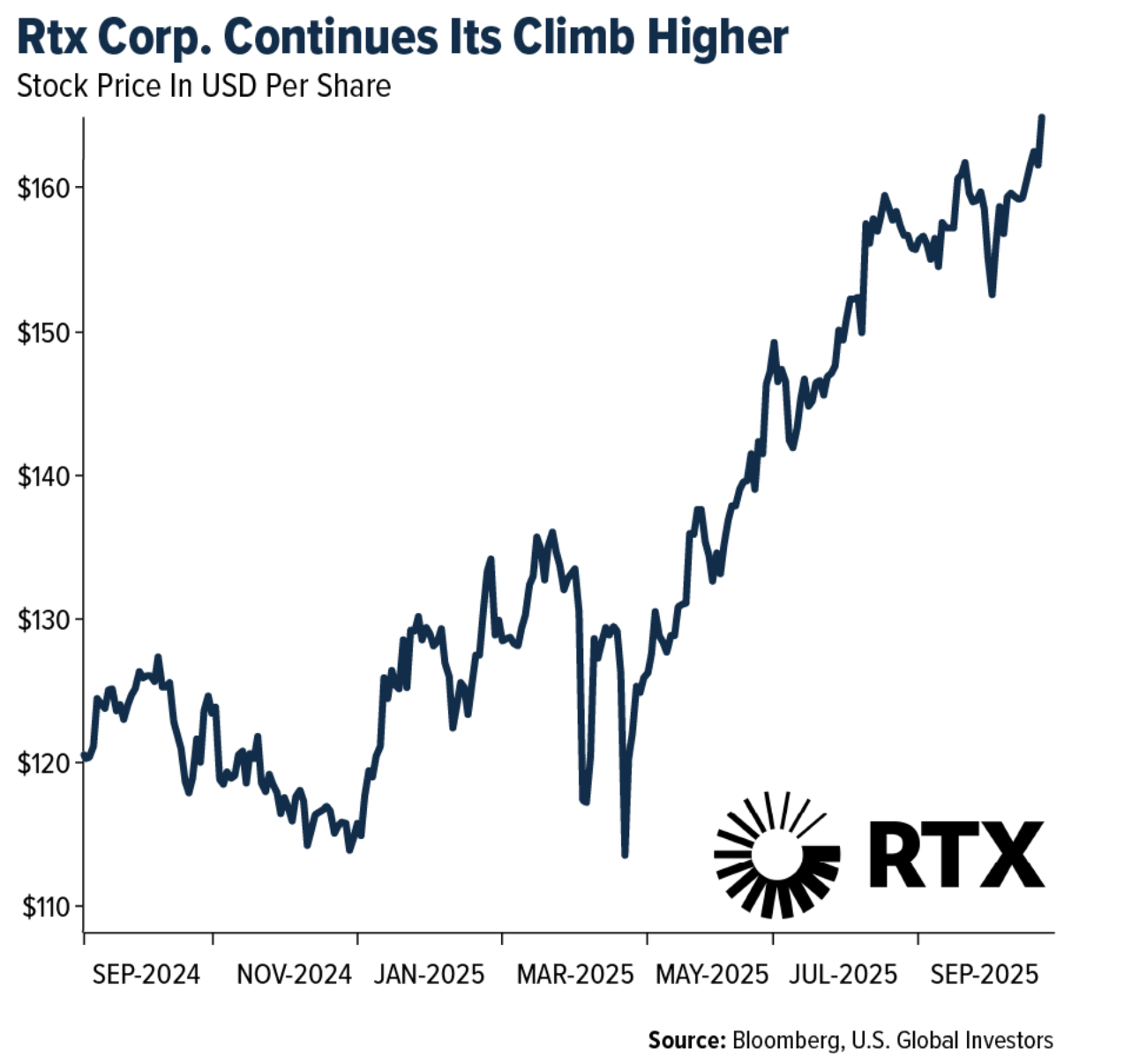

- The U.S. announced a $6.4 billion arms sale to Israel, including Boeing Apache helicopters and armored vehicles, while the State Department approved a $780 million sale of Javelin missile systems to Poland, with RTX Corporation and Lockheed Martin as contractors.

- Micron reported Q4 FY2025 revenue of $11.32 billion, up 46% year-over-year, with earnings per share of $3.03. For Q1 FY2026, the company expects $12.5 billion in revenue and gross margins above 50%, driven by strong AI data center demand, nearly $2 billion in high bandwidth memory sales, tight DRAM supply, and improved pricing and cost efficiency.

- The best-performing stock in the XAR ETF this week was AAR Corp, up 14.66% after reporting stronger-than-expected earnings, solid revenue growth, and announcing the acquisition of ADI. AAR’s stock climbed to record highs as investors responded positively to its expanding parts distribution business and improved outlook.

Weaknesses

- Hackers exploited the Oracle Database Scheduler’s External Jobs feature to infiltrate corporate networks, bypassing perimeter defenses and executing commands with OracleJobScheduler service privileges. This allows attackers to establish encrypted tunnels to external servers and deploy ransomware, highlighting the need for enhanced access controls and monitoring.

- The European Union has launched an investigation into major tech companies, including Microsoft, to assess their compliance with the Digital Services Act in preventing online financial fraud. This could have significant implications for regulatory compliance and operational practices.

- The worst-performing stock in the XAR ETF this week was Axon Enterprise Inc., down 8.54% after announcing the acquisition of Prepared, an AI-powered 911 communication company. Investors were spooked by concerns over execution risks and valuation.

Opportunities

- The Technology Prosperity Deal between the U.S. and the U.K.—which includes a commitment from the U.K. to purchase over $80 billion in products from U.S. tech and defense companies, including Palantir—is a significant development.

- General Dynamics was awarded a $1.5 billion contract to modernize IT capabilities for U.S. Strategic Command, while China added several U.S. companies, including Huntington Ingalls Industries, to its export control list, restricting dual-use item exports.

- The U.S. Air Force selected RTX and Shield AI to add autonomous software to two new fighter drones, enabling them to fly as “loyal wingmen” alongside manned aircraft. One prototype flew in August, with the second expected in October, though the Air Force has not officially confirmed the selection.

Threats

- Russia recently violated Estonian airspace with three MiG-31 jets near Vaindloo Island, while U.S. fighters intercepted Russian aircraft in Alaska’s air defense zone. Denmark also briefly closed airspace over Copenhagen and Aalborg due to drone activity, highlighting rising pressure on NATO’s northern borders.

- Western researchers suggest Russia has been supplying China with airborne assault equipment, vehicles, and training that could enhance Beijing’s ability to conduct large-scale amphibious operations. While Taiwan is not mentioned directly, the capabilities align with a potential invasion scenario.

- State-linked threat actors—including the Iranian group Nimbus Manticore—targeted job seekers with fake offers to deploy advanced malware like MiniJunk and MiniBrowse, affecting critical sectors in Europe and the Middle East.

Gold Market

This week gold futures closed the week at $3,804.90, up $99.10 per ounce, or 2.67%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 3.38%. The S&P/TSX Venture Index came in up 3.11%. The U.S. Trade-Weighted Dollar rose 0.55%.

Strengths

- The best performing precious metal this week was platinum, up 11.77%. New research from Chinese scientists shows how near-total atom utilization of platinum can boost efficiency and cut costs, highlighting its growing role in sustainable chemical production.

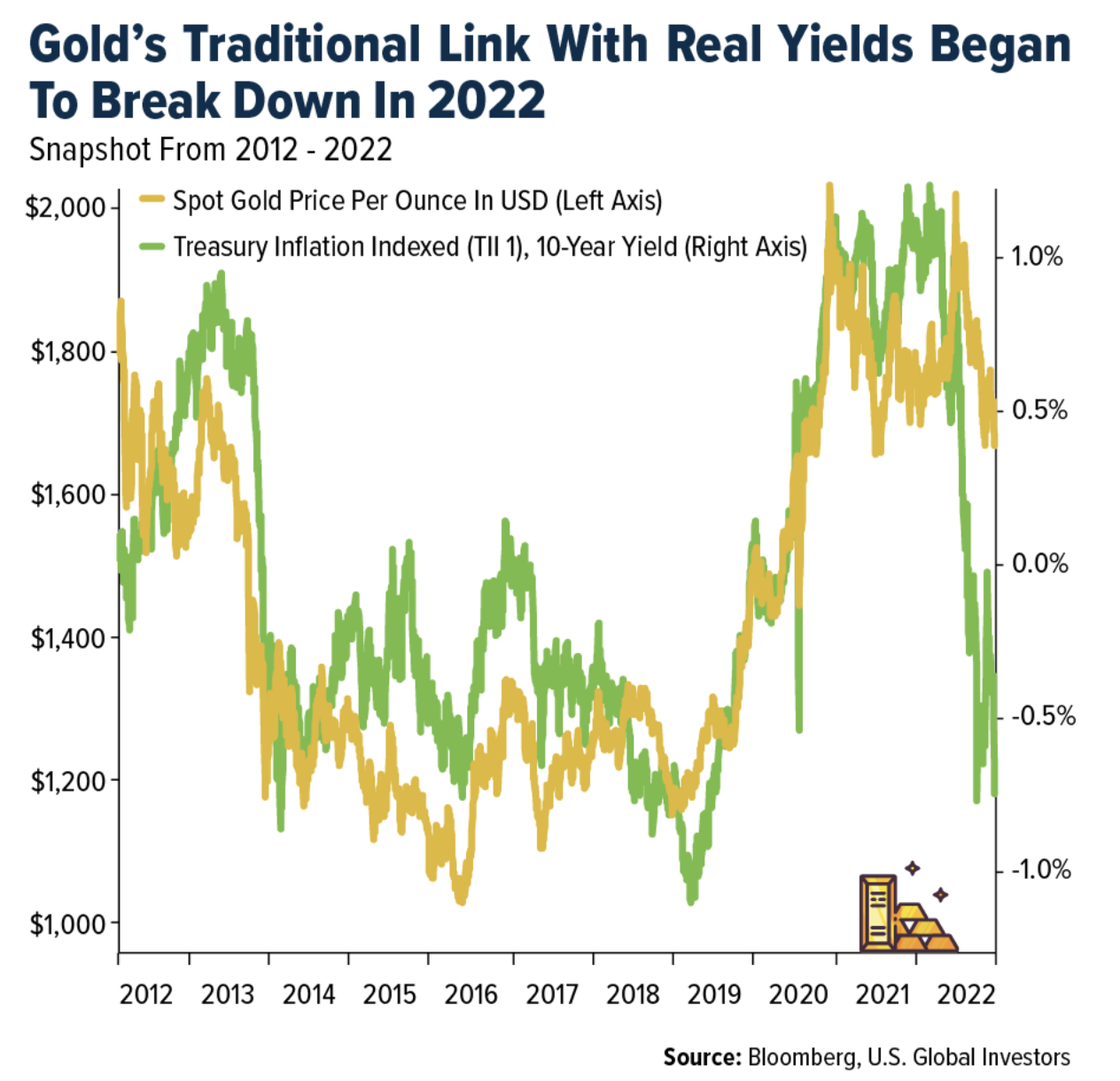

- The disconnect between gold and real yields reveals a growing investor desire for safety, highlighting a structural shift toward bullion as confidence in sovereign bond markets collapses. The traditional inverse relationship between gold prices and the inflation-adjusted 10-year Treasury yield (a real yield proxy) broke down in 2022 amid central bank bullion purchases. Widening fiscal turmoil worldwide, along with geopolitical and trade tensions, has emboldened retail investors and hedge funds to chase the record-setting precious metal rally, according to Bloomberg.

- Mali has approved seven agreements granting the state increased revenue from international and local mining companies in the military government’s latest effort to boost income from the sector. The Council of Ministers approved the exploitation and exploration agreements, securing Mali a guaranteed, non-reducible stake in mining projects with priority access to dividends, reports Reuters.

Weaknesses

- The worst performing precious metal for the week was gold, still up 2.67%. Gold’s strength is highlighted by its sixth consecutive weekly gain, driven by safe-haven demand amid geopolitical tensions, steady inflows into bullion-backed ETFs, and a risk-off tone in global markets. With prices up 43% this year and support from central bank buying alongside Fed rate cuts, the metal remains on track to extend its rally.

- The World Gold Council notes that gold withdrawals from the Shanghai Gold Exchange (SGE) declined again month-over-month in August, as weak investment demand masked a rebound in jewelry sales. Amid improving risk appetite among local investors, Chinese gold ETFs saw further outflows in August, and gold futures trading volumes on the Shanghai Futures Exchange (SHFE) also fell due to low price volatility throughout most of the month.

- ARIS confirmed a collapse in the main shaft access of the La Reliquia Mine, a third-party operation within ARIS’s Segovia title but outside its infrastructure. Twenty-three workers were underground at the time, including five ARIS employees. ARIS successfully rescued all workers after two days underground.

Opportunities

- Barrick Mining Corp. shares are rallying the most in five years on hopes that its U.S. Fourmile project in Nevada will become a major gold mine. A preliminary assessment suggests up to 750,000 ounces of annual production, leading analysts to raise price targets, according to Bloomberg.

- Angola’s state-owned diamond company Endiama has offered to buy a minority stake in De Beers to help keep the company independent, following Botswana’s move to seek control. Angola’s Ministry of Mineral Resources said the bid is fully financed and does not seek majority ownership.

- RBC notes gold producers have generated strong free cash flow at current spot prices. While M&A has focused on producers recently, developers may be next as mid-cap producers use cash for growth via acquisitions. Rising prices and share gains could spark a new wave of deals.

Threats

- Noting that gold’s surge began around the time the U.S. announced sanctions on Russia in response to its invasion of Ukraine, Bank of America suggests that a resolution to this conflict, and other major geopolitical tensions like the U.S.-China trade dispute, could reduce safe-haven demand. Another potentially bearish factor for gold is a bubble-driven rally in the U.S. dollar, which could draw capital into the U.S., trigger a bond sell-off, and push real interest rates higher.

- Parabolic price changes are unsustainable, notes Bloomberg. Since 1980, when gold’s trailing one-month gain has been 10% or more, the average one-week forward return has been -0.45%, with a one-month decline of -1.13%. Since 2020, the forward performance has been even worse, with a one-week change of -1.12% and a one-month drop of -3.91%. A near-term pullback in gold could be likely.

- Vault released its FY2026 production and cost guidance following contract changes. Its production forecast of 332,000–360,000 ounces was slightly below consensus expectations of 365,000 ounces, about 5% lower at the midpoint. While FY2026 gold production guidance is down 9% year-over-year at the midpoint, earnings are expected to rise 35% due to expiring hedges and a higher gold price, according to RBC.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (06/30/2025):

United Parcel Service Inc.

Embraer SA

Ferrari

LVMH Moet Hennesey

Brunello Cucinelli

Tesla

General Dynamics Corp.

Barrick Mining Corp.

Vault Minerals Ltd.

Electra Battery Materials

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The Shanghai Containerized Freight Index (SCFI) is a weekly measure of spot shipping rates for container transport from Shanghai to major global ports, serving as a key indicator of global trade and freight market trends.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits