Summary

- Venture Global (VG) is a rapidly expanding U.S. LNG producer that uses an innovative modular construction approach to build export terminals faster and at a lower cost, positioning it to potentially become the largest U.S. LNG producer.

- The company’s commercial strategy relies on stable, long-term contracts. It also involves selling LNG at fluctuating spot market prices during a facility’s commissioning phase. That adds earnings volatility and has resulted in legal disputes with customers.

- VG is prioritizing aggressive growth, aiming for 100 million tons per annum (MTPA) of production capacity in operation or under construction by 2030.

Venture Global (VG), which went public earlier this year, is a rapidly expanding, low-cost producer of U.S. liquefied natural gas (LNG). Its business centers around liquefaction, which is the process of cooling natural gas into LNG, making it possible to ship overseas. The process takes place at massive export terminals where the gas is processed and loaded for overseas shipment. Learn more about VG’s asset base, business model, and capital allocation plans below.

Inside VG’s Growing Asset Base

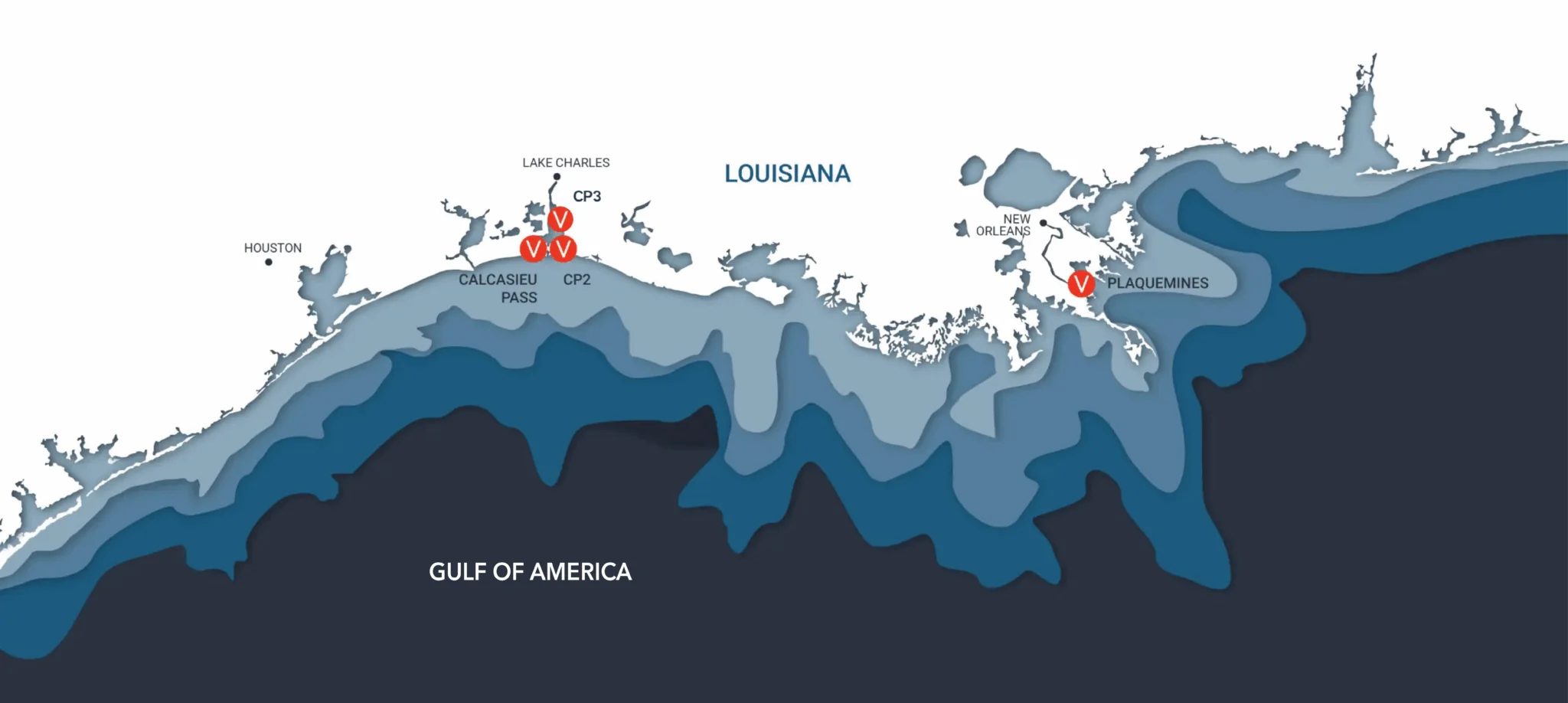

Founded in 2013, Venture Global positions itself as a long-term, low-cost provider of U.S. LNG. The company operates two LNG export facilities — Calcasieu Pass and Plaquemines, which is still commissioning. A third LNG export project, CP2, is under construction, having reached final investment decision (FID) for its first phase in late July. (FID is the point where a company formally commits to a project.) All of VG’s current and proposed projects are located along the coast of Louisiana, which provides deep-water access for tankers and proximity to an extensive natural gas pipeline network. VG is on track to be the largest LNG exporter in North America.

Calcasieu Pass has peak capacity of 12.4 million tons per annum (MTPA). By the end of this year, Plaquemines Phase 1 and 2 are expected to have combined peak capacity of 27.2 MTPA. Projects operating or under construction (including Phase 2 of CP2, which is expected to reach FID next year) represent 67 MTPA of LNG export capacity. However, with bolt-on expansions, VG sees a path to 100 MTPA of LNG production capacity by 2030. That equates to ~17.8 billion cubic feet per day (Bcf/d). For context, U.S. peak nameplate LNG export capacity is currently 17.1 Bcf/d (read more).

Source: Venture Global Website as of September 2025.

To support export volumes and create an integrated business, VG is expanding its asset base into pipelines, LNG tankers, and downstream markets. VG’s natural gas pipelines include TransCameron (supplying Calcasieu Pass), Gator Express (Plaquemines), the under-construction CP Express (CP2), and the under-construction Blackfin. (Blackfin is a joint venture with WhiteWater that will feed into CP Express). VG has also contracted to acquire nine LNG tankers. They are scheduled to be delivered on a rolling basis, with the company having received four as of Q2. Finally, VG is securing downstream market access in Europe, contracting for regasification capacity at the UK’s Grain LNG (42 cargoes/year from 2029) and Greece’s Alexandroupolis terminal (12 cargoes/year from October 2025).

VG’s Unique LNG Playbook

VG uses a unique “design one, build many” approach, where it prefabricates and pre-tests 0.6 MTPA liquefaction modules in a controlled factory setting. This innovative approach contrasts with the “stick-built” construction method used for most liquefaction terminals. This involves building a highly customized, large-scale facility almost entirely on site. VG’s differentiated approach allows it to improve the predictability of delivery schedules and shorten the time to first LNG. VG generally expects its facilities to have excess capacity of at least 30% relative to its nameplate capacity, with excess capacity available for sales on a short- or long-term basis.

Calcasieu Pass was the first project to prove VG’s modular construction concept at scale. Plaquemines is being developed in phases. Phase 1, like Calcasieu Pass, has 18 trains. Plaquemines has the distinction of being one of the fastest-built greenfield LNG projects in the world, as it reached first production only 29 months after its FID. Phase 2 remains under construction, and VG expects to reach FID on Phase 3 of Plaquemines after CP2.

Like most LNG exporters, VG’s commercial strategy centers on securing long-term sales and purchase agreements (SPAs) with customers. These contracts typically span 20-year terms and are secured before the company reaches FID on a project. The average remaining contract duration on VG’s existing SPAs of 43.5 MTPA is 19 years. The majority of contracts are signed with large investment-grade companies. This provides VG with a baseline of stable long-term revenue streams.

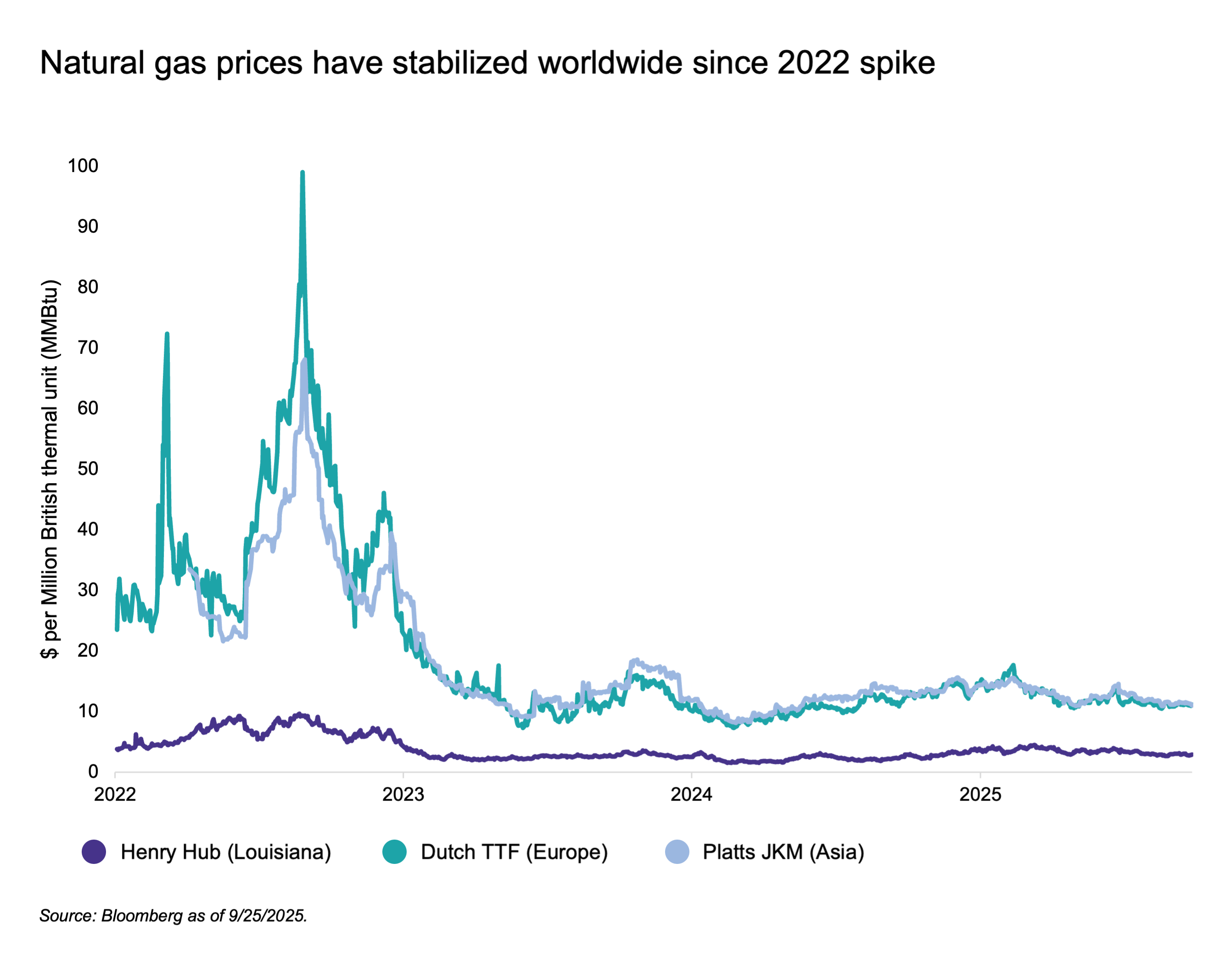

From early 2022, when its first cargo shipped, until the start of commercial operations earlier this year, Calcasieu Pass was in an extended commissioning phase, during which facilities perform final testing and preparation for commercial service. When global LNG prices spiked in the summer of 2022 following Russia’s invasion of Ukraine, VG capitalized by selling LNG at lofty spot market prices instead of delivering it to long-term contract holders.

While VG defended the move as legally permitted by its contracts, foundational customers including Shell, BP, and Repsol viewed the extended commissioning phase as an act of bad faith and filed a series of arbitration lawsuits. Recently, an arbitration tribunal ruled in VG’s favor against Shell in a key initial victory, validating VG’s stance. Still, the company faces similar pending arbitration proceedings with other long-term customers, leaving a degree of legal uncertainty. Management is confident in a positive outcome for the other arbitration proceedings given very similar contracts and the same set of circumstances.

VG continues to be exposed to fluctuating global prices through its commissioning strategy, with Plaquemines’ commissioning phase extending from December 2024 to 4Q26. This exposure can make VG’s earnings more volatile. For example, a narrowing of the spread between domestic gas prices and international prices in 1Q25 contributed to the company lowering full-year 2025 EBITDA guidance in May from a range of $6.8 billion to $7.4 billion to the current range of $6.4 billion to $6.8 billion.

VG’s most recent full-year 2025 guidance assumes a liquefaction fee range of $6.00 to $7.00/MMBtu for cargos not yet sold for this year. Based on this assumption, the company has projected that a $1.00/MMBtu change in the liquefaction fee received for unsold cargos will impact 2025 EBITDA by $230 to $240 million.

Capital Allocation Prioritizes Growth

VG’s IPO on the New York Stock Exchange was the largest energy IPO by valuation in U.S. history. Though downsized from its initial target, the offering still valued the company at $65 billion. It raised $1.75 billion in gross proceeds. These funds are central to VG’s capital allocation strategy. This strategy fully focuses on funding the buildout of its LNG asset base. The company uses project-level financing for its LNG export terminals. It dedicates corporate funds, including its IPO proceeds, to pre-FID activities, tankers, and pipelines.

Even at this early stage, VG is generating significant cash from operating activities. Calcasieu Pass and commissioning cargos from Plaquemines helped VG bring in $2.6 billion in the first half of 2025. The scale of the company’s ambitious investments has lifted capital spending much higher, at $6.4 billion in 1H25. These expenditures rely on both internally generated cash and project-level debt.

At the end of 2Q25, VG had roughly $30 billion in long-term debt and had raised approximately $80 billion of capital since inception. The $15.1 billion financing for CP2 Phase 1 was the largest stand-alone project financing ever. While the company has a high-yield (BB-) rating from S&P, reflecting the execution risk associated with its massive construction pipeline and high overall leverage, its project-level debt has a stronger credit rating, which lowers borrowing costs. For example, S&P recently upgraded the Calcasieu Pass project’s credit rating to investment-grade (BBB-) as it commenced commercial operations. Senior secured notes for the Plaquemines project are rated BB+ by S&P.

As of September 26, VG has fallen ~40% since its debut, bringing its market capitalization to $36 billion. This decline was driven in part by several aspects. They include the lowering of full-year guidance, investor concerns over high debt, and ongoing legal proceedings. This has brought VG’s forward EV/EBITDA ratio to 10.2x, below that of its peer, Cheniere Energy (LNG) at 10.8x as of September 26.

VG Adds Liquefaction Exposure in Midstream Indexes

VG was added to the Alerian Midstream Energy Select Index (AMEI) and other Alerian midstream indexes with C-Corps in their September rebalancings. AMEI includes 75% U.S. and Canadian C-Corps, with the remaining 25% made up of midstream MLPs. VG had a weight of 2.7% in AMEI as of September 25. Alongside Cheniere Energy and NextDecade (NEXT), liquefaction companies have a combined weight of 8.1% in AMEI as of September 25.

Looking for midstream insights in your inbox? Subscribe here to keep a pulse on midstream investing through our weekly updates.

AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the ALPS Alerian Energy Infrastructure Portfolio (ALEFX).

Related Research:

Investors Underestimating U.S. LNG Export Growth

Sizing Up the Next Wave of U.S. LNG Export Projects

Cheniere Grows LNG Capacity, Updates Dividend Outlook

U.S. LNG Dealmaking Picks Up With Benefits for Midstream

Venture Global Files for IPO as U.S. LNG Export Capacity Expands

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for ENFR and ALEFX, for which it receives an index licensing fee. However, ENFR and ALEFX are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of ENFR and ALEFX.

For more news, information, and analysis, visit the Energy Infrastructure Content Hub.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by VettaFi